Conditions Do Not Exist for A Weak Housing Market

The recent headlines from Real Estate analysts and pundits have been downright scary. If, however, one actually takes the time to read the article and pay attention to the conclusions, the prognostications are fairly mundane and some are actually positive. Below is a small sampling of recent headlines:

- Sellers are starting to freak out: Redfin CEO sees market slowdown – CNBC

- US Home Sellers Cutting Prices Hits Highest Level Since 2019 – Bloomberg

- List prices are finally starting to fall – Inman

Make no mistake, prices rising slightly, prices flat and/or prices declining in selected markets would be a huge shift from what we have seen for more than 2 years, but it will not mean a crash or even a significant decline in prices. We are not calling for either of those scenarios and we have not seen any other expert calling for that type of real estate environment. A different kind of market will necessitate adjusting expectations and utilizing different strategies for buying and for selling, but it will still mean a stable housing market, in which demand is still strong and outstripping supply in most of the United States.

In this article, we will take you through the data and reasoning, which shows that, regardless of 2 years of price rises and the recent historic increase in mortgage rates, historically low supply, historically high demand, and the unique nature of housing mean that the housing market will remain stable for the long-term.

Returning to the recent articles on housing for a minute, a careful read of the CNBC, Bloomberg and Inman articles includes the following statements that are a far cry from the threatening headlines:

- CNBC – “Buyers are saying ‘I’ve had enough,’ and sellers are starting to freak out a little bit,” Kelman (Redfin CEO) said. – Freaking out a little bit is not nearly as scary.

- Bloomberg – “…raising questions about whether the US housing boom has met its limit with signs emerging that the once-intense pace of the market could be decelerating.” A decelerating intense pace can still be fast.

- Inman – “Nearly 1 in 5 home sellers dropped their listing price in the four-week period ending May 22…” Of course, 1 in 5 is only 20%.

Meanwhile many others believe that high rates may cool the market a bit, but the supply-demand imbalance will still mean stabile or higher prices. This is what our analysis also concludes. Below are excerpts from recent articles:

- “After 2 stormy years of ‘moonshot’ house prices, don’t hold out hope for a major correction. Why COVID-era property values may be here to stay.” WSJ/Marketwatch

- “The Housing Market Boom Has At Least Another Year To Run, Zillow Economists Predict” Yahoo Finance

- “Over the coming 12 months, the Seattle-based real estate firm predicts that U.S. home prices will climb 11.6%.” Zillow housing forecast

- “CoreLogic predicts that U.S. home prices will rise 5.9%. If CoreLogic’s prediction comes to fruition, it would see a return to a historically normal rate of growth.” Corelogic housing forecast:

- “Zandi tells Fortune he expects U.S. home prices to be flat over the coming year…” Moody’s housing forecast.

The Current Housing Market

HOUSING SUPPLY

In any market, the reason that prices decline is more sellers than buyers. Prices cannot decline for long and usually not at all if there are more buyers than sellers.

We have repeatedly explained that the Financial Recession created a historic lack of housing supply in the U.S. The lack of housing is so serious that it will take years, if not decades to correct.

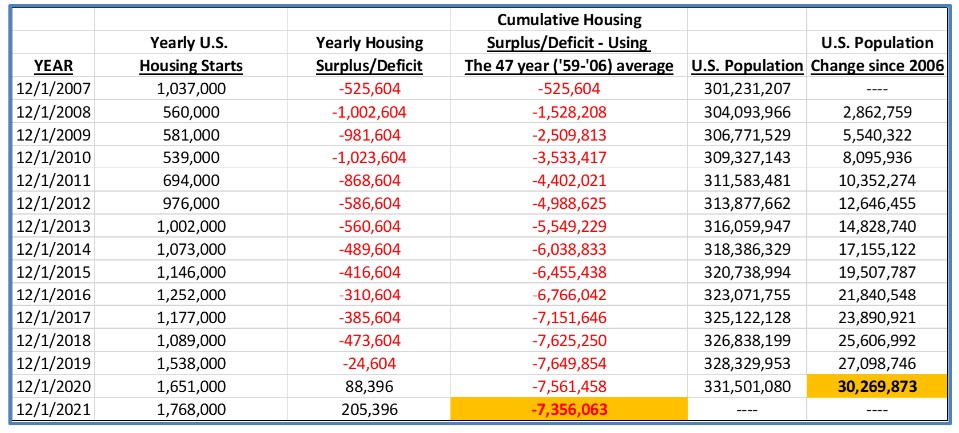

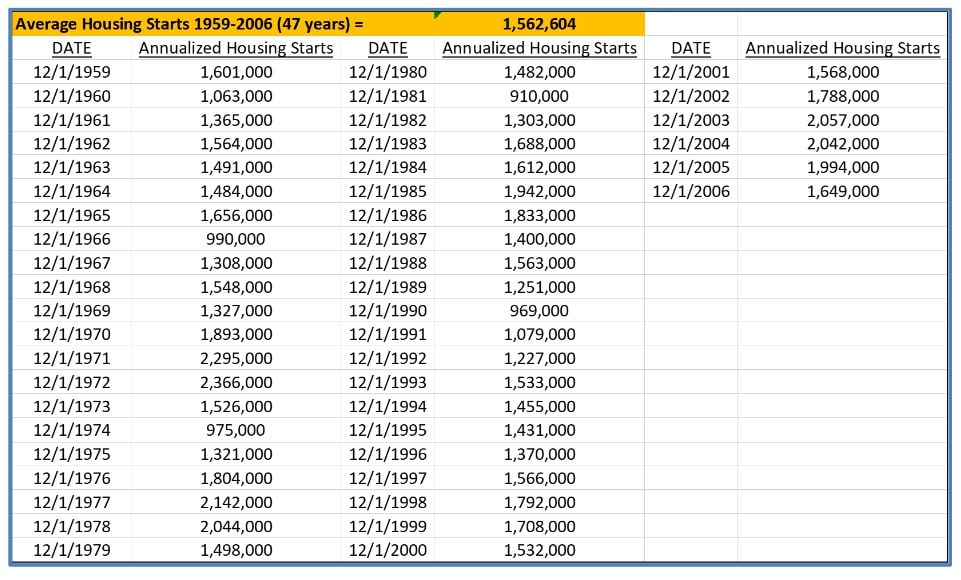

The table below shows U.S. Housing Starts from 2007 to 2021. Using the 47-year average annual housing start in the U.S. from 1959 to 2006 of 1,562,604 (see table 2), we have calculated the deficit of homes built in each year. We have also calculated a cumulative shortage of homes as the lack of construction following the housing debacle played out. By 2019, the cumulative housing deficit was over 7.5 million homes. To illustrate how severe this is, if we could sustain the housing start peak seen in 1972 of 2.36 million homes per year, it would still take over 9 years to get back to equilibrium.

In addition, as the lack of homes started has sharply declined since 2006, the U.S. population has grown by over 30 million people.

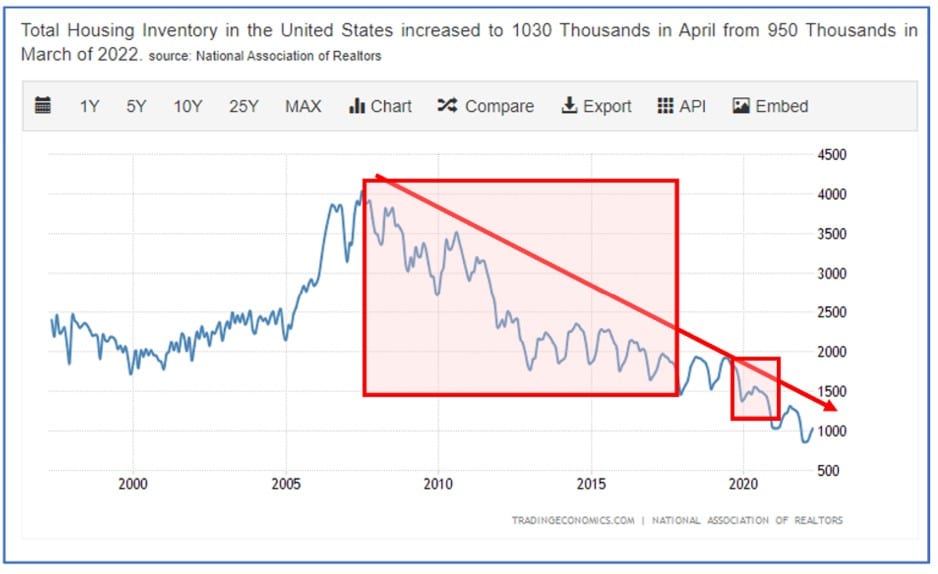

The chart below highlights the rapid decline in home construction in the U.S.

HOUSING DEMAND

The onset of the Covid pandemic in 2020 only exacerbated an already tight housing market. As people fled urban areas because of Covid, they were leaving locations where apartments and the ability to rent were plentiful. The initial fear of disease and the ability to work remotely rapidly turned into a desire for a more permanent lifestyle change. Working remotely is no longer reserved for a privileged few. Remote work holds out the promise of allowing more people to move further from cities. Housing away from cities is predominantly single-family units or houses.

The last two years saw the collision of 2 phenomena:

- A deficit of homes

- Greater demand for single-family homes.

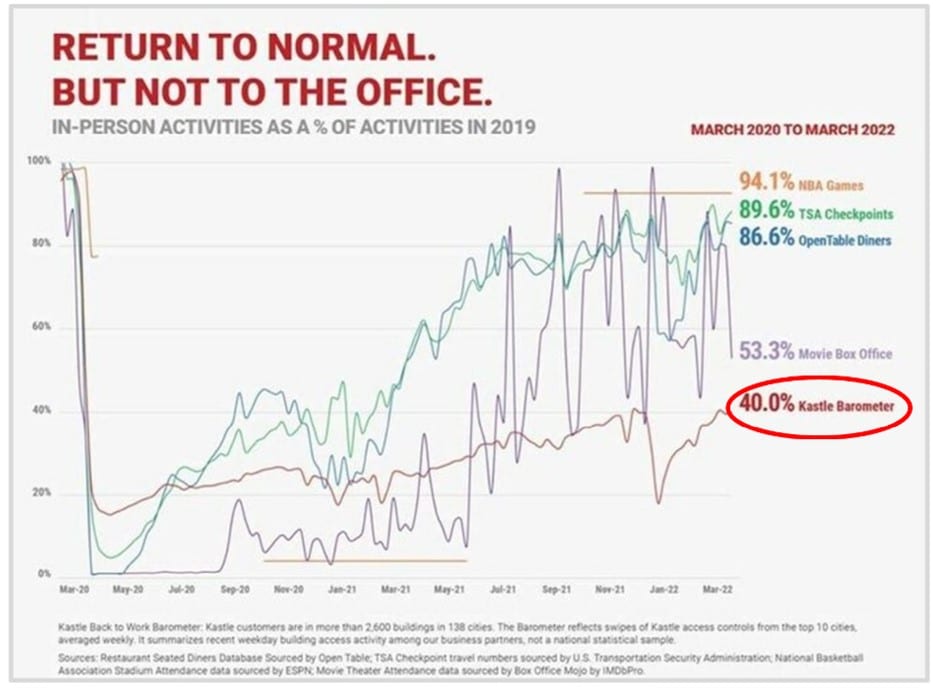

It does not appear as if this trend will end any time soon. Although some companies are expecting employees to return to the office, a large percentage have either not made any strict rules or they have committed to remote work. Remote work seems to be here to stay. In fact, a recent survey by Kastle, which has customers in more than 2,600 U.S. buildings in 138 cities, showed that average weekly office occupancy rates are still about 40% (see chart below).

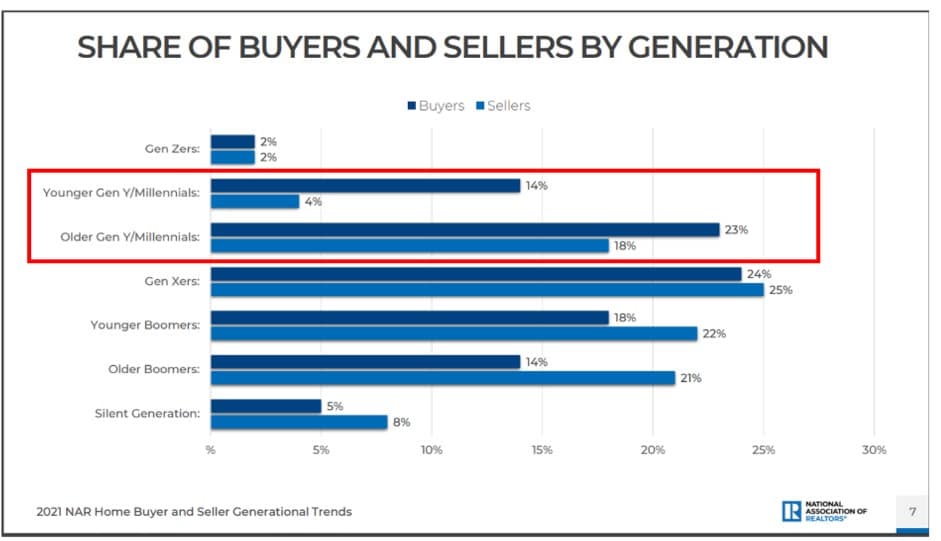

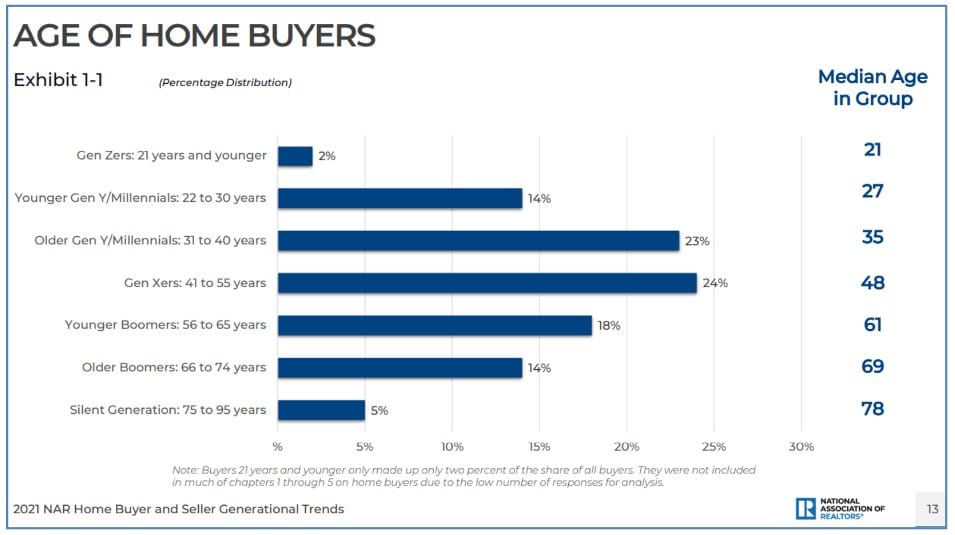

The most recent NAR 2021 Home Buyers and Sellers Generational Report gives an indication of where the housing demand is coming from and why it will be so persistent. The tables below show the percentage of buyers and sellers in every age category. Not surprisingly, younger people (21 – 40) are more likely to be buyers, while older people (41 – 95) are more likely to be sellers. This younger group is fast-growing and they are exactly the people who have left urban areas just as they start families and have the greatest need for housing.

HOMES ARE DIFFERENT THAN OTHER THINGS WE OWN

The NAR 2021 Home Buyers and Sellers Generational Report also provides some insight into the critical factors that drive home buying. Warnings about the housing market build their arguments on the idea that buyers will not buy because of high prices and high mortgage rates and that homeowners will be selling because of the recent historic price increases. This reasoning does not, however, make sense once we understand what motivates home buyers and sellers.

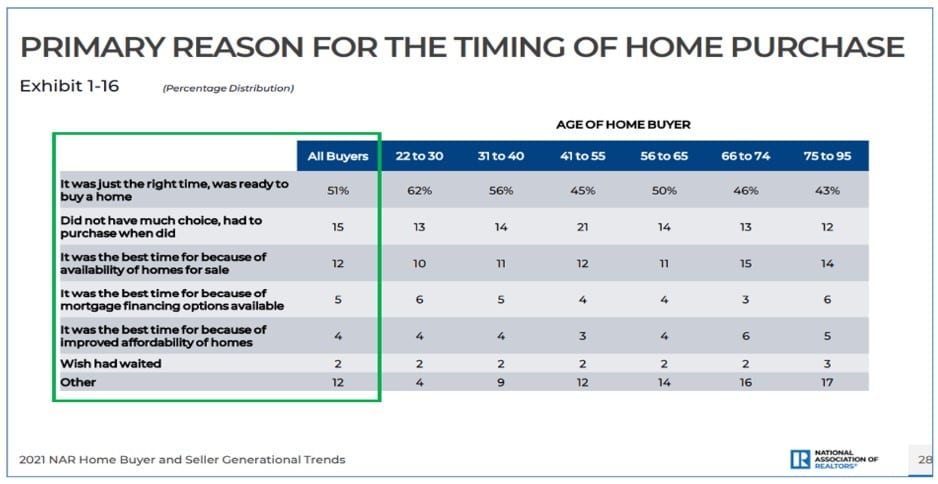

Mortgage rates are important, since the report explains that 87% of recent buyers financed their home purchase. However, only 5% of buyers said that their purchase was because “it was the best time because of mortgage financing options available”. In fact, the NAR table below shows that people buy because “it was just the right time, was ready to buy a home” (51%) or “did not have much choice, had to purchase when did” (15%). They also did not buy because home availability was good (only 5%) or because of “affordability” (only 4%).

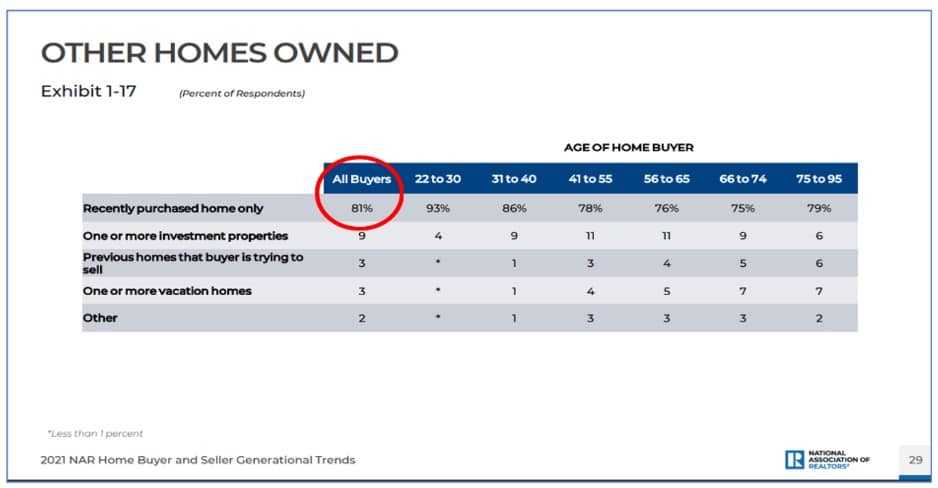

Some analysts have postulated that second home sellers would drive down prices, but the data would indicate that they will not be much of a factor in the overall housing market. 81% of buyers were buying their one and only home (table below).

A home is not like other things we buy. Armies of sellers are not going to materialize suddenly. If someone sells a home, they must find an alternative living situation. A seller must buy another home or rent unless they are moving in with a relative or pitching a tent in a park. So, no one is going to sell just because prices have gone up or due to a fear that prices will go down. In the end, they have to live somewhere.

Conclusion: Prices are high and mortgage rates are high, but those negative factors are more than overcome by a historic lack of supply and the mitigating factors of Covid/remote work demand and a growing young population who wants to buy a home. In addition, a home is a singular type of asset that cannot be functionally replaced. Until supply can be seriously increased, prices will either be stable or continue to rise.

Sources:

Jeff Marcus founded Turning Point Analytics (TPA) in 2009 after 25 years on trading desks and 13 years as a head trader to provide strategic and technical research to institutional clients. Turning Point Analytics (TPA) provides a unique strategy that works as an overlay to clients’ good fundamental analysis. After 10 years of serving only large institutions, TPA now offers its research services to mid and small managers, RIA’s, and wealthy sophisticated individuals looking for a way to increase their returns and outperform their peers.

Subscribe 2 Week Trial

Customer Relationship Summary (Form CRS)