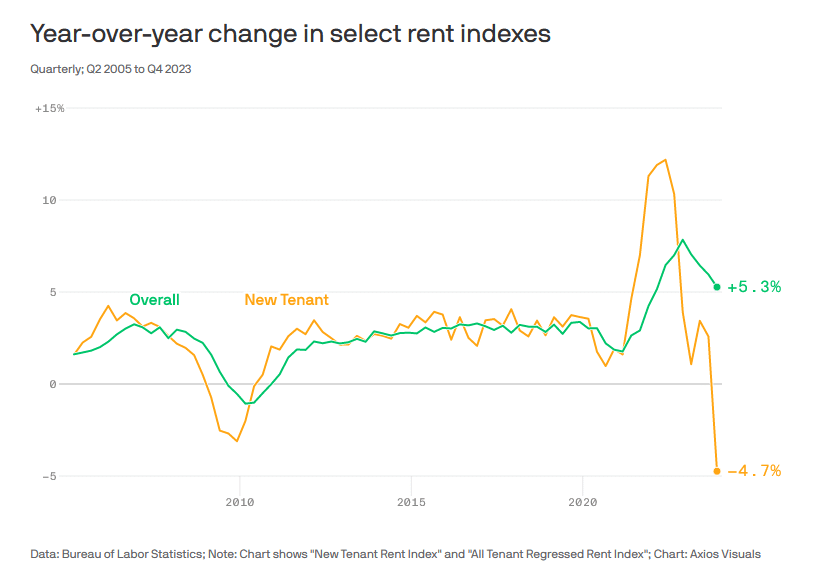

On a few occasions, we have shared data on the differences between real-time rent inflation versus the rental price index used in CPI. In a nutshell, almost all private sector rent indexes are flat to slightly lower. However, the CPI rent index is growing by 0.4% monthly, or nearly 5% annualized. In a telling article, Axios shines a light on what is happening. Most rental agreements are for one-year terms. Therefore, approximately only 1/12th of them come up for renewal in any given month. The CPI index takes the weighted average of the 12 months. Most private rent indexes are based on current asking rates.

So, if CPI-rent lags, what can we expect? The graph below from Axios speaks volumes about what will likely happen to the CPI rent index. Axios compares CPI rent to the BLS gauge of new tenant rent prices. This is like comparing monthly inflation rates to year-over-year inflation rates. Monthly CPI is more volatile than a 12-month average but provides more insight into recent inflation rates. Likewise, the current month of new rental prices are more volatile, but tell us more about the actual state of prices. New tenant rents were down by 0.4% last month or -4.7% annualized. CPI rent rose by 0.45% or +5.3% annually.

We suspect the CPI rent index will follow new tenant rents in the coming months. Rent and imputed rents comprise a third of CPI. If CPI rents fall to actual levels, CPI will likely be at or below the Fed’s 2% target.

What To Watch Today

Earnings

Economy

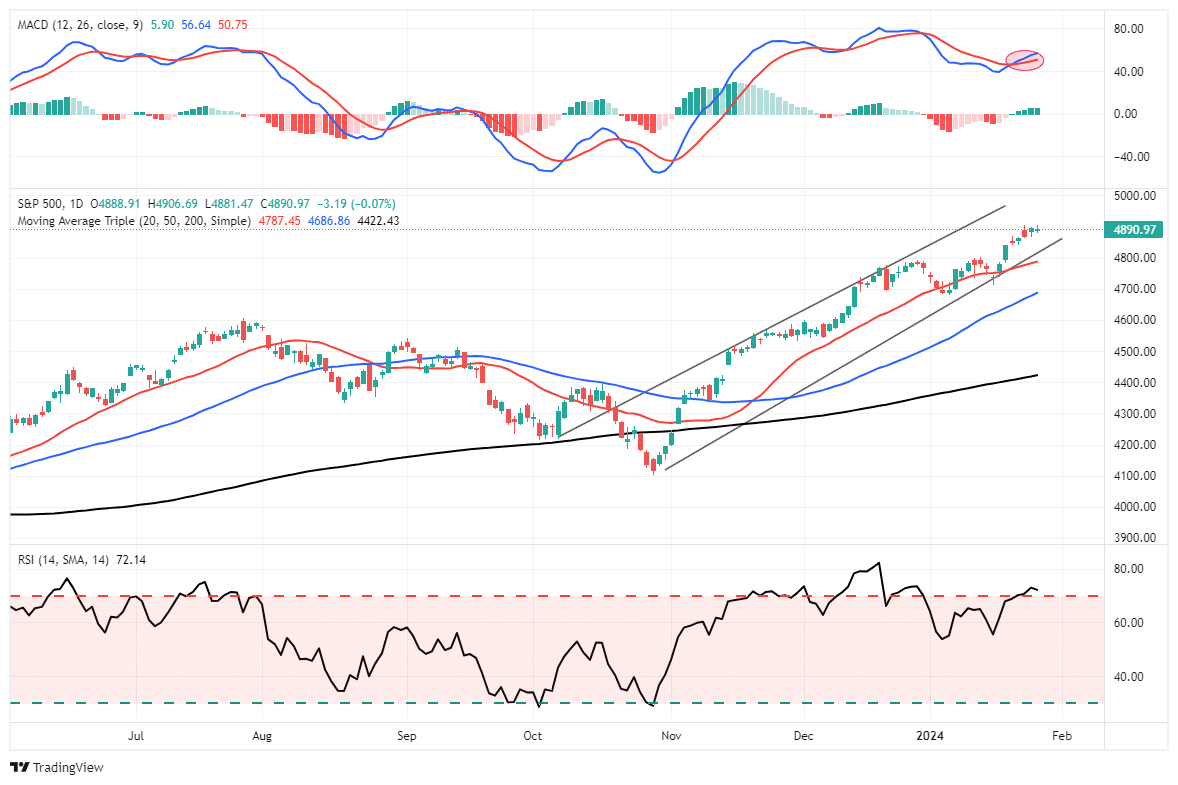

Market Trading Update

Friday’s commentary discussed the continued rally in the market and the breakout to new highs. We also detailed some potential correction levels when one eventually occurs. To wit:

“The first is the 23.6% retracement, coinciding with the 50-DMA. This is the most logical support level for a short-term correction to reduce overbought conditions. If more selling pressure comes to bear, then the 38.2% retracement, which was also the break out of the short-term consolidation heading into December, should provide support. The 50% retracement is the least likely at the current time. However, it will most likely be tested during a deeper correction back to the 200-DMA this summer.”

The MACD “buy signal” is firmly intact, although at a high level, suggesting the bullish bias remains. While the market is overbought in the short term, corrections will likely remain mild with 4800, where the market broke out, remaining essential support.

The ongoing advance remains within a trend channel from the October 2023 lows. We continue to recommend maintaining exposure to equity risk, but be aware the current advance is getting rather long concerning time. As stated, the market will have a correction sometime over the next few months. Such will provide a better entry point for increasing exposure.

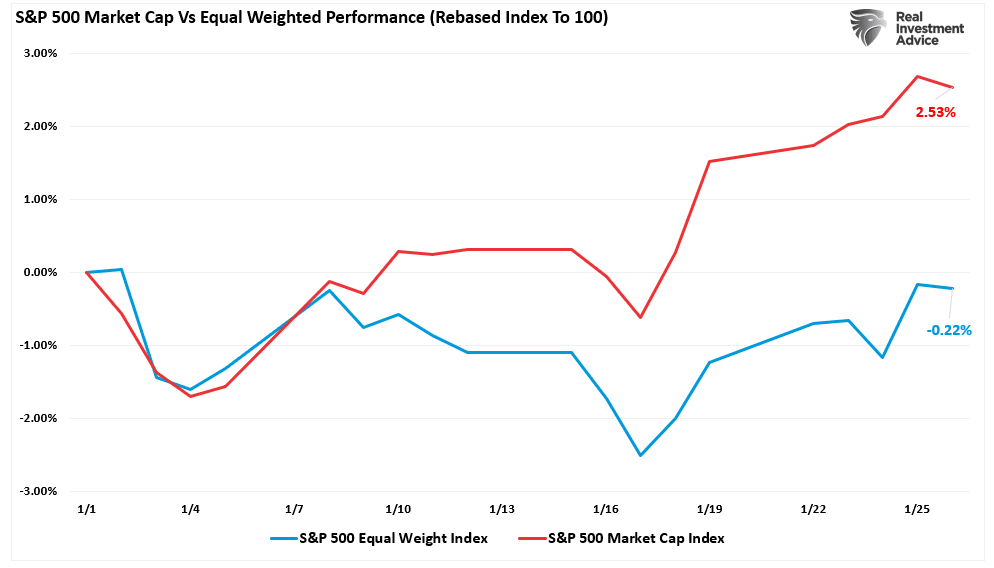

Nonetheless, the market continues its advance, but as we showed last week, it is back to the Mega-caps leading the way, with everything else lagging.

I am unsure what eventually causes the rotation, but one will occur. Hopefully, more defensive positioning will reduce portfolio volatility when that correction occurs.

The Week Ahead

There is a lot of news and data for investors to digest this week. On the economic front, JOLTS, ADP, and the BLS labor report on Friday will update us on the health of the labor markets. Given that jobless claims remain historically low, we should expect relative strength in this set of numbers. However, seasonal adjustments will again plague the data, as post-holiday labor patterns can significantly affect the reports. We will also keep a close eye on the ISM Manufacturing survey. The New York, Philadelphia, and Richmond Fed regional surveys took a decided turn for the worse. Do they reflect a national trend, or is their weakness primarily related to activity on the East Coast?

The Fed meets on Wednesday. The market is pricing in a very slim chance of a rate cut. We also expect very little change to their statement and no policy actions. However, we will listen closely to Powell for his views on liquidity and what may portend for rate cuts and QT. The Fed has been informally discussing tapering QT. Accordingly, a more formal notice could come at this meeting.

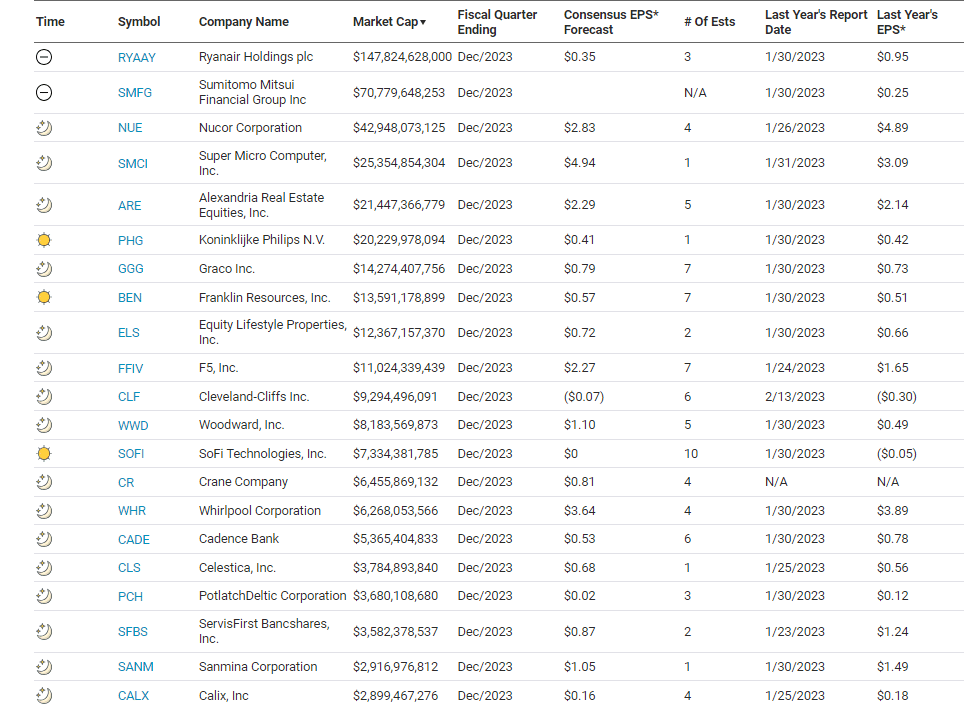

Earnings for some of the largest companies will be released throughout the week. As the graphic from The Transcript shows, Google, Microsoft, GM, MasterCard, Amazon, Apple, Meta, and Exxon, among many others, will report earnings.

PCE Inflation and GDP Prices

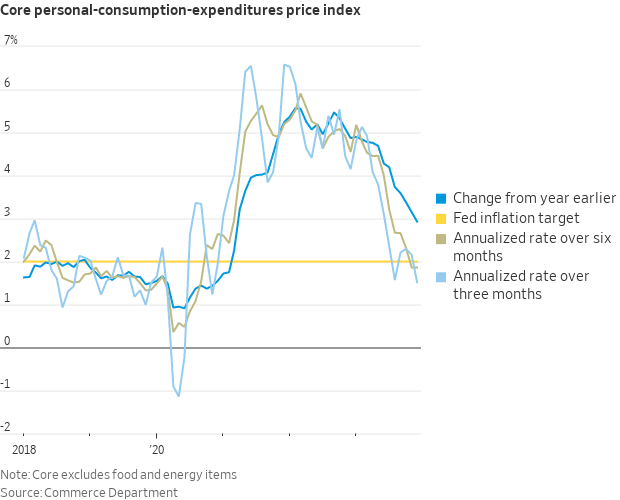

As expected, the Fed’s preferred inflation index, Core PCE Prices, rose 0.17% in December. This is the sixth month in the last seven, where monthly inflation has printed at an annualized rate equal to or below the Fed’s 2.00% target. While year-over-year core PCE inflation is still relatively high at 2.9%, the 6-month annualized rate is 1.9%, and the 3-month rate is 1.5% annualized. Similarly, as we wrote in the opening, the more recent data leads year-over-year data.

The PCE price index used to convert nominal GDP to the well-followed real GDP only rose 1.5% annually. That was much lower than expectations of 2.3% and the prior quarter’s reading of 3.3%. Consequently, real GDP beat expectations by 1%.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 5

2024/01/29