Google’s parent, Alphabet, just issued $32 billion in global debt, including £1 billion of rare century bonds. Alphabet’s century bonds are called such because they do not mature for 100 years (2126). While the century bond is a small piece of its recent debt offering and even less of its outstanding debt ($78 billion), the tranche secures ultra-long-term capital for a long time. On the small piece of debt, Alphabet insulates itself from future interest-rate cycles and the need to refinance debt at maturity.

Century bonds are typically issued when companies can borrow cheaply and, importantly, when investors are confident in the issuer’s durability. Buyers must believe the issuer will still be solvent 100 years from now. The strong demand for its century bonds, as evidenced by orders reportedly several times the offering size, signals that long-term institutional investors such as pension funds and insurance companies are bullish on Google’s prospects.

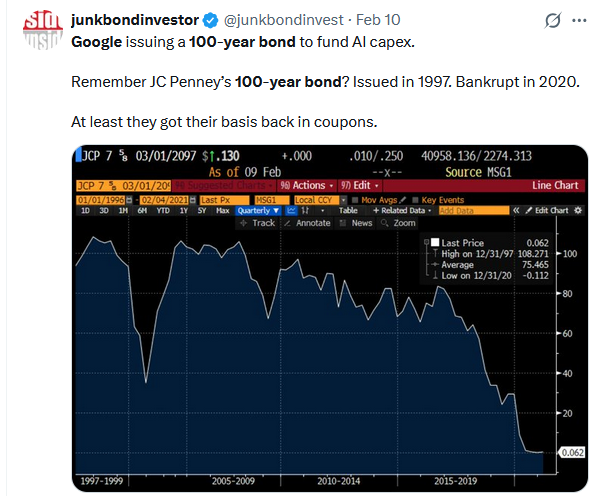

What makes the issuance notable is how rare century bonds are, especially for corporations. Ultra-long maturities are usually associated with governments or institutions like universities. Only a handful of major companies have issued them historically. In fact, Alphabet’s deal is the first century bond issued by a technology company since Motorola’s in 1997. The reason for the scarcity is risk. Over the course of 100 years, industries will transform, business models will vanish, and inflation can radically alter real returns. That is precisely why century bonds tend to appear only during periods of strong investor confidence and abundant liquidity, as we have today. The Tweet below serves as a reminder of what can happen over 100 years.

What To Watch Today

Earnings

Economy

Market Trading Update

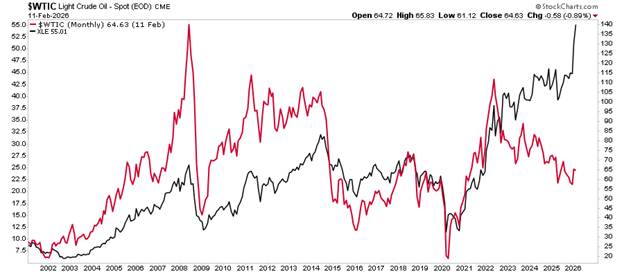

Yesterday, we discussed the potential for a rally in the US dollar and its impact on other assets, particularly those traded in US dollars. Continuing down that rabbit hole, oil also trades and is subject to the US dollar’s rise and fall. The non-correlation persisted until 2021, when speculative market activity took over.

However, what is more important is the price of oil itself. It should be evident that oil prices directly affect the profitability of energy companies. As such, energy companies should trade roughly in line with oil prices over time. As shown, over the 20-year period prior to the pandemic, that was indeed the case. However, since then, energy companies have risen far more than their fundamentals.

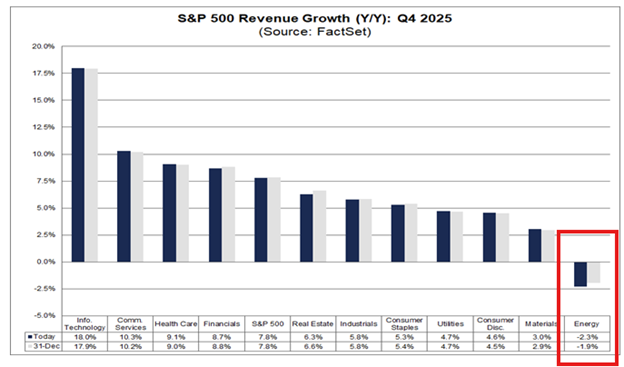

While the rise in energy stock prices may seem justified, the underlying revenue growth rate doesn’t support that conclusion. Moreover, revenue growth rates reflect the decline in oil prices, as expected.

As such, the rise in energy stocks over the last couple of years has been driven by multiple expansion rather than earnings growth. As such, many of the energy companies investors are currently chasing are no longer “value” stocks but are becoming rather expensive, particularly given the very low rate of earnings growth.

The surge behind these stocks is not surprising. We have seen markets chase one narrative after another into overvalued territory. This push into energy stocks will eventually end the same way. However, for now, the speculative momentum continues, suggesting that higher prices are possible. Just be aware of your risk-taking, rebalance regularly, and understand that, eventually, the price will revert to fundamentals.

Don’t get caught on the wrong side when that happens.

More On Employment

In yesterday’s commentary, we stated, “We are concerned that revisions to the BLS have been higher than normal.” Our concern is justified. To wit, accompanying Wednesday’s BLS labor report was its annual revisions. Per the BLS:

The seasonally adjusted total nonfarm employment level for March 2025 was revised downward by 898,000. On a not seasonally adjusted basis, the total nonfarm employment level for March 2025 was revised downward by 862,000, or -0.5 percent. Not seasonally adjusted, the absolute average benchmark revision over the prior 10 years is 0.2 percent.

The table below from the report shows that over the last 12 months, the BLS overestimated job growth by over 1 million jobs. Furthermore, and relevant to the Wednesday labor report covering January, there are large seasonal adjustments that are flawed. Accordingly, revisions for January tend to be larger than those for other months. As shown below, the BLS revised its January 2025 forecast down by 159k jobs. A similar revision to the current data would result in a negative number for January 2026.

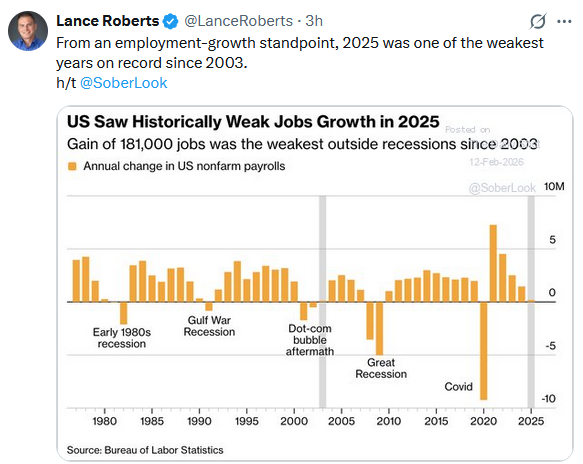

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.