The supply side of the energy transition is well on its way, but the demand side of the equation presents a major obstacle to victory. EY published it’s 2024 Energy Transition Consumer Insights Report last week, in which the firm surveyed nearly 100,000 consumers across 21 global markets over three years. As highlighted in the report, the success of the energy transition ultimately depends on one factor: the rate of consumer adoption. Per the report,

Seventy percent of energy transition outcomes will depend on consumers changing their consumption, behaviors and lifestyles.4 Half of consumers’ impact on the energy transition comes directly from shifts in home energy use and transportation

Some consumers are willing to pay higher prices for energy sourced sustainably. However, lofty global inflation over the past three years has heightened the obstacle. The report indicates that consumer fatigue is stagnating progress toward the desired outcomes. EY posits that although 65% of energy consumers know how to do their part, 70% say they won’t spend more time or money doing so.

Our research warns that wavering consumer confidence could become a major handbrake that stalls progress. There simply is no energy transition unless consumers lead the way.

While this is a negative for the energy transition, it presents a valuable opportunity for companies planning to expand fossil fuel capacity in addition to investments in alternative energy sources, such as XOM and CVX. If consumers are unwilling or unable to make the leap due to financial constraints, these players stand to increase both market share and profitability.

What To Watch Today

Earnings

Economy

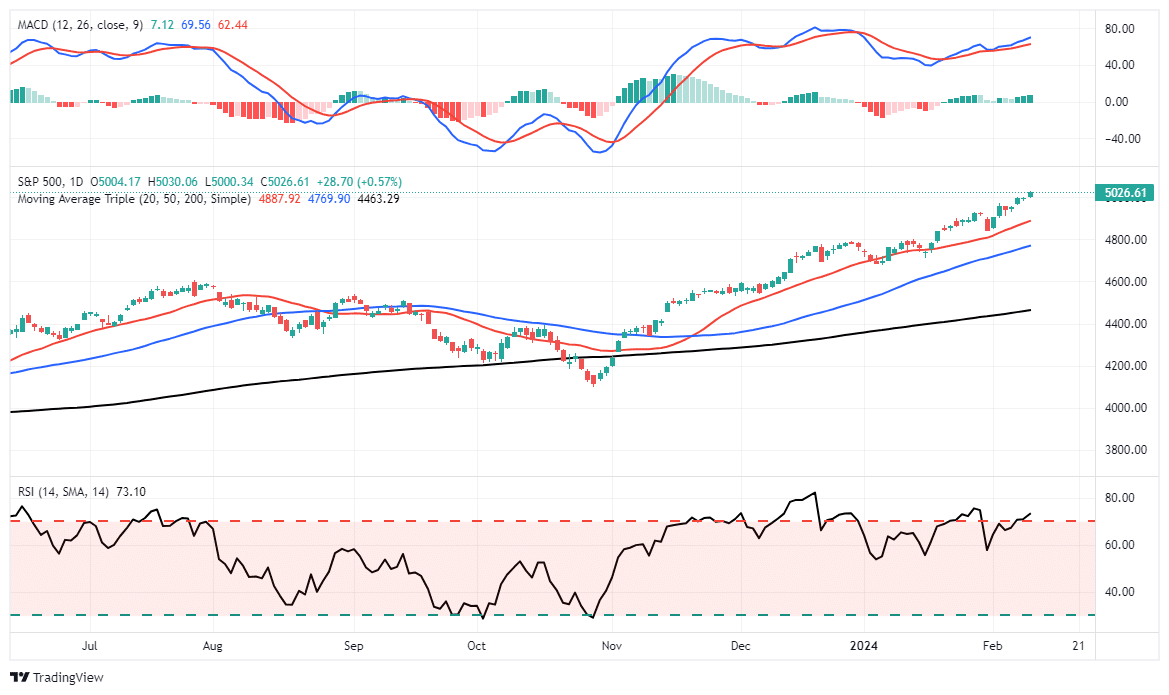

Market Trading Update

On Friday, the market finally broke through 5000. As we had noted in our Daily Commentary:

“Yesterday, the market closed at 4997.91, unable to break above that level. However, such is not surprising given the market remains extended and overbought on many technical levels. Interestingly, we are beginning to see some rotation. Yesterday, the recent leaders lagged while energy and staples outperformed. The action remains spotty, with stocks mostly still trading off earnings reports.”

Well, that rotation didn’t last long. On Friday, the unstoppable advance, driven by the mega-capitalization stocks, topped the psychological 5000 level on the index. With the strong momentum carrying that particular group of stocks, the index will likely try to push higher over the next few days. However, as shown, the market is back to more extreme overbought levels, and bullish sentiment has reached “greed.”

Most notably, the deviation between the index and the 200-DMA is getting rather extreme as well, which has typically preceded short-term corrections. As discussed in this week’s newsletter, those extensions and deteriorating internals suggest we should begin rebalancing portfolio risk.

While we are highly confident that a correction is coming, the timing of that event is uncertain. As such, we must maintain exposure to garner performance while we can. However, once signals are triggered, we will become more aggressive in the risk reduction process.

The Week Ahead

This week brings some important economic data to the forefront. We kick off the week tomorrow with inflation data for January. The consensus estimate for headline inflation is 0.2% MoM, reflecting a decrease of 10 basis points from December. Core inflation is expected to remain flat at 0.3% MoM, reflecting an annualized 3.6% rate of inflation. Regardless of how the results pan out, we expect the Fed to continue downplaying the possibility of rate cuts early this year.

Thursday brings the release of retail sales data for January, which will give us insight into how consumers are faring after the holiday season. The consensus expectation is an increase of 0.2% MoM. When paired with inflation estimates, real retail sales are expected to be flat in January, down from 0.3% in December. Finally, Friday brings January’s PPI data and a preliminary look at Consumer Sentiment in February. The consensus expects PPI to rise to +0.1% from three consecutive months in the red.

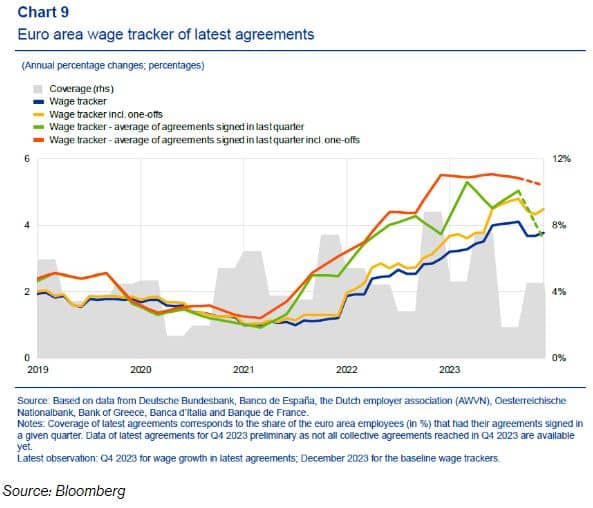

Euro Area Wage Growth Charges On

The ECB developed a new wage tracker to aid its interest rate policy decisions. It makes data from the new collective bargaining agreements available to central bank officials more quickly than previously possible. While inflation slowed dramatically last year, the wage growth in the Euro Area presents an obstacle to policymakers. Wage growth will be a critical factor in the timing of rate cuts for fear of a resurgence in inflation via “price/wage spiral.” The ECB is likely taking notice of the Fed’s playbook and waiting for clear and convincing evidence of slowing inflation before taking its foot off the brake. According to Bloomberg,

The latest collective-bargaining agreements through end-2023 “do not show a clear indication of a turning point for negotiated wage growth yet and the long average contract duration in some countries could potentially lead to quite some persistence of the current high wage growth rates in the future,” the ECB said.

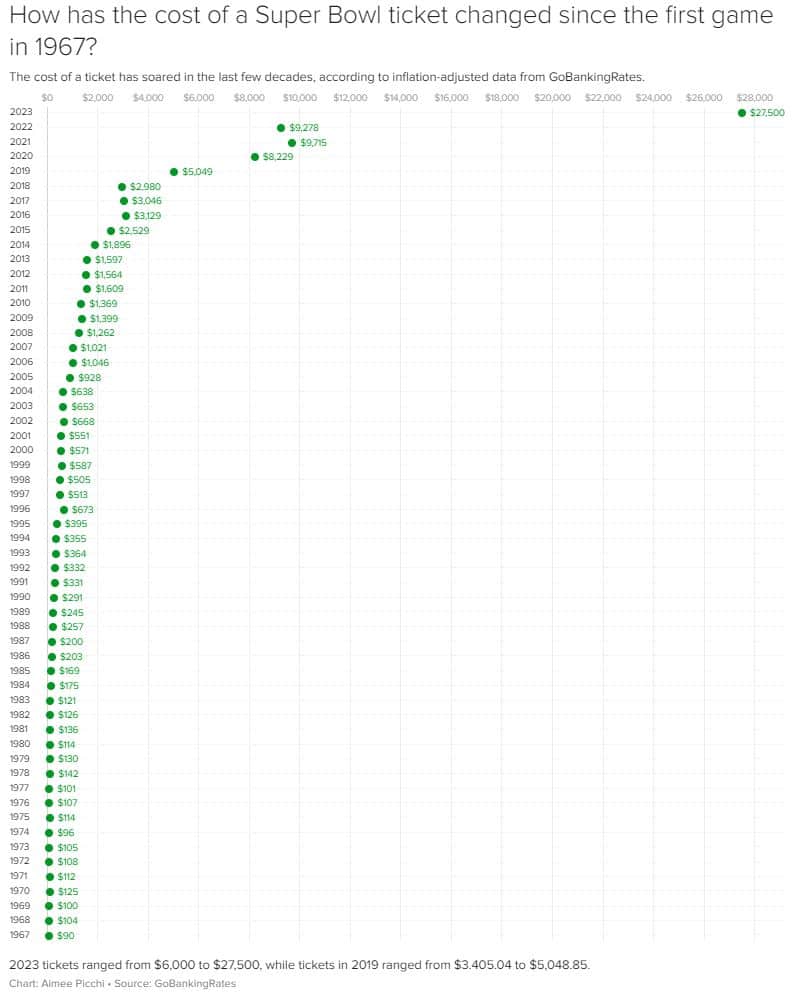

The Wealthy Paid-Up to Attend the Big Game

Ticket prices surged ahead of Yesterday’s Super Bowl LVIII in Las Vegas, Nevada. According to CBS News, a fifth of the tickets changed hands in the week leading up to the event. Surging prices in the resale market created a major obstacle for many with dreams of attending. As of Wednesday, the average ticket purchased on StubHub was $8,600. Meanwhile, resellers were asking up to $45,000 for a single ticket.

The chart below illustrates the magnitude by which premium ticket prices have surged over the last few decades. It plots inflation-adjusted figures for the highest-priced ticket sales over time. There are a few staggering aspects about this year’s ticket prices. First, the average ticket price increased over 50% YoY, easily topping the previous record from the attendance-restricted game in 2021. Furthermore, the average ticket price in 2024 was in the same territory as the most expensive tickets prior to 2022. Finally, the asking price for the most expensive tickets surged by over 450% since last year.

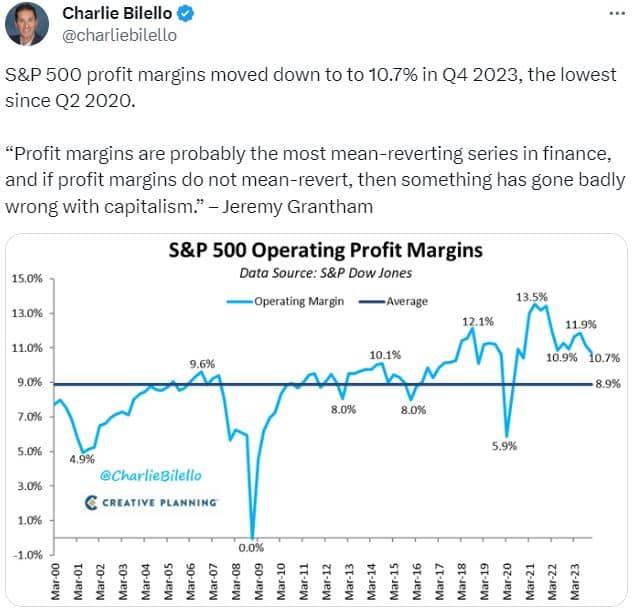

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 3

2024/02/12