🔎 At a Glance

- Technology Stocks: Dead or an Opportunity

- Market Brief & Technical Review

- From Lance’s Desk: The Reflation Narrative – RIA

- Market stats, screens, and risk indicators

🏛️ Market Brief – Market Volatility Returns

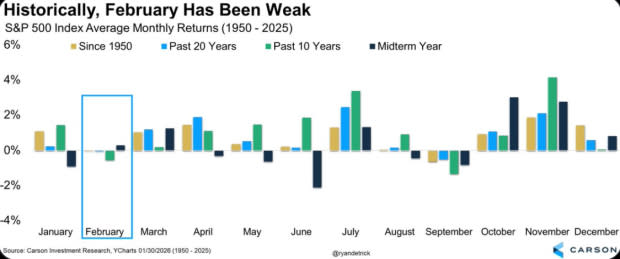

Markets stumbled into February, a historically weak month. February tends to deliver modest returns, with average performance trailing the stronger gains typically seen in January and March. Seasonal tailwinds, such as earnings season and new-year fund flows, begin to fade, while macro headwinds, such as tightening liquidity or policy uncertainty, often reemerge. February also lacks the retail-driven momentum of the holiday season, leading to lower volume and more volatile price action. Investors should be cautious, as February has a track record of chopping sideways or pulling back before spring’s broader recovery patterns take hold.

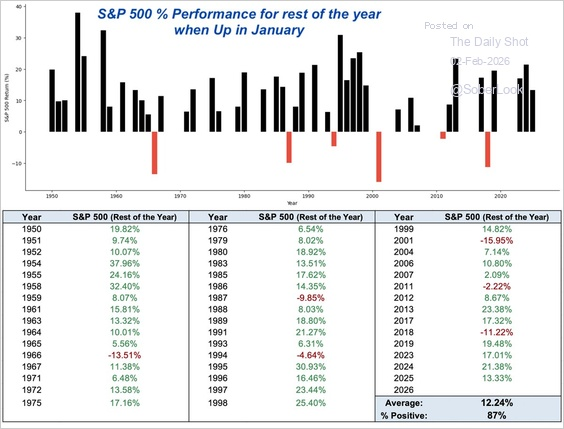

The good news is that both the first 5 days and the month of January were positive. As shown, when January’s performance is positive, the rest of the year has been positive 87% of the time. However, that does not mean there can’t be bumps along the way.

Returning our focus to this past week, it was Technology stocks that led the decline, along with precious metals, particularly silver, and cryptocurrencies. While headlines suggested a combination of earnings guidance and rising capital spending triggered the sharp reversal in sentiment, it was most likely margin calls from leveraged longs in the metals and crypto markets that bled over into the stock market.

While the decline in the technology stocks was notable, the earnings reports were very strong and certainly didn’t justify the price declines. For example, Alphabet (GOOG) reported solid revenue but shocked investors with a $50 billion AI capex plan. That raised concerns about future margins and capital discipline, leading the stock to decline by 6%. Amazon (AMZN) also exceeded earnings and revenue estimates by a hefty margin, with revenue rising 14%. But as with GOOG, the $200 billion capex commitment was noted as the reason for the 8% decline.

Another area of significant weakness was in Software, particularly SaaS stocks, which sold off hard. CrowdStrike (CRWD), Salesforce (CRM), and ServiceNow (NOW) were hit as investors trimmed exposure to high-multiple names. The liquidation across the technology sector was brutal and is likely far more extreme than forward expectations for growth and earnings justify, as the subject of today’s commentary.

Conversely, while tech stocks stumbled, capital rotated into value. Energy, Financials, and Industrials outperformed on a relative basis, and even small and mid-caps held up better. However, as we noted in our Daily Market Commentary, that push into value stocks is now grossly extended. Investors should consider taking profits and rebalancing risk.

The macro backdrop didn’t help, with the Fed sidelined for now and markets shifting expectations for rate cuts later into the year. Labor market data was also mixed, with fewer jobless claims and strong job openings, but ADP showed only 22K jobs in January. (The release of the BLS employment report was delayed due to the Government shutdown.)

Notably, while technology sentiment broke under the weight of earnings misses and rising macro uncertainty, the long-term backdrop remains unchanged. The recent selloff, like the many others we have seen in the past, is likely a reset, not a crash. Stay disciplined, manage risk, and let price and data lead.

Which brings us to the market.

📈Technical Backdrop – Technology Gets Tripped Up

As noted, the markets started February on a sloppy note. Leverage unwound fast once volatility spiked, and selling pressure hit crypto first, then metals, then equities. The sequence mattered as gold and silver broke sharply after repeated CME margin hikes tied to extreme price swings. Higher margin requirements forced traders to raise cash as margin calls mounted, and the fastest way to do so was to sell liquid positions. That selling spread into bitcoin, where leveraged longs liquidated aggressively as prices sliced through technical support near 65,000. Equities followed as cross-asset risk reduction took hold. This looked mechanical, not emotional.

However, on Friday, buyers once again “bought the dip” at the 100-day moving average, pushing stocks above initial resistance at the 50- and 20-day moving averages. That move keeps the bull trend alive and well, and the market continues its consolidation that began in November. Notably, investors were busy rebuying everything that got sold this past week, including metals and crypto. Heading into next week, the market will have to contend with resistance at the previous highs. Furthermore, given the recent selloff, particularly in metals, was so sharp, I would consider reducing risk on rallies as “trapped longs” look to exit. The next bottom will likely prove to be more lasting.

While the media was full of headlines about why selling was so broad across markets, the more likely explanation was that metals and crypto cracked, and systematic and risk parity strategies reduced exposure. The Nasdaq absorbed most of the damage as high-multiple software and AI-related names led the decline. By Thursday, price action showed signs of forced selling, with intraday ranges widening and volume rising on down moves. These patterns align with margin-driven liquidation rather than discretionary positioning.

As noted, the change in tone on Friday was encouraging as the sharp rebound eased automated selling pressure. However, when forced sellers finish, prices often snap back quickly. Crucially, this does not signal a new uptrend, just a potential end to the first liquidation wave. There is now a much higher risk of another leg lower than a move higher. As such, traders should focus on levels, not narratives. Relief rallies fail often when resistance holds. Sustained upside requires volatility stabilization and tighter intraday ranges. If support holds early next week, consolidation becomes the base case. Failure at support opens the door for a second leg lower.

| Index/Level | Level (Approximate) | Notes |

|---|---|---|

| S&P 500 | 6932 | Friday’s closing level |

| Immediate Support | 6927 | 20-day moving averge |

| Intermediate Support | 6885 | Rising 50-day moving average, structural trendline |

| Major Support | 6799 | 100-day moving average |

| Initial Resistance | 7000 | Psychological level, tested twice in January |

| Major Resistance | 7076 | First Fibonnaci Extension Zone |

🔑 Key Catalysts Next Week

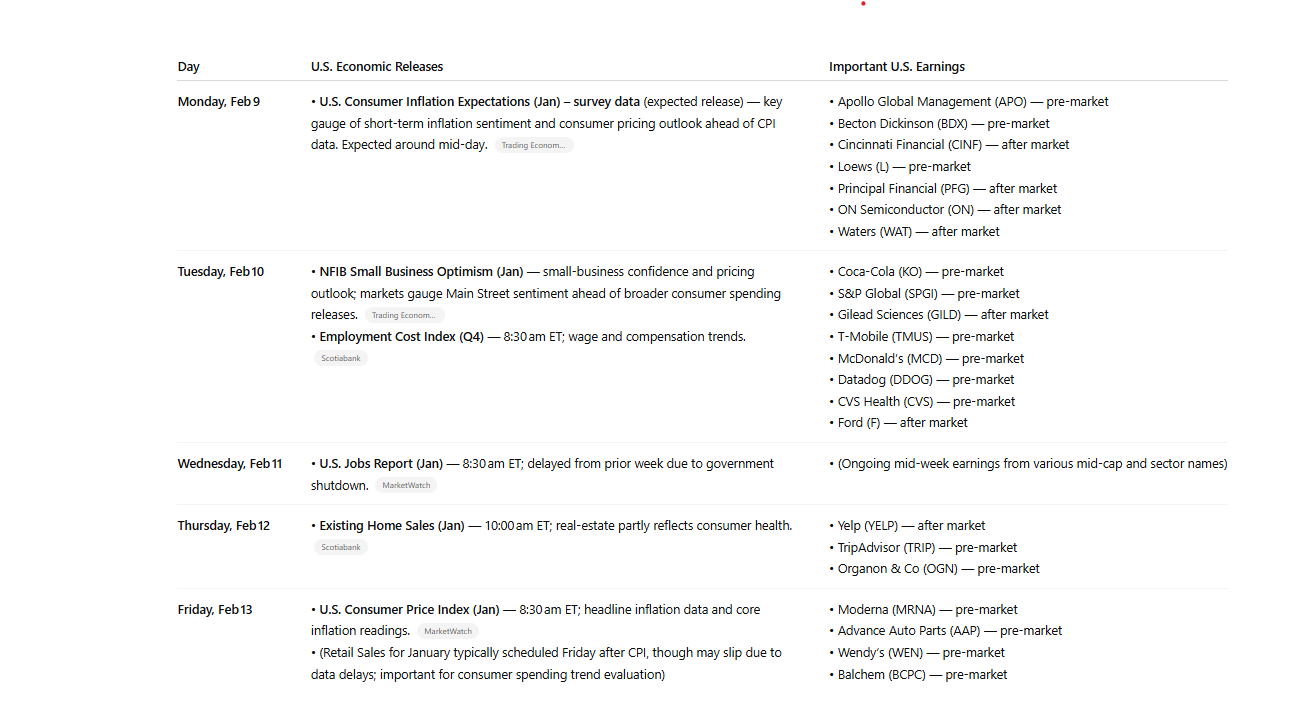

The coming week brings a heavy docket of economic data and earnings reports that could influence market direction, especially given last week’s volatility in Technology. First among macro catalysts is a shift in key U.S. economic releases: the Bureau of Labor Statistics rescheduled the January employment report to Wednesday, Feb 11, meaning investors will get updated jobs data midweek. The accompanying Consumer Price Index for January and real earnings figures are now slated for Friday, Feb 13, adding another potential market mover late in the week.

These inflation and wage measures will be closely watched for clues about consumer demand, pricing pressures, and the Federal Reserve’s future rate path. Broader macro data scheduled around the same period includes the Employment Cost Index and U.S. import/export price indexes on Feb 10, and existing home sales on Feb 12, all of which will add to the economic narrative. On the supply side, Treasury auctions continue throughout the week, which could influence bond yields and risk sentiment.

Earnings season resumes with a diverse slate of company reports that could shape sector leadership and sentiment. Early in the week on Feb 9, companies such as Apollo Global Management, Becton Dickinson, Arch Capital Group, Cincinnati Financial, and ON Semiconductor are expected to release quarterly results, offering insights into financials and tech hardware segments. Financial firms reporting include Principal Financial Group and Loews Corporation, which should help gauge the health of the banking and insurance sectors. Semiconductor companies such as ON Semiconductor could serve as a barometer for chip demand after recent headwinds in demand expectations and inventory normalization.

Taken together, the week’s data and earnings will continue to be parsed by investors, particularly the employment and inflation reports for signs of sticky price pressures or labor market resilience. At the same time, the earnings landscape will reveal how corporate America is navigating slowing growth, cost pressures, and capital allocation priorities. With volatility elevated and sentiment fragile after recent sector sell‑offs, this week’s catalysts could swing market leadership and risk appetite.

Need Help With Your Investing Strategy?

Are you looking for comprehensive financial, insurance, and estate planning services? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

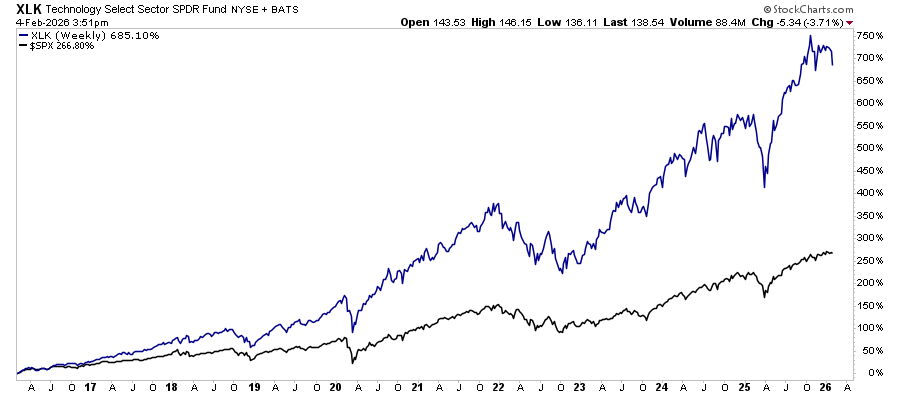

💰 Technology Stocks: Dead or an Opportunity

The narrative driving the recent sell-off in technology stocks centers on fear. Investors are fearing rising interest rates. They fear slower growth, a shift in economic conditions, and that “revenue generation” is likely not as robust as hoped. This fear has pushed many to reduce exposure to the names that have led markets higher for the last two years. While high valuations became a focal point, earnings outlooks changed, and prices reacted downward quickly.

Investors began to price in higher discount rates, thereby reducing the present value of future profits. Since technology stocks trade on future earnings expectations, changes to those expectations adjust valuations. This contraction triggered a wave of selling that metastasized into momentum selling, further fueling the decline. Many funds with risk controls were forced to liquidate positions, option contracts had to be unwound, and retail investors reacted to headlines, moving out of the sector. This created a feedback loop in which selling drove prices down, triggering more selling, putting pressure on the entire sector, and souring sentiment.

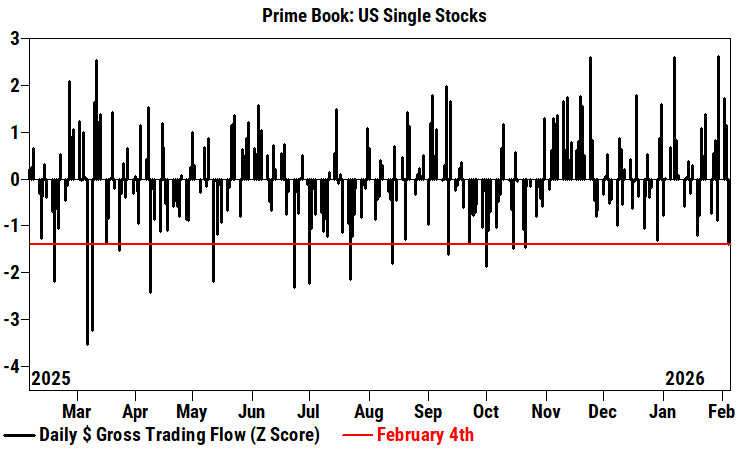

For example, as noted on Thursday,

“Hedge Funds net sold single stocks for a second straight session (5 of the last 6 trading sessions, -1.1 SDs one-year), driven mainly by long sales. While Wednesday’s de-grossing in US Single Stocks was the largest in more than three months (-1.4 Z score one year), it was not yet extreme (e.g., early March 2025) and relatively modest vs. the sharp price moves seen across multiple factors.” – Goldman Sachs

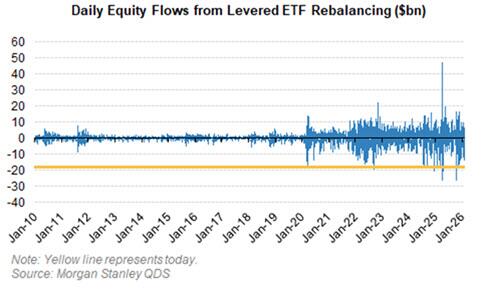

More notably, we have warned previously that the chase for levered exposure also “cuts both ways.”

“Finally, mechanical supply also exacerbated today’s moves and has the potential to do so going forward: Levered ETF rebalancing translated to roughly $18bn of US equity supply on the day — placing today in the top 10 largest levered ETF supply days on record, with a large share concentrated in NDX/Tech/Semis and meaningful single-name impacts (TSLA, NVDA, MU, PLTR, AMD, IREN each >$100mm).” – Morgan Stanley

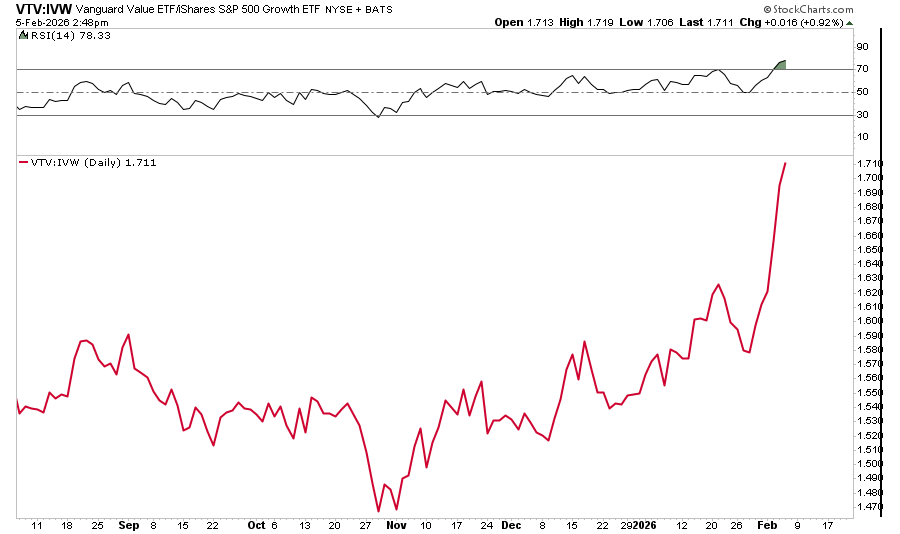

Another part of the narrative was rotation. We have written extensively about sector rotations and noted several months ago that the more extreme overbought conditions in technology would likely lead to a rotation toward value. That has occurred over the last two months in particular, with value stocks very overbought and technology, particularly the Megacaps, very oversold.

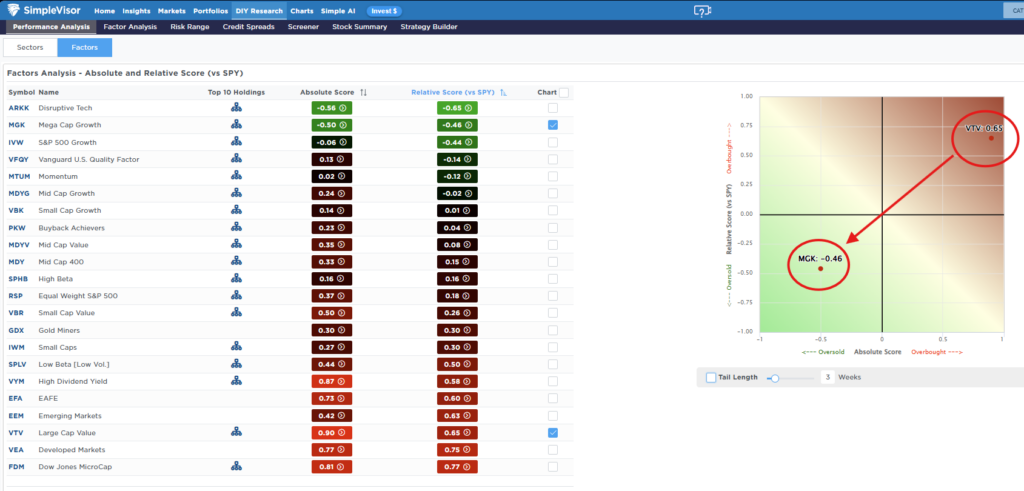

The rotation story suggested investors would find better returns outside growth stocks, and, as we discussed previously, when value was deeply out of favor, it was only a matter of time before that changed. The chart below is from the September 10, 2025, newsletter.

“The Low Beta Factor is the most oversold sector in the market on a relative basis right now, as High Beta, Momentum, and Gold Miners are extremely overbought. If the market corrects, we are likley going to see a rotation to low beta and value stocks for defensive positioning.“

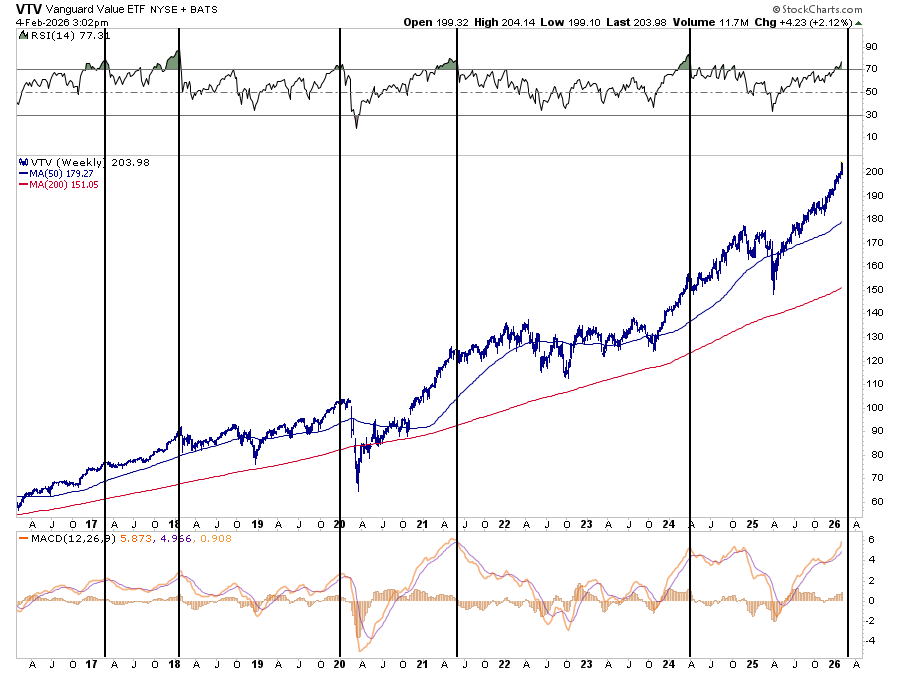

Note in that chart that MGK was extremely overbought and VTV was very oversold. Just the opposite of what we see currently.

While the current “reflation trade” narrative has gained traction amid momentum, as shown, large-cap value stocks are now very overbought.

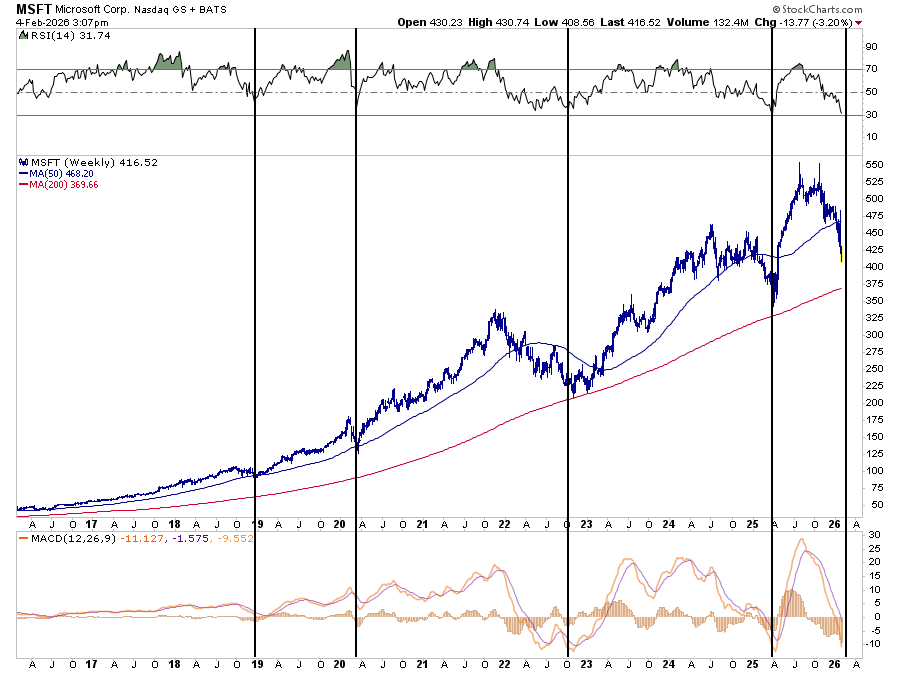

At the same time, many of the technology names have worked their way back to more oversold conditions. For example, Microsoft (MSFT) has only been this oversold a few times over the past decade. Each one of those periods was a good opportunity to gain exposure to the company.

This “technology is dead” narrative gained further traction as inflation data stayed elevated and rates rose. Unsurprisingly, as we noted last September, this increased the prospects for consumer discretionary and energy stocks, which looked more appealing under the “reflation” narrative and the fact that “everyone hated them” at the time. That shift began slowly as institutional players moved in, but as prices rose, retail investors began to chase them. Naturally, media headlines amplified this narrative. While the talk of the “end” of the technology rally spread, investors, as expected, reacted emotionally.

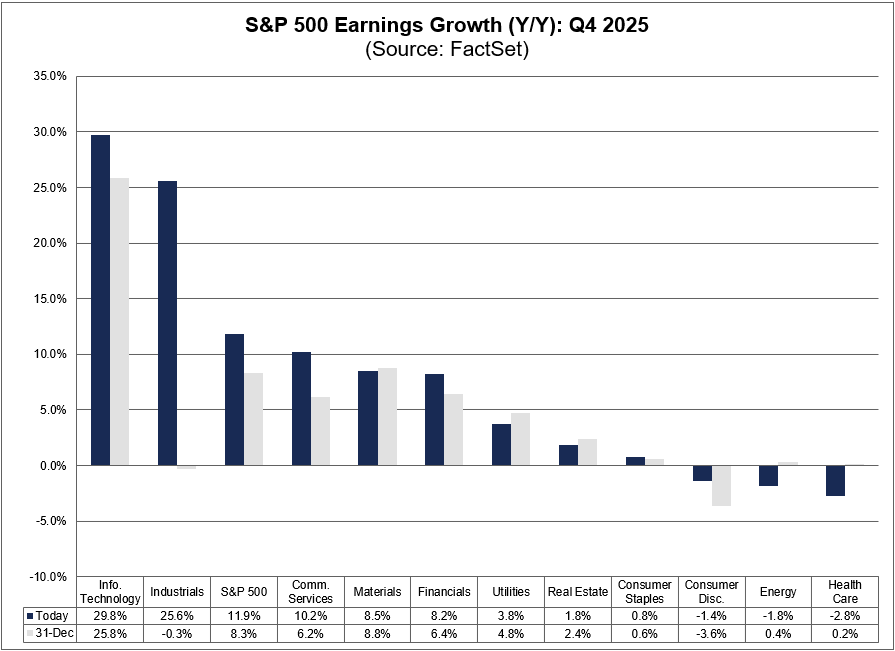

However, this fear narrative overshadowed the fundamentals. With the S&P 500 about midway through the Q4 earnings season, FactSet notes that technology is a leading contributor to earnings growth, particularly in the semiconductor industry. Technology also has the highest number of companies issuing positive EPS guidance for the quarter. However, just for comparison, while Energy and Staples have been the big winners in early 2026, they are also posting negative earnings growth.

In addition to strong earnings growth, technology companies also posted solid revenue and profit growth. Cash flow remained strong, and balance sheets stayed healthy, yet price action ignored these metrics as short-term traders focused on macro themes.

However, for longer-term investors, an opportunity may be presenting itself.

Fundamentals of Technology Companies

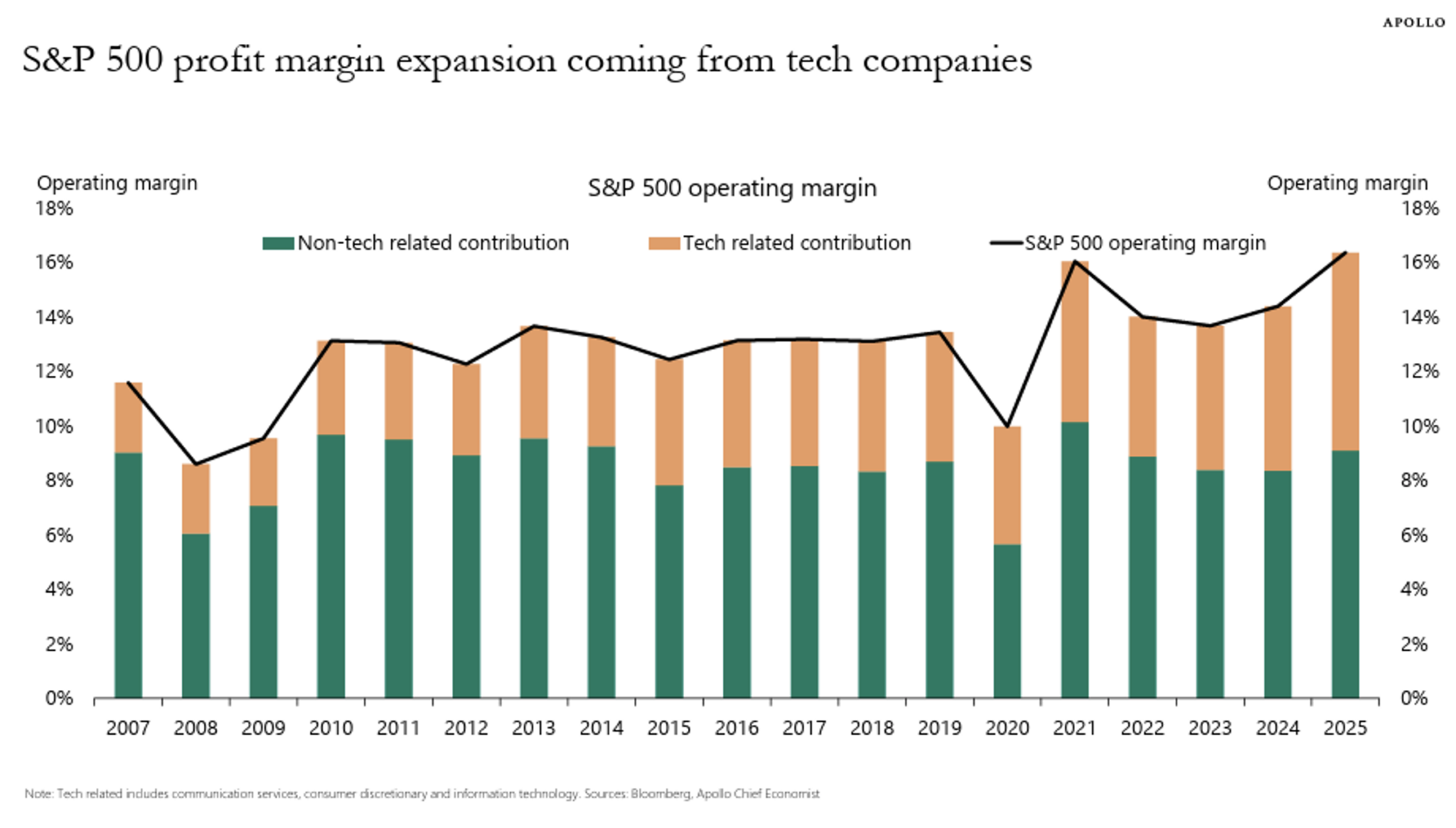

To evaluate the fundamental case, we must look at earnings growth, cash flow, innovation, and competitive advantages. Many technology companies delivered record revenue growth over the last several years, and profit margins have increased notably over the past 3 years. Furthermore, free cash flow generation among large technology firms still outpaces that of most sectors, and those same companies have strong balance sheets with significant cash reserves.

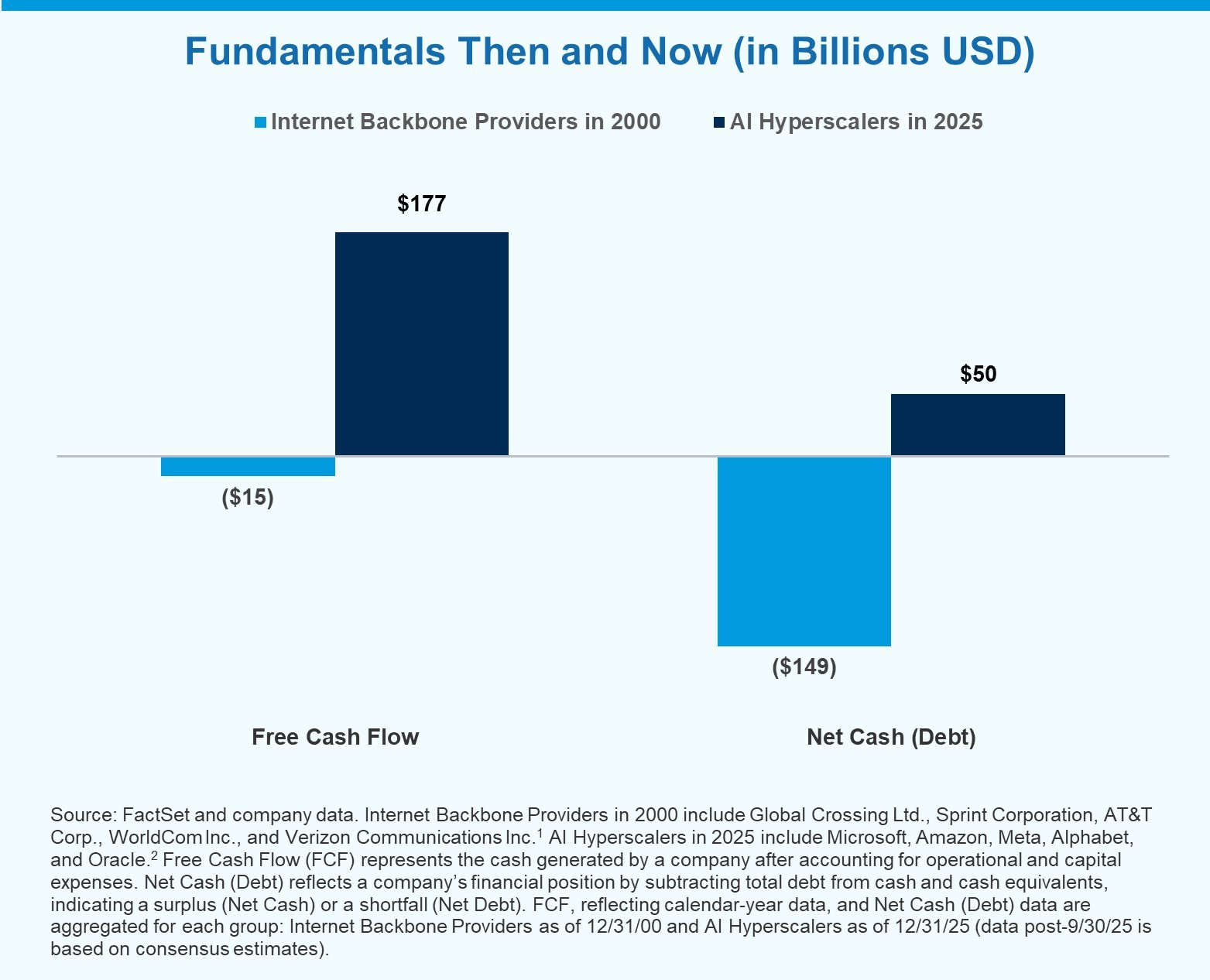

One of the rising concerns among investors with a more bearish outlook is the increase in debt taken on by Megacap companies to fund capital expenditures for data center buildout. However, as shown, those debt levels remain exceptionally low and very manageable, along with free cash flow, compared to the Dot.com bubble. At the same time, many are returning capital to shareholders through buybacks and dividends have increased in select names.

Innovation remains a consistent theme in technology. Artificial intelligence, cloud computing, digital advertising, and cybersecurity are expanding markets, particularly as demand for digital services has not waned. Enterprises continue to shift workloads to the cloud, consumers continue to adopt digital platforms for entertainment, communication, and commerce, and governments are increasingly investing in artificial intelligence and technology to modernize warfare. The secular trends supporting technology earnings have not reversed.

However, the recent market sell-off does reflect risk. As we noted previously, earnings expectations were exceptionally high coming into 2026, and they are moderating lower for some companies. Higher costs and slower consumer spending are impacting revenue projections, and there has been a broad revaluation across many names. That theme of “revaluation” has been the subject of many of our past commentaries over the last several months.

“Valuations also matter. As noted above, the current price-to-earnings ratio for the S&P 500 remains above historical averages, at approximately 22x forward earnings. Those valuation levels are also well above the five- and ten-year averages. In other words, the market is pricing in continued earnings momentum. Therefore, if growth slows toward historical norms or margins compress, elevated valuations will mean even modest earnings disappointments could result in share price declines rather than gains.”

This revaluation process, while painful in the near term, presents an opportunity for investors. This revaluation process will eventually end, and astute buyers will be looking for companies with solid fundamentals at lower valuations. As such, it is crucial for investors to separate the short-term sentiment from long-term fundamentals. For companies with durable competitive advantages, solid earnings growth, and strong cash flow, the sell-off may represent a mispricing.

Historically, technology has delivered superior long-term returns. Innovation has driven productivity gains across the economy, and companies leading in technology often expand market share during downturns.

Most notably, the future of technology is not decelerating; rather, it is accelerating rapidly. Yes, some of the winners today could very well be the losers of tomorrow; however, our job as investors is to sort that out. That is the job of a “contrarian investor.”

Contrarian Perspective on Accumulation

Howard Marks once stated that being a “contrarian” is tough, lonely, and generally right. To wit:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, particularly when momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’)

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

The problem with being a contrarian is determining where you are during a market cycle. The collective wisdom of market participants is generally “right” during the middle of a market advance but “wrong” at market peaks and troughs.

As such, a contrarian investor looks beyond the bearish narrative. When fear is high and prices are low, opportunity emerges. Such may indeed be the case, as the valuation adjustment continues to build for technology. Many technology stocks now trade at lower price-to-earnings ratios than a year ago, as well as price-to-cash flow, price-to-sales, and price-to-earnings growth. These lower valuations reduce downside risk and increase potential upside.

Often, contrarians ask whether the fundamentals truly justify the current valuations. In many cases, earnings growth remains intact, and the sell-off has punished quality alongside speculative names. This indiscriminate selling can create entry points for long-term investors, as buying during periods of fear often yields stronger returns in the future. However, this approach is not for the “faint of heart,” as it requires discipline and patience.

Furthermore, another contrarian support is market leadership. Technology has been a leader in innovation and earnings growth for decades, and that leadership is unlikely to disappear permanently. It may pause or shift temporarily, but it rarely disappears entirely, and investors who buy into a temporary weakness position themselves for future growth when conditions change. The key is identifying companies with clear competitive advantages, strong balance sheets, and sustainable earnings.

Yes, market sentiment matters in the short term, which could last weeks, months, or even quarters. However, fundamentals matter over the long term.

Risk Factors to Consider

I would be remiss not to state that running a contrarian strategy is not without risks. Contrarian investing can take quite some time to become profitable and can lead to longer-than-expected periods of underperformance. Furthermore, the economic or fundamental backdrop could worsen, such as a rise in interest rates that would negatively impact valuations. Higher capital costs could slow investment, or geopolitical risk could disrupt supply chains. Other factors could also weigh on outcomes, such as slowing consumer spending or restrictive regulation in technology markets. While these factors are not guaranteed, they must be part of any investment decision.

One area where investors do very poorly is distinguishing between cyclical risk and structural decline. Some technology segments face cyclical headwinds, while other segments have structural growth drivers. Understanding this difference helps prioritize where to allocate capital. For example, software businesses with recurring revenue may be less sensitive to macro swings than hardware companies dependent on consumer demand.

Furthermore, investors should:

- Monitor earnings reports.

- Watch guidance and revisions.

- Look for consistency in revenue and profit margins.

- Evaluate cash flow growth relative to capital expenditures, as healthy free cash flow provides flexibility. Companies with strong balance sheets can sustain investment through downturns.

- Dollar cost averaging into quality names reduces timing risk.

- Accumulating positions over several months smooths entry prices.

A disciplined approach helps an investor build exposure without attempting to time the exact bottom.

The recent sell-off in technology stocks was driven by fear and rotation. Short-term sentiment overshadowed strong fundamentals in many cases, even as technology companies continued to generate strong earnings and cash flow growth. From a contrarian perspective, lower valuations create a potential entry point for disciplined investors. Prioritizing quality, using a systematic approach to accumulation, and managing risk are essential. By following clear tactics, investors position themselves to benefit when sentiment improves and fundamentals regain focus.

Trade accordingly.

🖊️ From Lance’s Desk

This week’s #MacroView blog digs into the “reflation” thesis and provides a bull and bear case to consider as you allocate into 2026.

Also Posted This Week:

📹 Watch & Listen

A discussion of how the market functions and why there was an unsurprising snapback in commodities af the recent decline.

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

📊 Market Statistics & Analysis

Weekly technical overview across key sectors, risk indicators, and market internals

💸 Market & Sector X-Ray: Pullback To Support

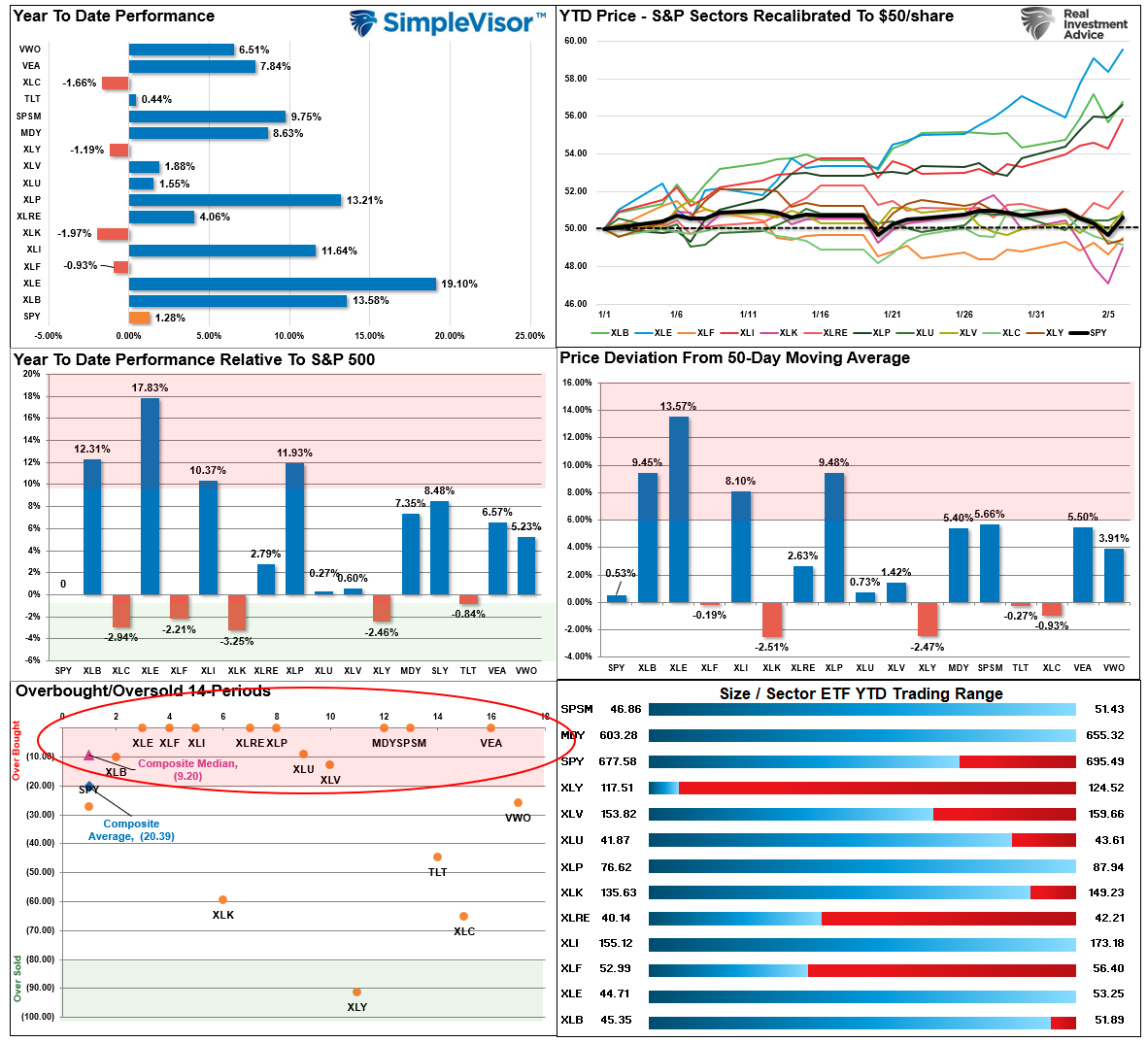

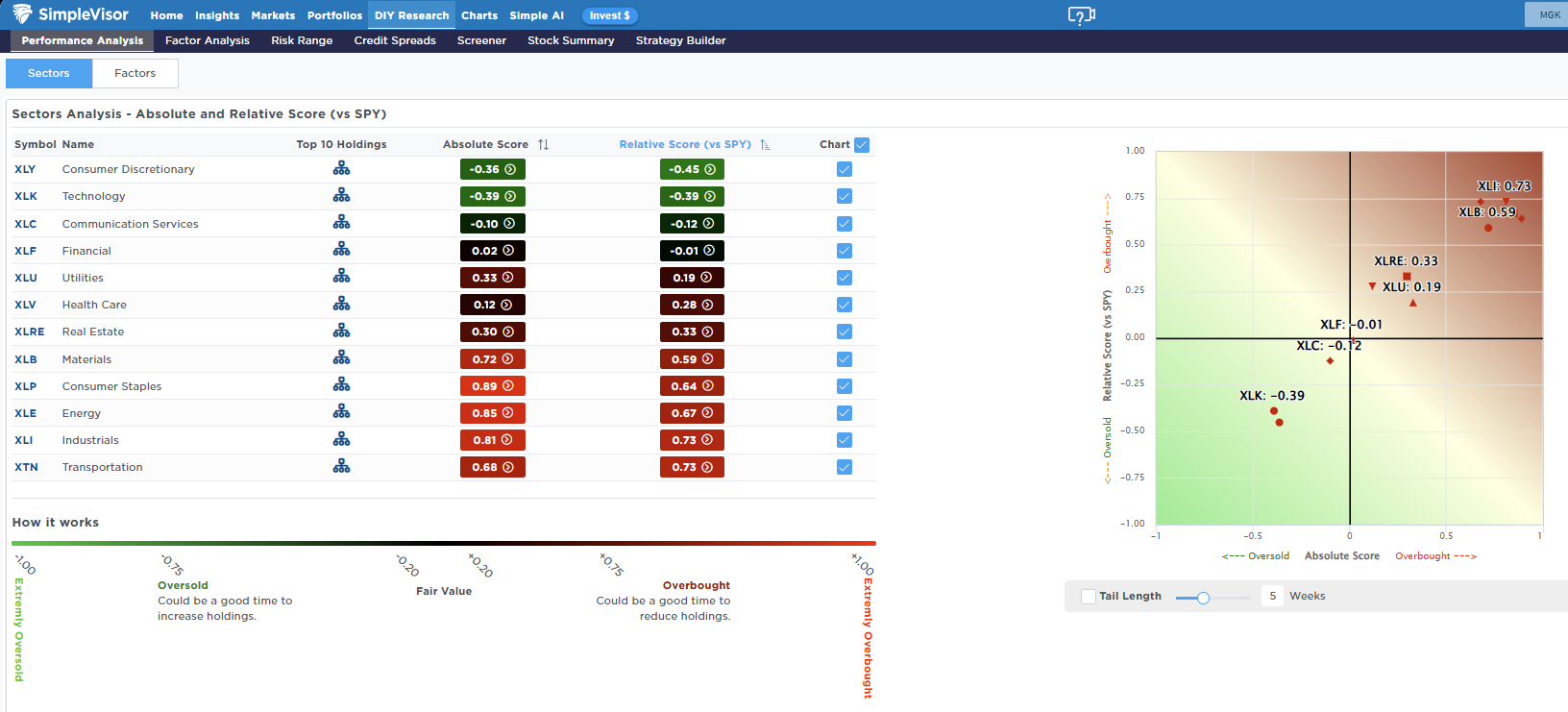

Despite what seemed like a rough week in the market, it really wasn’t as most sectors and markets, outside of technology, moved into very overbought territory on a short-term basis. Energy, Materials, Industrials, and Staples, or rather “value,” have strongly outperformed every other market and sector. These areas are the most overbought, and a rotation back to growth seems increasingly obvious.

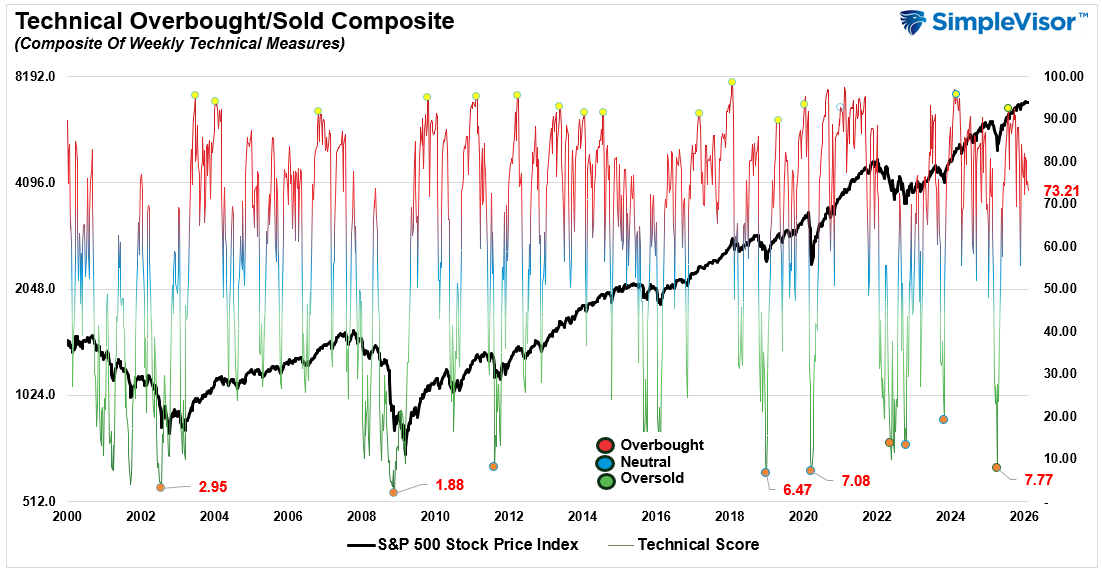

📐 Technical Composite: 73.21 – Bulls Still Optimistic

The overall technical condition remains bullish, but has weakened slightly over the last month. After hitting more extreme overbought conditions heading into October, the market has continued to consolidate, working off some of that state. While not bearish, some further weakness early next week would be unsurprising, providing a better entry point for a rally at some point.

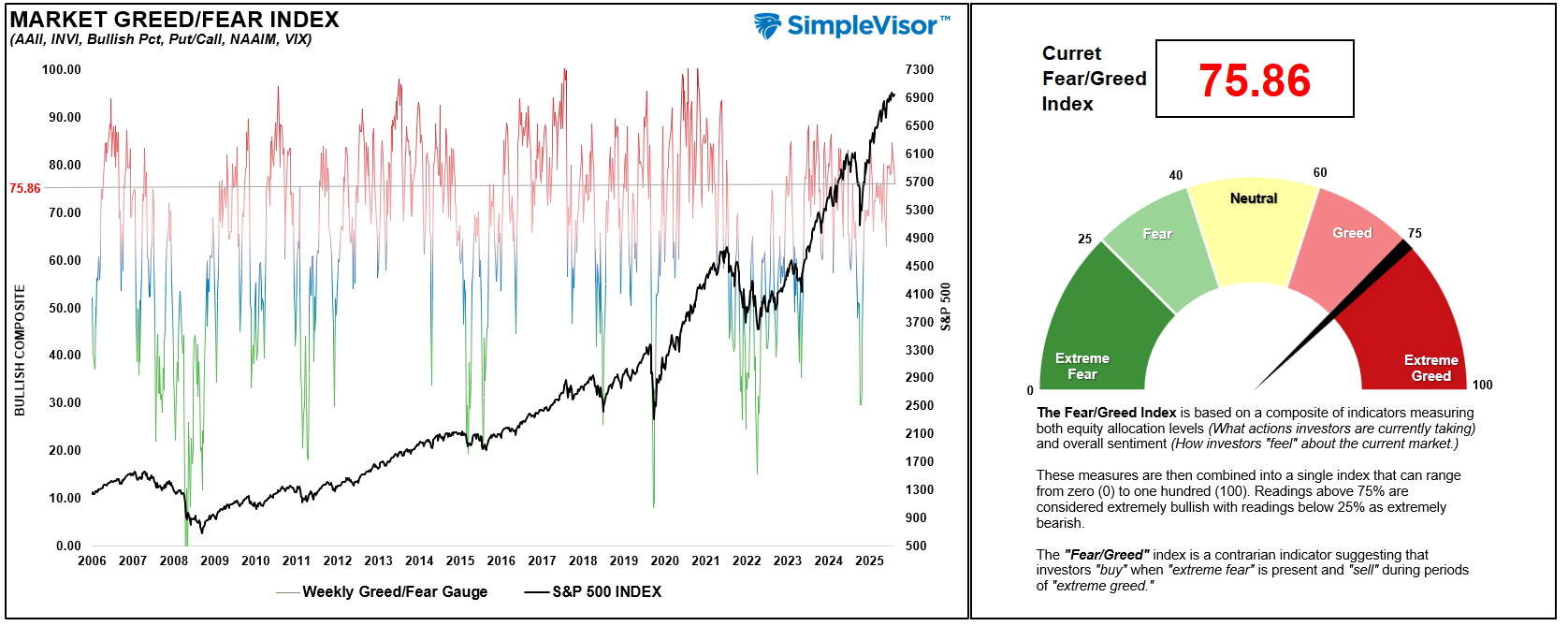

🤑 Fear/Greed Index: 75.86 – Extreme Greed Retreats

Positioning in equities remained strong this week, despite the relatively sloppy price action and the wreck in metals, technology, and Bitcoin. Overall, retail investors continue to remain aggressively invested, while professional managers slightly reduced net exposure this past week. We could see a further decline if weakness continues next week.

🔁 Relative Sector Performance

This past week saw a push into value early, sending Transportation, Industrials, and Energy into extreme overbought territory. Those sectors are now in prime territory to rotate back towards neutral in the months ahead. Take profits and rebalance risk accordingly.

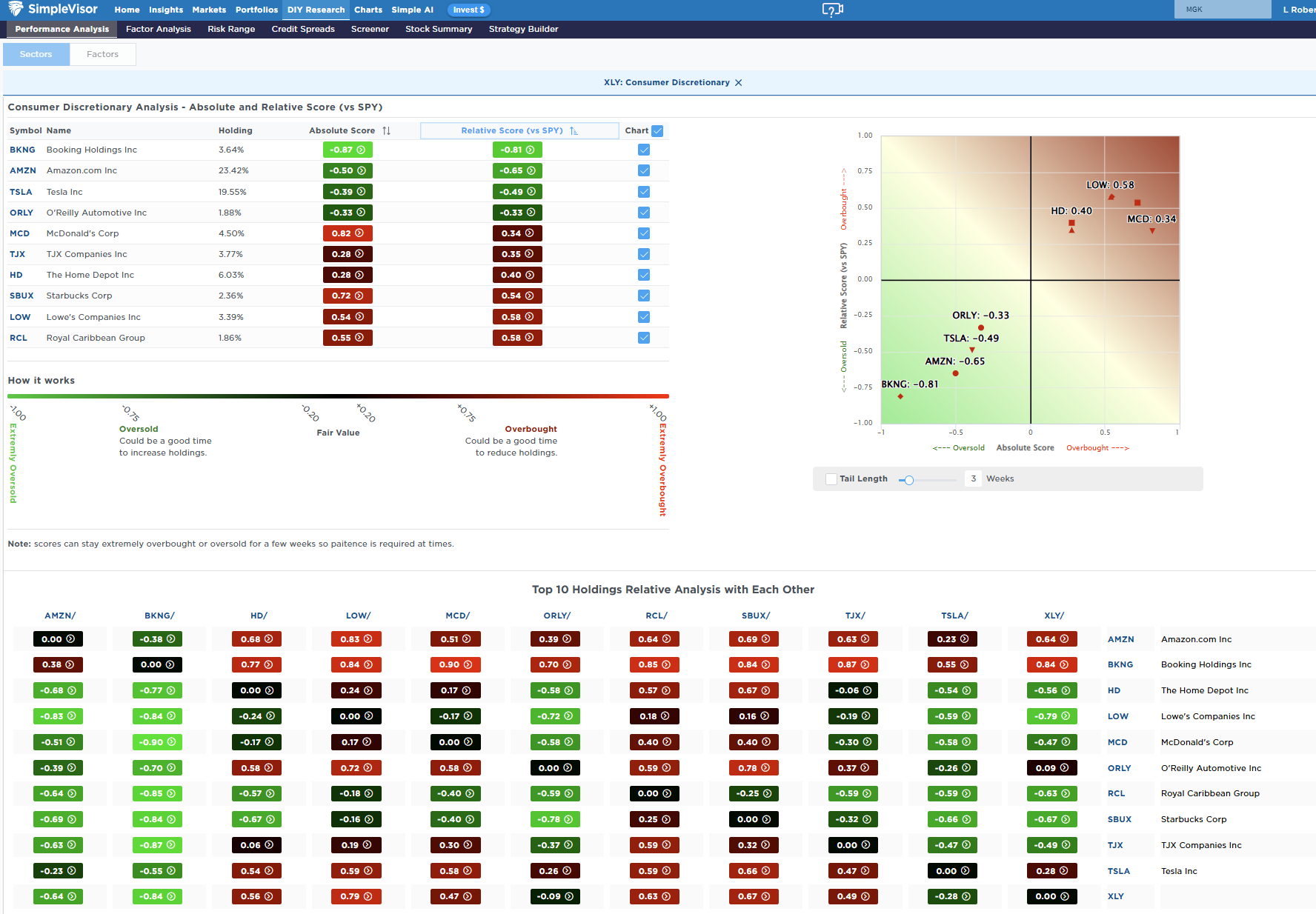

📊 Most Oversold Sector Holdings

Currently, the most oversold sector is Discretionary. Within that sector, BKNG, AMZN, TSLA, and ORLY are the most oversold companies, particularly after AMZN’s slide post-earnings on Friday. If we see a rotation from value back towards growth, these stocks should start to perform better.

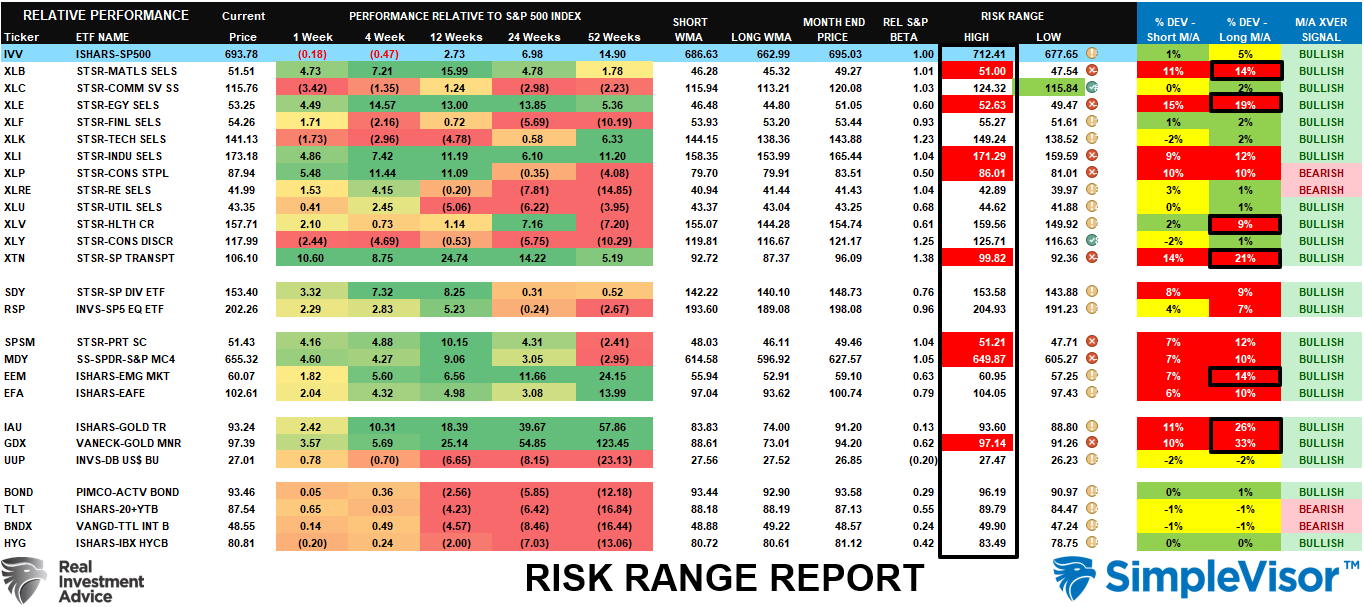

📊 Sector Model & Risk Ranges

Over the last month, we have noted a sharp advance in Basic Materials, Industrials, Energy, Transportation, Small and Mid-Cap, and Gold and Gold Miners, which pushed deviations from long-term means toward extremes that are ultimately unsustainable. This past week, we saw a minor reversion in those extremes, but most of those extremes still remain, suggesting continued risk in the period ahead. As we stated last week: “These extremes can persist for a while; therefore, it is important to maintain exposure while managing risk along the way.” That seems a prudent warning given the sharp reversal in metals and Bitcoin this past week. Investing isn’t risk-free, so continue to manage risk accordingly.

Have a great week.

Lance Roberts, CIO, RIA Advisors

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)