The graphs below point to a potential problem for corporate bond investors. The graph on the left highlights that as banks tighten lending standards, corporate defaults rates tend to rise about nine months later. Bank lending standards are tightening rapidly. The graph provides credence to a topic we have spent a lot of time, the lagging effects of monetary policy. If the typical nine months between lending standards and defaults holds up, we are likely to see corporate bond yield spreads to U.S. Treasuries widen soon.

We are well aware that corporate bond spreads widen during recessions. As such, we are taking a conservative approach to corporate bonds. We are primarily sticking with higher rated, shorter-term corporate bonds whose spreads will not come under much pressure, unlike lower rated, longer term bonds. Remember that the spread widening during a recession is a function of risk. Corprorate bond investors, will rotate to less risky bonds via higher quality and lower duration bonds when yield spreads widen and bond defaults rise.

What To Watch Today

Economy

- 8:30 a.m. ET: Trade Balance, December (-$68.5 billion expected, -$61.5 billion prior)

- 12:40 p.m. ET: Fed Chair Powell Speaks

- 3:00 p.m. ET: Consumer Credit, December ($25.000 billion expected, $27.962 billion prior)

Earnings

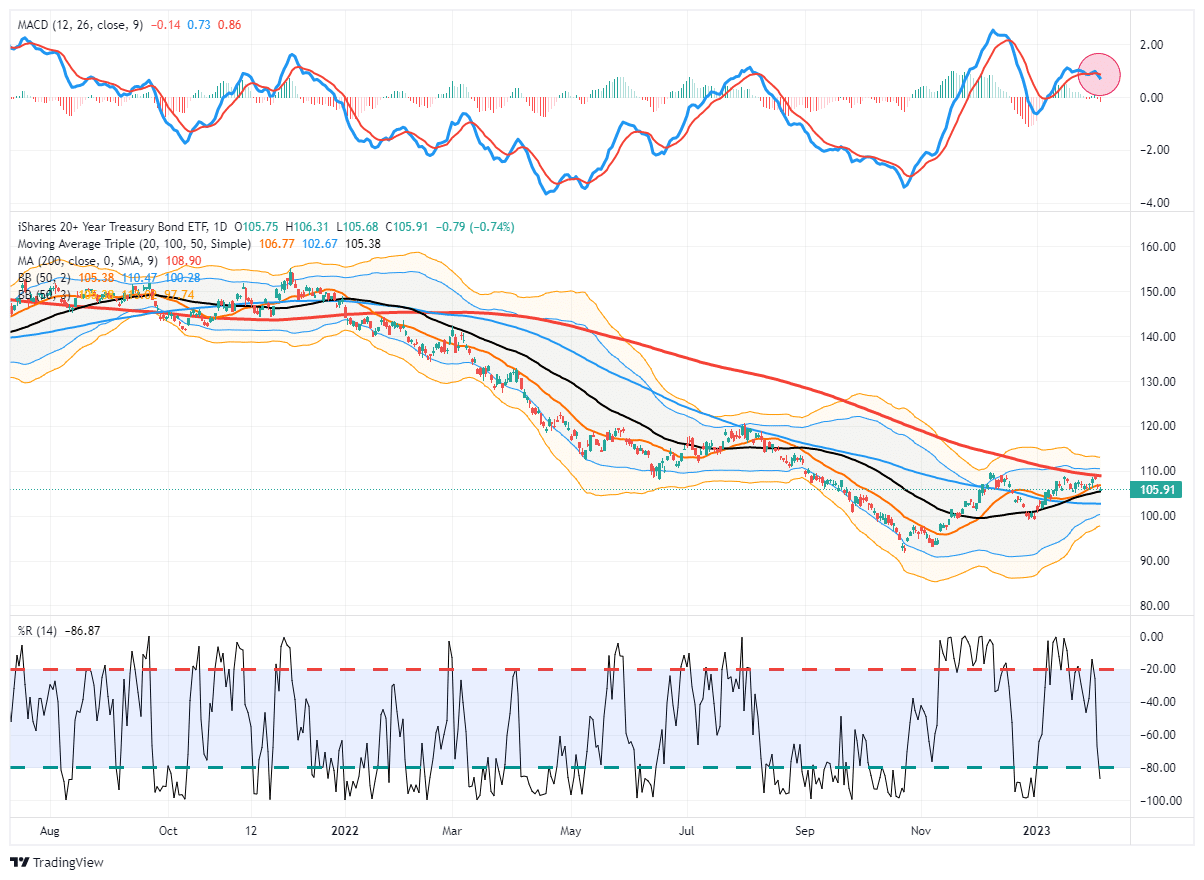

Market Trading Update – Bonds

We have received many emails lately asking when it will be time to buy long-dated Treasuries. Currently, the MACD sell-signal currently suggests that bond prices could struggle as the Federal Reserve continues hiking interest near-term. However, once that rate hiking cycle is complete, there should be a substantial upside to Treasury bond prices in the future.

Be patient and wait for the bond “buy” signal. With the 50-DMA set to cross the 200-DMA and the price consolidation becoming tighter, a breakout to the upside should prove to be rather explosive. I imagine such a breakout will coincide with something breaking economically that pushes the Fed to reverse its policy. However, that could take several more months to manifest itself, so there is no rush to buy now.

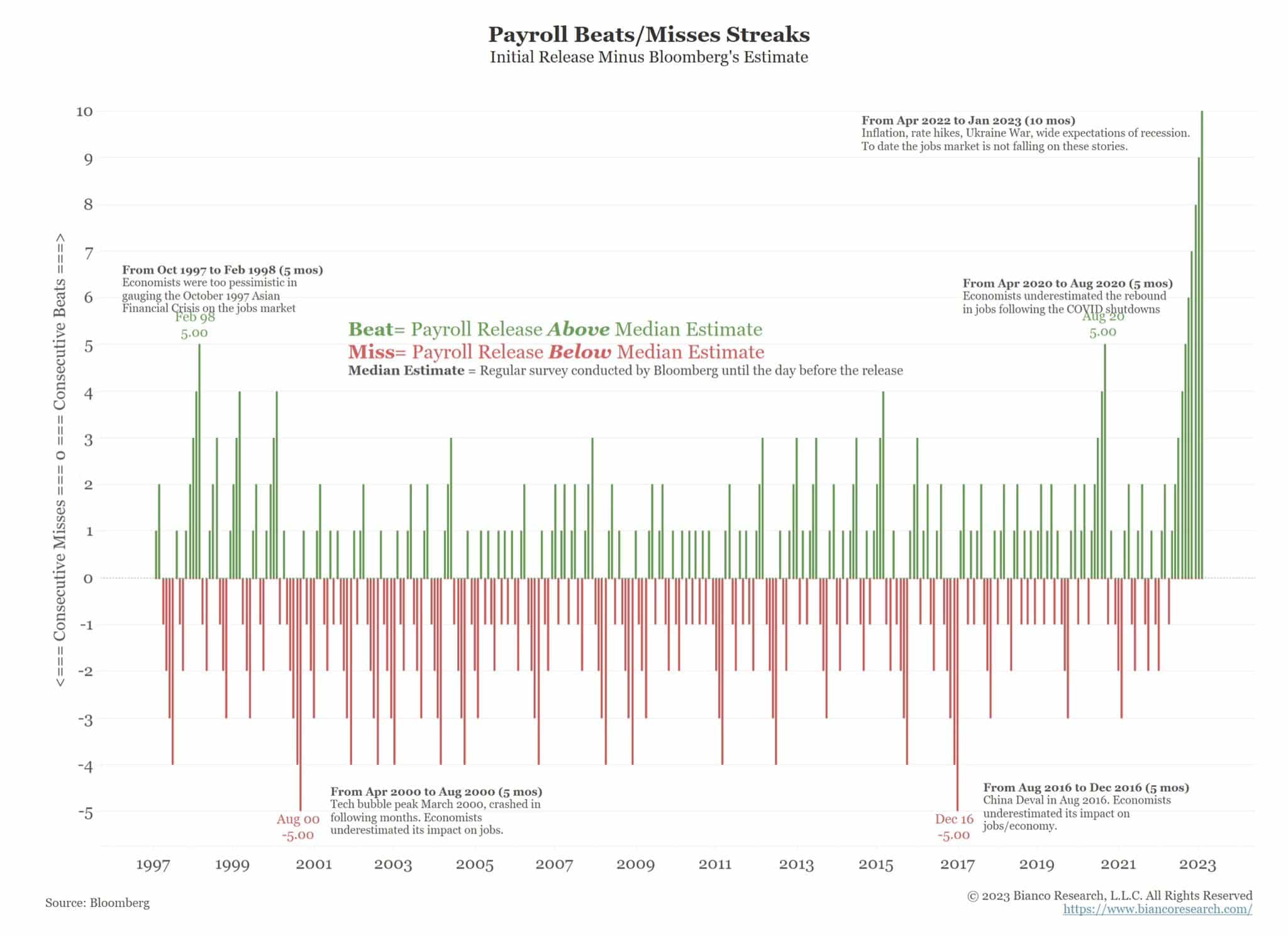

Employment, A Record Streak

Last Friday’s BLS employment report surprised Wall Street’s economic analysts. This is nothing new. The last time economists over-estimated job growth was in March 2022. The ten-month underestimating streak dwarfs all others in at least the last 25 years. The prior record was five months on two separate occasions, as shown below.

A Glut of Commercial Office Space is Here to Stay

According to Kastle Systems, office occupancy in the top ten metro areas just topped 50% for the first time since the pandemic started. While the improvement is good, the vacancy rate remains very high. More concerning, it may be near a peak. Per the Washington Post:

But the return-to-office figures are unlikely to go much higher as flexible work becomes entrenched in the lives of white-collar workers, experts say

While companies may want their employees in the office more often, they also reap benefits from allowing remote location flexibility. For starters, companies can enlarge the population of qualified potential employees, as the office location is no longer a hindrance. Such allows a more competitive roster of potential employees and more leverage in setting pay. In such a tight labor market, these factors can be critical.

Per the National Association of Realtors, the following five metro areas have the highest office vacancy rates:

- Houston 18.9%

- Dallas/Ft. Worth 17.6%

- San Francisco 15.5%

- Washington DC 15.2%

- Chicago 15.1%

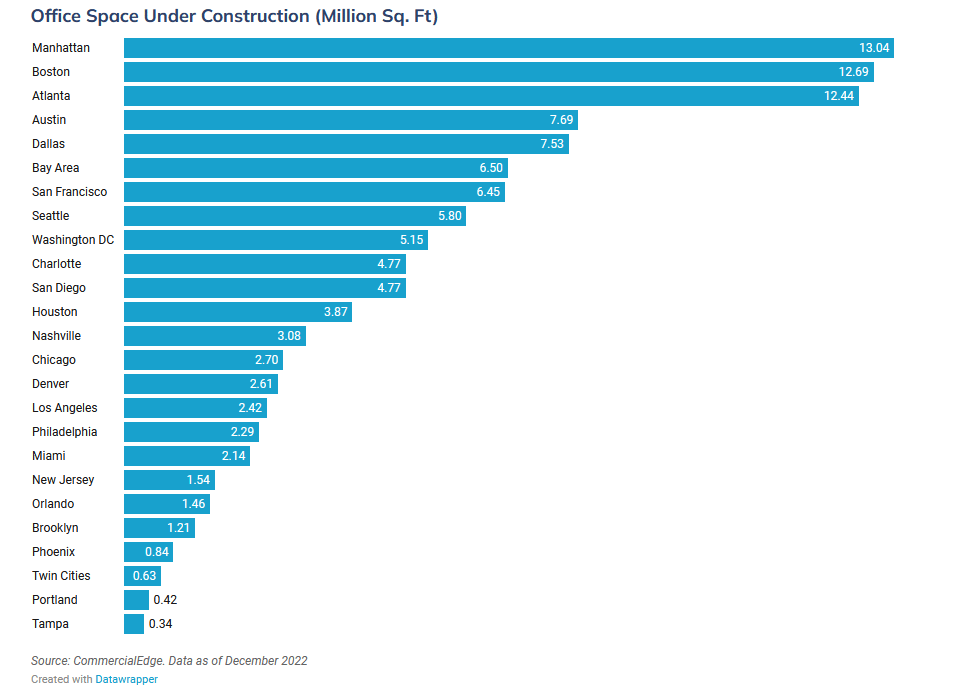

Further complicating the picture, the vacancy rates will likely rise as multiyear tenet leases come up for renewal negotiations. Many companies will likely opt for less space in their next lease. Further, new supply is coming to the market, as shown below.

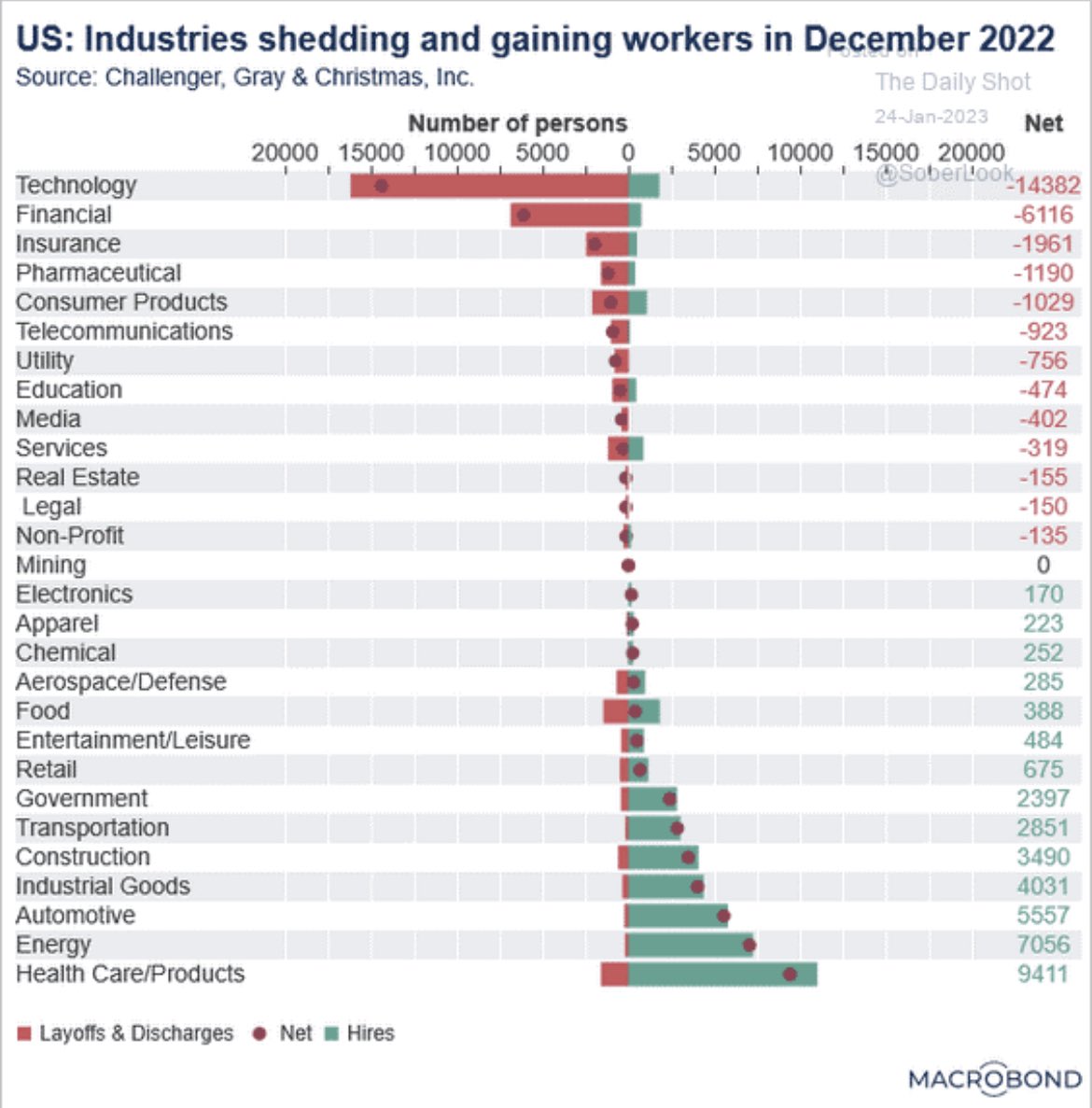

Why Are Wages Controlled Despite Tight Labor Conditions?

Over the last few days, we broke down the BLS jobs report and numerous other labor data. The broad takeaway is that the labor market is extremely tight. The graph below may help explain why the market is historically tight, but wages are not rising as quickly as many would expect in such a jobs market. The bottom line, the economy is losing jobs in the higher paying sectors and gaining them in lower paying sectors.

For example, consider what happens to jobs statistics if a tech person in middle management earning 100k a year loses her job, but a restaurant or hotel hires two new employees at $35,000 a year. In this case, average and total wages will decline despite what many labor reports characterize as a stronger market.

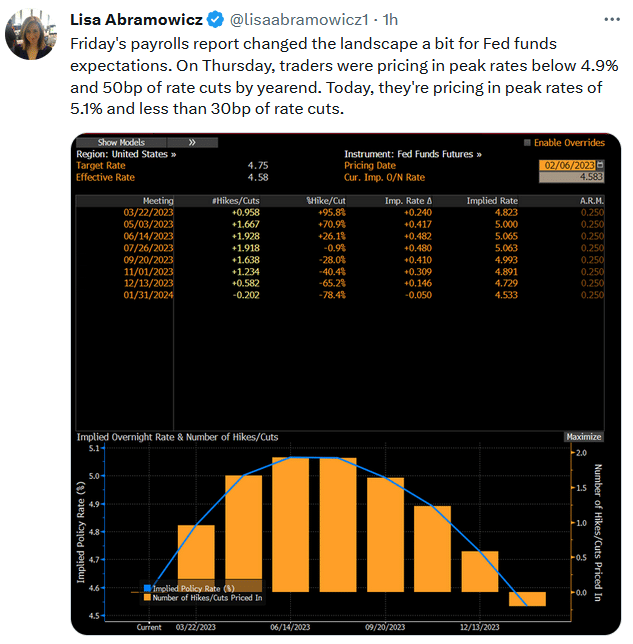

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.