Just days after raising interest rates and starting QT, the Bank of England is taking aggressive actions to halt the recent surge in UK bond (Gilts) yields. As we show below, the yield on 10-year gilts has risen by over 2% in just the last two months. On Wednesday morning, the Bank of England cried uncle. It announced an emergency measure to temporarily buy long-dated gilts to attempt to stop yields from rising further. Simply, the bank is scared of financial instability. “To achieve this (financial stability), the Bank will carry out temporary purchases of long-dated UK government bonds from September 28.” Within the same statement, the Bank of England affirmed that its annual QT target of reducing its balance sheet by 80 billion is “unaffected and unchanged.”

Quite simply, the Bank of England will be conducting QE and QT simultaneously. Desperate times call for desperate measures!

What To Watch Today

Economy

- 8:30 a.m. ET: Initial Jobless Claims, week ended Sept. 24 (215,000 expected, 213,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Sept. 17 (1.385 million prior)

- 8:30 a.m. ET: GDP Annualized, quarter-over-quarter, 2Q third (-0.6% expected, -0.6% prior)

- 8:30 a.m. ET: Personal Consumption, quarter-over-quarter, 2Q third (1.5% expected, 1.5% prior)

- 8:30 a.m. ET: GDP Price Index, quarter-over-quarter, 2Q third (8.9% expected, 8.9% prior)

- 8:30 a.m. ET: Core PCE, quarter-over-quarter, 2Q third (4.4% expected, 4.4% prior)

Earnings

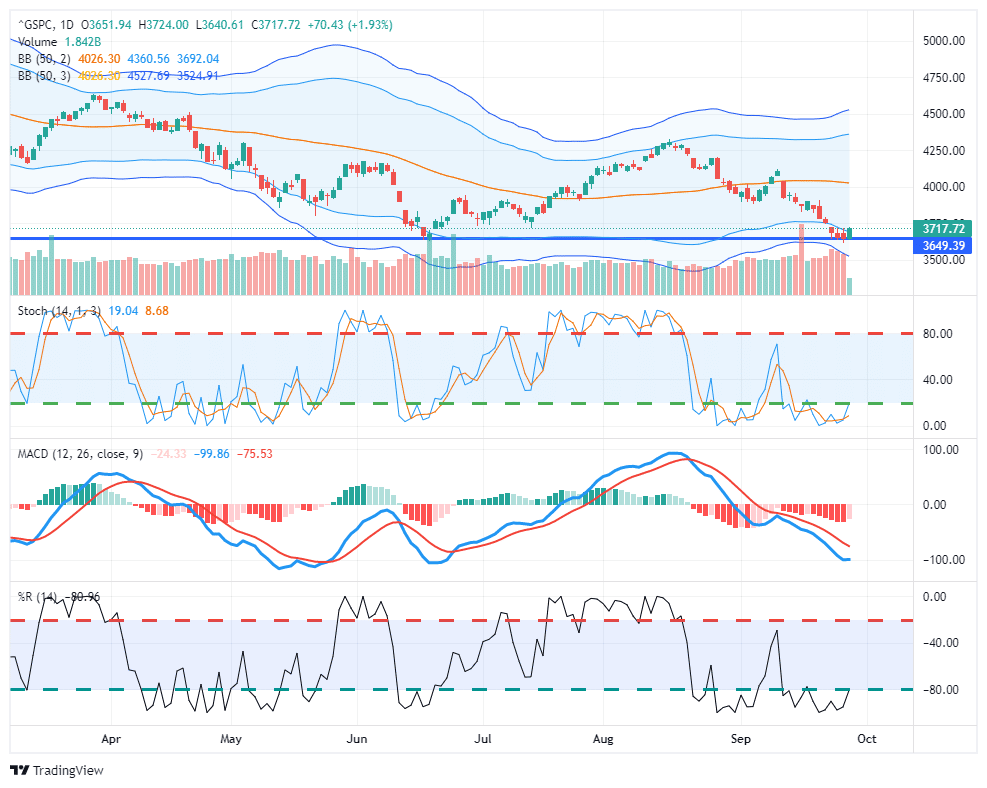

Market Trading Update

The markets were set to struggle at the open yesterday until the Bank of England reversed QT and stepped in to rescue both pension funds facing margin calls but a massive number of variable rate mortgages on the verge of repricing. As is always the case, “market instability” is a far more insidious risk than inflation, and the Central Banks will come to the rescue.

As such, pretty much everything rallied sharply yesterday, helping the markets hold key support. This is probably the beginning of that counter-trend rally we expected, and some follow-through is needed to confirm. The initial target will be approaching the 50-dma with the 3900-4000 level on the S&P 500 index. If the MACD turns onto a bullish buy signal, given the extreme negativity in the market, a rally could go further. However, we suggest using that rally to raise cash and reduce risk as we are likely facing another leg down before this bear market is over.

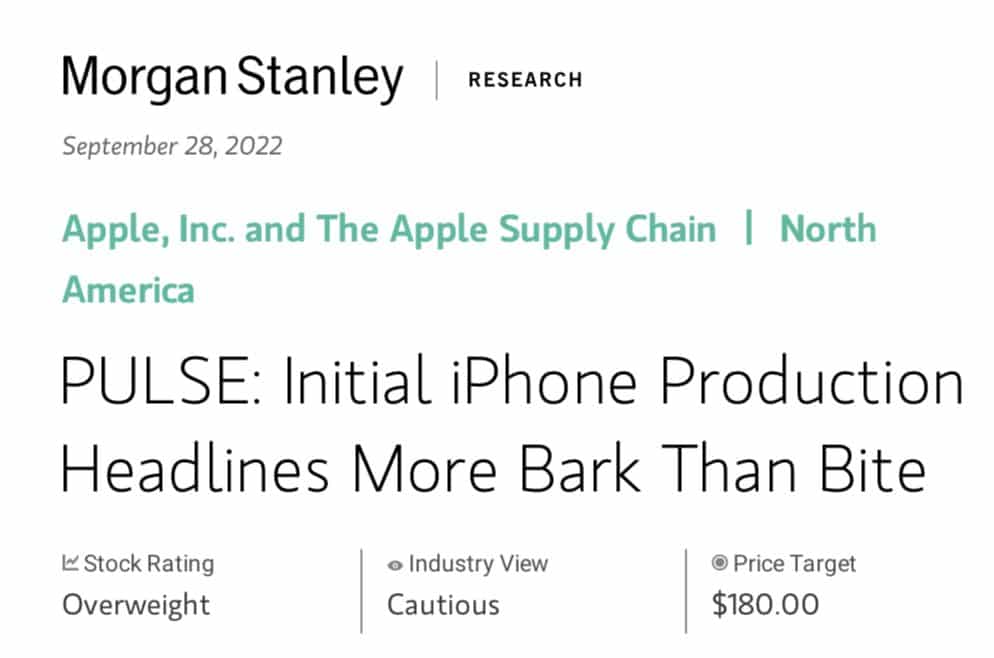

Apple Cuts iPhone Production

Apple stock traded lower yesterday after announcing it is backing off plans to increase iPhone production due to weaker than expected demand. While the news appears bad, Morgan Stanley thinks it is “more bark than bite.”

suggests that the upside from better-than-expected iPhone 14 Pro/Pro Max demand is likely being offset by weaker initial iPhone 14/14 Plus demand. ..does not imply any downside to our iPhone shipment forecasts. – Morgan Stanley

Demand for its higher-priced new iPhone 14 Pro line is better than its entry-level versions. Our take- inflation is taking its toll on demand for cheaper phones as lower and middle-class consumers are struggling. At the same time, many of Apple’s wealthier clients are still in good shape.

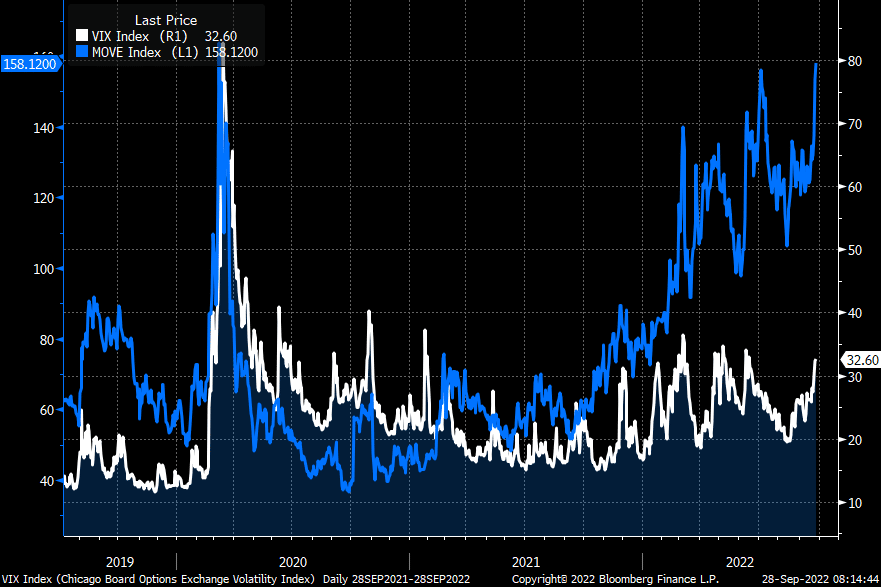

Stocks vs. Bonds- Volatility

The graph below is very telling. As it shows, the MOVE index is similar to the VIX, except it measures bond volatility. Bond volatility is approaching the high water mark from the initial shock of the pandemic. At the same time, stock volatility (VIX) is high but well below the pandemic highs and less than quite a few instances over the last two years. Typically, the correlation between the two indexes is strong. We must ask whether bond volatility will fall back in line with the VIX, or will equity market volatility play catch up to bonds? The graph argues an allocation toward bonds from stocks may be an intelligent rotation.

Corporate Profit Growth Will Slow

Yesterday we published Corporate Profit Growth Will Slow, Says the Fed. The article looks at corporate profits and profit margins. The article’s simple conclusion is that corporate profit growth will likely slow in the future. The article piggybacks on a Fed white paper that comes to the same conclusion. Per the Fed:

Over the past two decades, the corporate profits of stock market-listed firms have been substantially boosted by declining interest rate expenses and lower corporate tax rates. This note’s key finding is that the reduction in interest and tax expenses is responsible for a full one-third of all profit growth for S&P 500 nonfinancial firms over the prior two-decade period. I argue that the boost to corporate profits from lower interest and tax expenses is unlikely to continue, indicating notably lower profit growth, and thus stock returns, in the future.

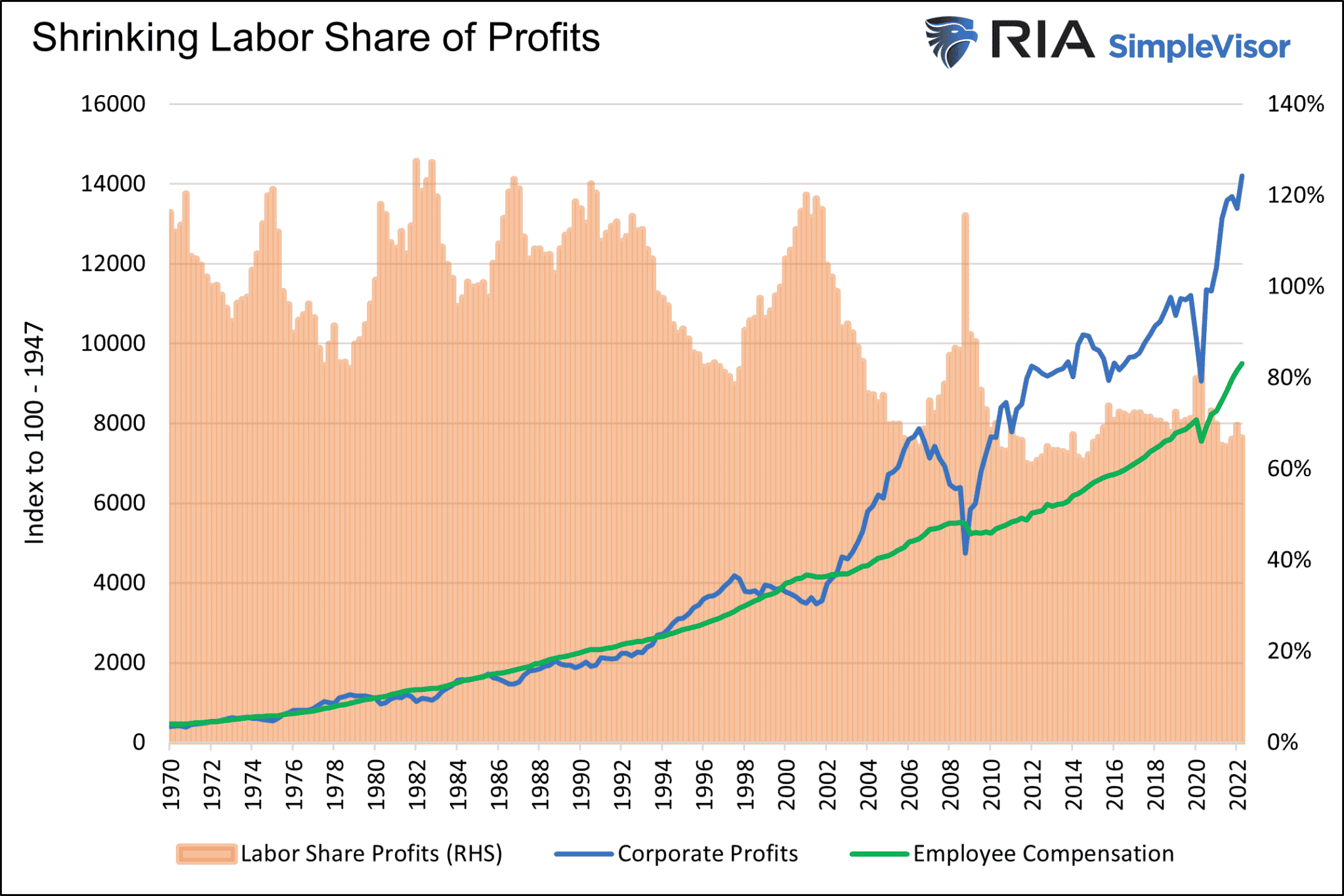

In our article, we take the Fed analysis and dig deeper. One of the factors further affirming the Fed view is rising labor costs. Therefore, as we share below, labor costs as a share of profits are set to rise from 50-year lows as de-globalization and less friendly immigration laws make labor more expensive.

The graph below shows that from 1970 to 2000, wages accounted for almost 100% of corporate profits. Over the last twenty years, they averaged 77%.

The summary from the Fed paper:

The overall conclusion, then, is that—with the expected slowdown profit growth and the associated contraction in P/E multiples—real longer-run stock returns are likely to be notably lower than in the past.

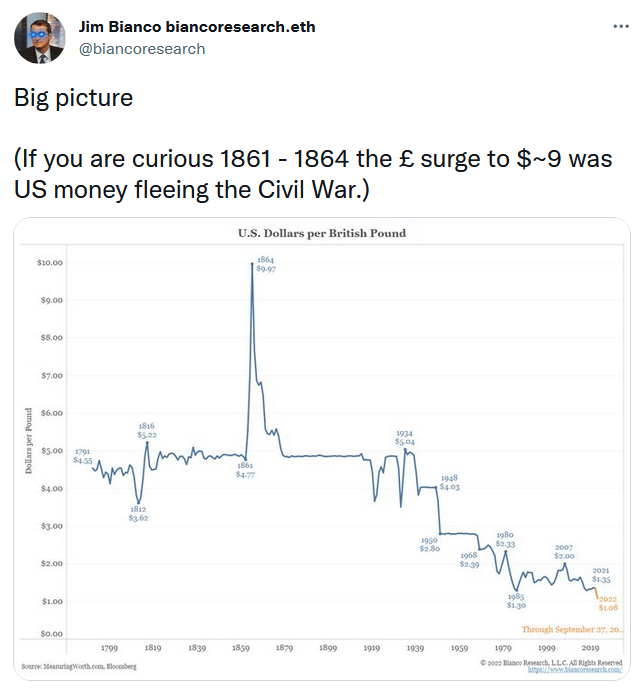

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.