Wednesday’s mega-cap tech earnings produced one of the cleaner real-time experiments we’ve seen this cycle. Four hyperscalers reported. All four beat on revenue and earnings. All four committed to massive AI infrastructure spending. Yet the market reactions were wildly divergent: Alphabet surged 10% higher, while Amazon rose 0.8%, Microsoft fell 3.9%, and Meta fell 8.6%. The market isn’t punishing AI spending. It is demanding receipts that justify the magnitude of AI spending.

Alphabet earned its premium with proof. Q1 revenue grew 22% year-over-year, and Google Cloud accelerated to 63% growth, exceeding $20 billion for the first time. More importantly, Cloud backlog nearly doubled quarter-over-quarter to over $460 billion. That is the receipt that matters. Alphabet bumped 2026 capex to a $180-$190 billion range and flagged 2027 as significantly higher, and investors didn’t blink. When the revenue line is showing up that fast, the AI spending number takes care of itself.

Amazon told a similar story on the fundamentals but received a cooler reaction. AWS reaccelerated to 28% growth, its fastest pace in 15 quarters, and management noted customer commitments already cover a substantial portion of the planned spend. The catch is the size of the bill: Q1 capex came in at roughly $43 billion, and Amazon is on track for a $200 billion full-year pace.

Microsoft and Meta are where the bifurcation is most pronounced. Microsoft beat across the board with Azure printing 40% in constant currency and AI annualized revenue hitting $37 billion. Yet management guided full-year capex to roughly $190 billion and warned capacity will remain “constrained” through 2026. The market is asking the right question: when does “constrained” stop being a bullish demand signal and start being a depreciation problem? Meta got the harshest verdict of the four, and we’ll dig into why below.

What To Watch Today

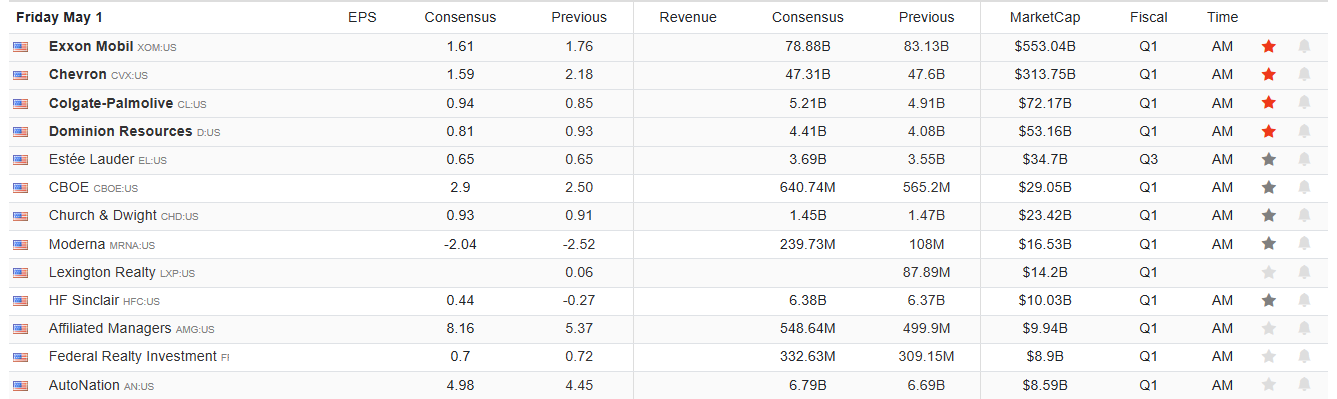

Earnings

Economy

Market Trading Update

Yesterday, we discussed the most crowded trades in the market currently. However, we are now receiving many questions about the lingering effects of high oil prices amid the Iran crisis.

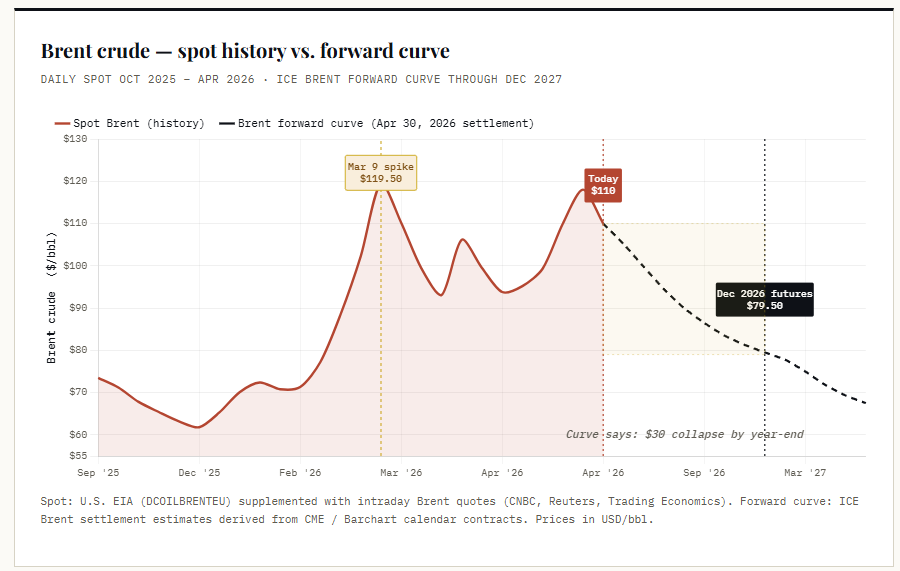

When we framed the oil shock through three scenarios in mid-March, Brent was retracing from its $119.50 panic high, and the burden of proof had shifted to the bulls. Six weeks later, two things have happened that I did not expect — and they tell most of the story heading into May.

First, the conflict has not been resolved. President Trump rejected Tehran’s reopening proposal yesterday and reaffirmed the naval blockade until a nuclear agreement is reached. Brent printed $114 intraday Thursday — its highest since June 2022 — on reports that CENTCOM is briefing the White House on a new wave of strikes. Front-month settled at $118.03 yesterday, then opened today at $111.84 before sliding to roughly $110. The Strait remains effectively closed, and the IEA continues to call this an unprecedented supply shock.

Second, equities don’t care. The S&P 500 remains at or near record levels, the VIX is at 18, and gold is above $4,600. The defensive rotation we discussed in March has been completely unwound. This is despite $110 Brent, an active naval blockade, and an index trading at 22× forward earnings near record highs. That is not a normal coincidence.

What explains it? Look at the futures curve. Front-month Brent is around $108–110, but the December 2026 contract is pricing roughly $80, and the back end falls into the $60s by late 2027. That is the steepest backwardation in modern oil history. The futures market is making a clean bet: this shock is severe but short-lived. Equities are trading the futures view that by year-end, oil normalizes and the earnings drag is contained. The cash market is trading reality: barrels can’t get out of the Gulf today.

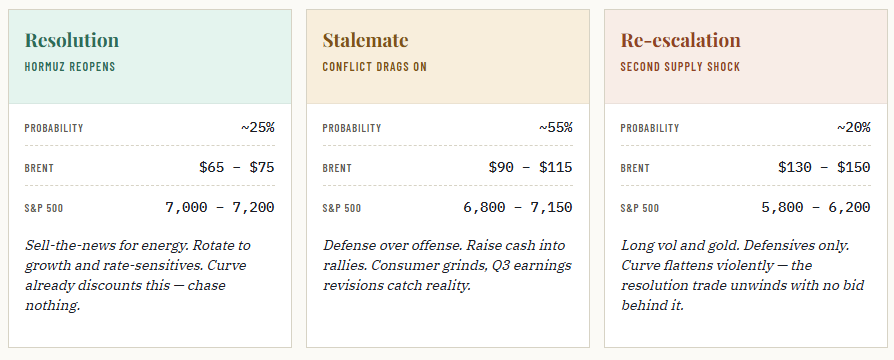

Pay attention to that slope. The market is not pricing oil at $90 in 2027; it is pricing it at roughly $70. That is either a generational good hedging opportunity for any business that buys energy, or a generational mistake that gets corrected violently. Below is the updated three-scenario framework. The structure from March holds; the probability weights and price targets have shifted to reflect the new reality.

Watch the back end of the curve. If Brent in December 2026 breaks above $90, the equity bid for oil-shock complacency disappears.

Trade accordingly.

Meta’s Capex Bill Comes Without A Third-Party Cloud Business

Meta’s headline numbers looked great. Revenue rose 33% to $56.31 billion, the fastest growth quarter since 2021. The problem was everything underneath. Meta lifted 2026 capex guidance to $125-$145 billion, up from $115-$135 billion just a quarter ago, and tagged 2027 spending as “significantly higher” still. Multi-year infrastructure commitments rose by $107 billion in the quarter alone. Adding to the skepticism, an $8 billion tax benefit flattered headline EPS by over $3, making the operating beat look far less impressive against an accelerating spend curve.

The deeper issue is that Meta is the only one of the four hyperscalers without a third-party cloud business to point to as proof of ROI. Alphabet has Google Cloud at 63% growth. Amazon has AWS at 28%. Microsoft has Azure at 40%. Meta has Reels and Instagram ads. Those are excellent businesses, but they are not infrastructure businesses, and the capex bill Zuckerberg is committing to is an infrastructure-business-sized bill. Investors are being asked to fund a hyperscaler buildout against an advertising payoff that, however strong, doesn’t have a contracted backlog like Google’s $460 billion to lean on.

The lesson is that the AI spending debate has matured. The market is no longer arguing about whether the capex is too large in aggregate. It is sorting which companies have shown the receipts and which haven’t. Meta hasn’t yet, and yesterday it paid the price.

New Thematic Model Alert

Let’s travel back in time to revisit one of the primary market narratives before the Iran conflict began in late February: the resurgence of international stocks amid a stretch of superior price performance outside the US, driven by a weakening USD index in 2025. The narrative became: “Investors are shedding US stocks in anticipation of a further weakening in the USD, driving a comeback in international stocks.” While we’ve disputed the arguments in favor of this narrative (and a continued USD weakening in general), we’ve received enough interest from clients and subscribers alike to launch an International Thematic Model.

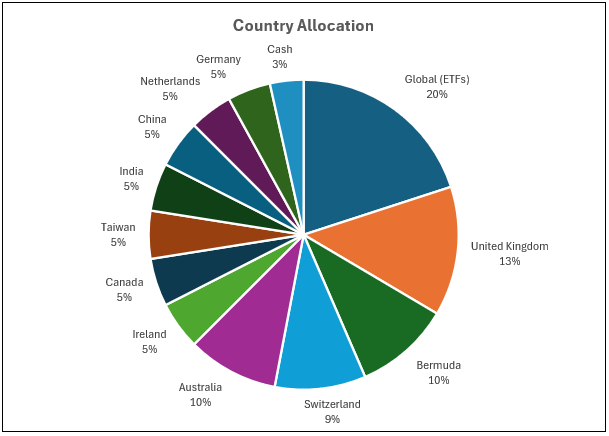

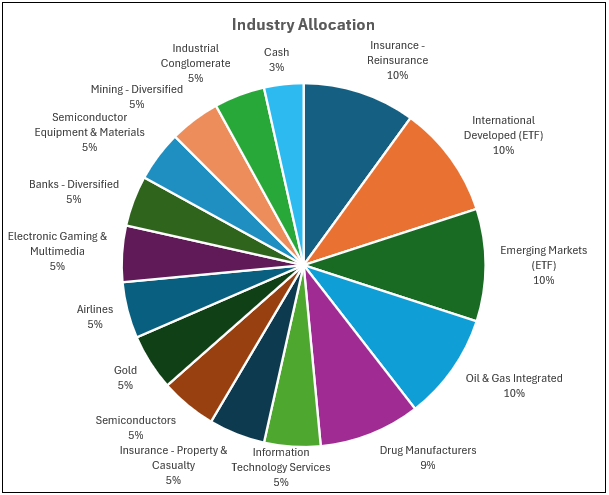

Our International Thematic Model takes a value-oriented approach to investing outside the US. The model allocates roughly 80% across 16 value-oriented stocks, with the remaining 20% split equally between two broad international indices, the iShares MSCI Developed Markets ETF (EFA) and the iShares MSCI Emerging Markets ETF (EEM). The graphs below show that the new model diversifies exposure across both countries and industries.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.