The Fed’s media mouthpiece, Nick Timiraos of the Wall Street Journal, let it be known the Fed will likely raise rates by 75bps at the Fed’s September meeting. Per his article, Fed on Path for Another 0.75-Point Interest Rate Lift: “The Federal Reserve appears to be on a path to raise interest rates by another 0.75 percentage point this month in the wake of Chairman Jerome Powell’s public pledge to reduce inflation even if it increases unemployment.” Goldman Sachs quickly followed the Fed’s lead and increased its rate expectations. Goldman now forecasts 75bps in September, 50bps in November, and 25bps in December. Such a path would bring Fed Funds to 4% by year-end.

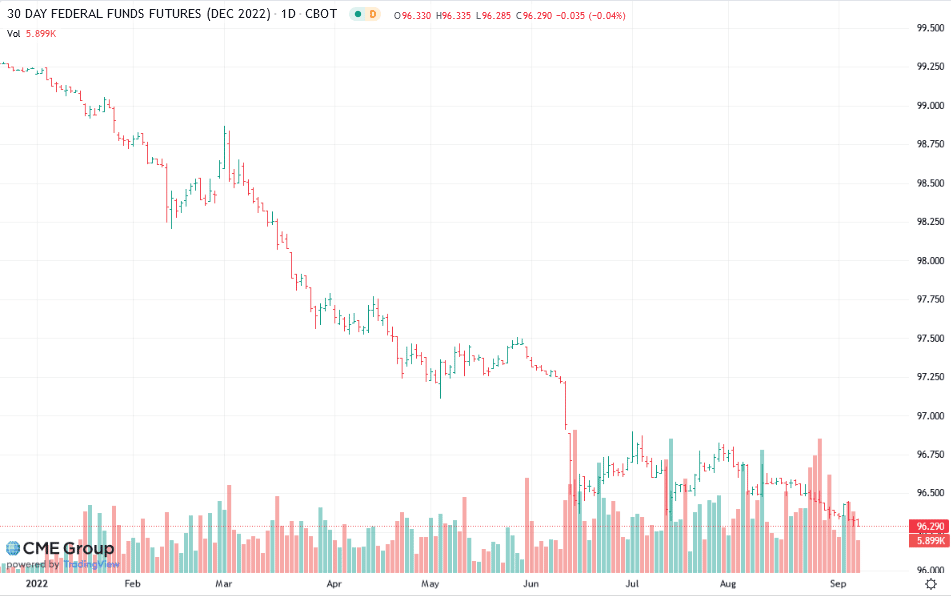

The equity markets rose despite Nick’s article and Goldman’s increased expectations. The market is pricing a 75bps rate hike this month but not matching Goldman’s longer-term forecast. December Fed Funds futures expect Fed Funds to be 3.71% (100-96.29) by year-end, as compared to Goldman’s 4% expectation.

What To Watch Today

Economy

- Wholesale Trade Sales, month-over-month, July (1.8% previously)

- Wholesale Inventories, month-over-month, July final (0.8% expected, 0.8% previously)

- Household Change in Net Worth, Q2 (-$544.0 billion previously)

Earnings

Market Trading Update

The market chopped around yesterday as the bulls tried to keep Wednesday’s rally alive. However, in the face of a hawkish ECB, followed by Powell’s statement yesterday, the markets are now coming to grips with a .75% rate hike at the end of the month. As noted, Jerome Powell spoke yesterday, stating:

“We need to act now, forthrightly, strongly as we have been doing. It is very important that inflation expectations remain anchored. What we hope to achieve is a period of growth below trend.”

That last sentence is the most important. If the Fed is pushing or is at least comfortable with below-trend growth, that means that earnings growth will, by extension, be below trend. As noted, the markets have not fully priced in slower earnings growth, much less an earnings recession.

As discussed in yesterday’s 3-minutes video, the market is holding important support for now. However, there is substantial resistance just overhead as the 100-dma is set to cross below the 50-dma. Rallies to resistance should be used to raise cash and rebalance risks for now.

Real Yields 2018 vs. Today

The graph below compares 5yr UST yields, 5yr real yields, and the six-month change in real yields. Many economists believe real yields, or the nominal yield, less inflation expectations, best quantifies how tight or loose monetary policy is. As we show, 5yr real yields are approaching 1%. The last time they were at such a high level was in 2018. At that time, the Fed was conducting QT and raising interest rates. Today the Fed is taking similar actions, albeit much more aggressively. In 2018, real yields peaked at just over 1%, which proved too much for the financial markets. Real and nominal yields plummeted from that point. The decline was further exaggerated by covid in 2020.

In the 2018 instance, the increase in real yields was gradual. As shown in blue, real yields have risen by 2.50% in just six months. Most economists believe it takes changes in interest rates six to nine months to fully take effect. If so, the financial markets may have quite a shock in the coming months.

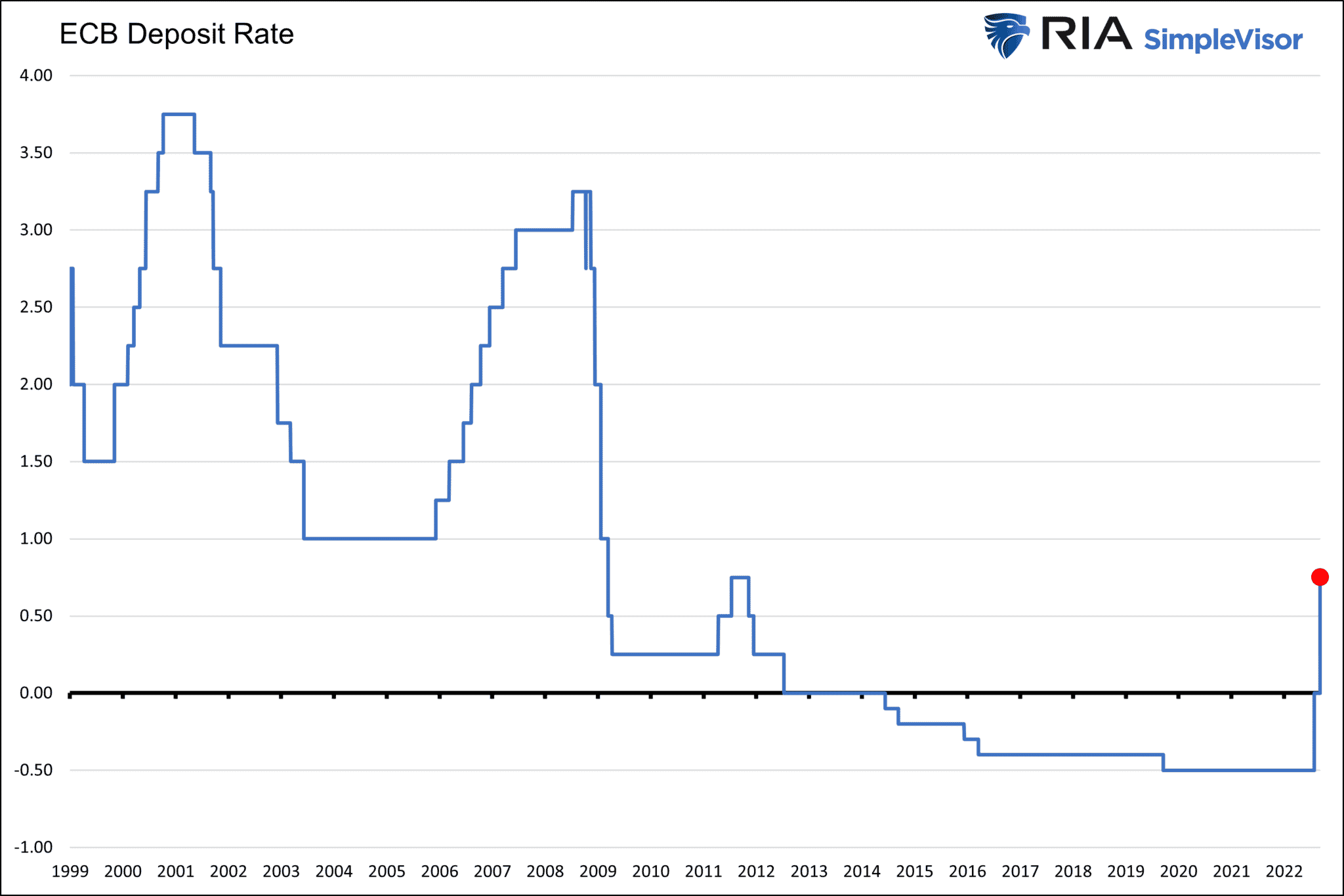

ECB Goes 75bps

The European Central Bank (ECB) raised its deposit rate by 75 basis points on Thursday morning. The move was widely expected and should help stabilize the euro. The ECB lowered its growth forecast but still appears optimistic. They continue to expect the euro economy to grow despite significant economic headwinds and surging electricity prices. Per the ECB’s statement:

After a rebound in the first half of 2022, recent data point to a substantial slowdown in euro area economic growth, with the economy expected to stagnate later in the year and in the first quarter of 2023. Very high energy prices are reducing the purchasing power of people’s incomes and, although supply bottlenecks are easing, they are still constraining economic activity. In addition, the adverse geopolitical situation, especially Russia’s unjustified aggression towards Ukraine, is weighing on the confidence of businesses and consumers. This outlook is reflected in the latest staff projections for economic growth, which have been revised down markedly for the remainder of the current year and throughout 2023. Staff now expect the economy to grow by 3.1% in 2022, 0.9% in 2023 and 1.9% in 2024.

The graph below shows the 75bps rate increase not only brings the rate positive for the first time in eight years but also increases it to the highest level in ten years.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.