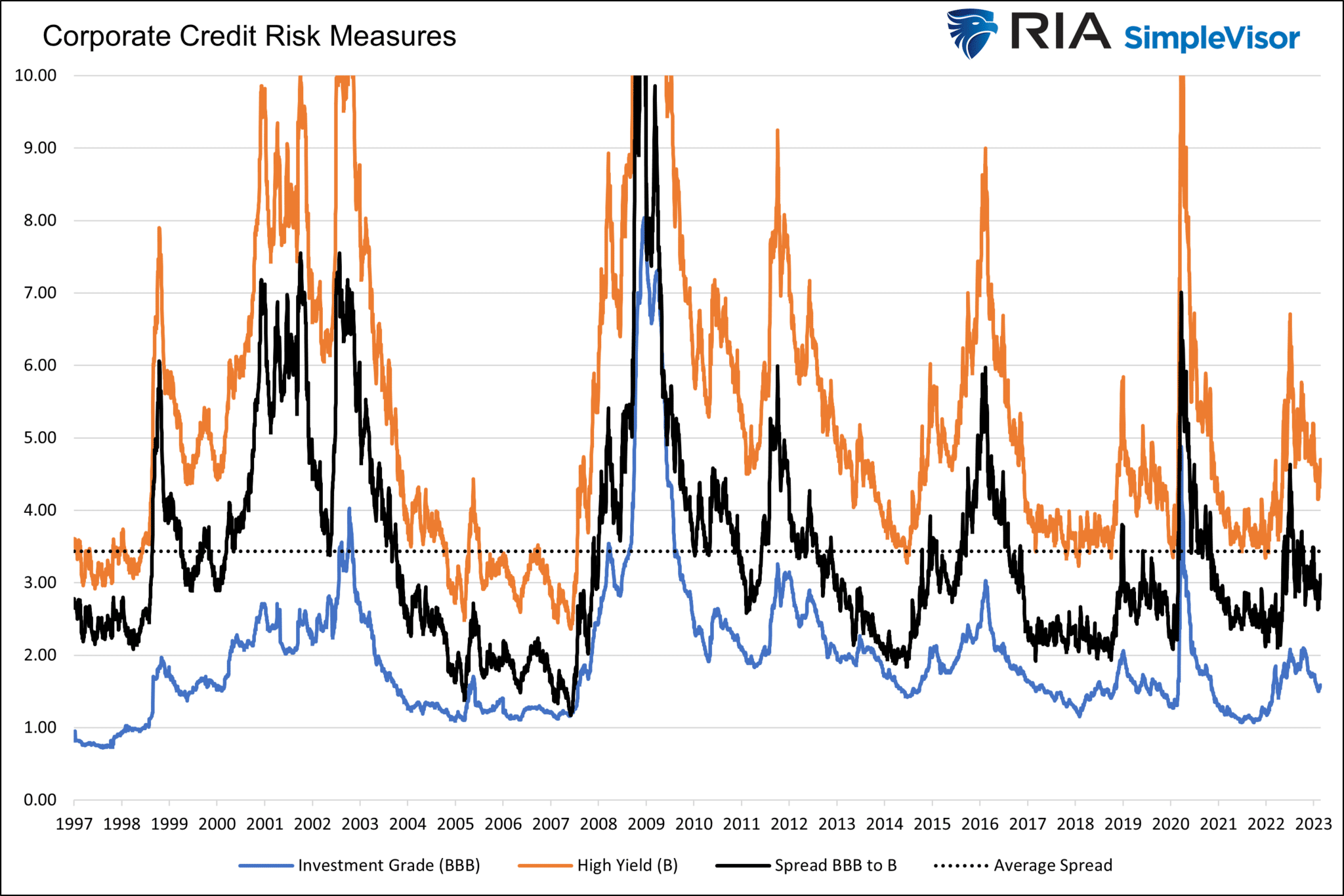

Tuesday’s Commentary led with a discussion of equity valuations and margins. Both are well above average, portending an elevated level of risk for the equity markets. As shown below, corporate bonds also exhibit no worries about a pending recession. The graph compares the yield difference between corporate bonds and U.S. Treasuries. The difference measures the risk premium for taking on credit risk. As it shows, investment grade (blue) and high-yield (orange) corporate bond yield premiums are within normal ranges. Further, the spread between riskier high yield and investment grade (black) is below the 25-year average (dotted black).

Higher interest rates will increase the number of defaults, especially for B-rated companies. Further, recessions tend to cause spikes in credit spreads. Therefore, the takeaway is that corporate bond investors have no concerns that either of these will occur. The term “picking up pennies in front of a steam roller “comes to mind when looking at the graph below.

What To Watch Today

Economy

- 8:30 a.m. ET: Personal Income, month-over-month, January (01.0% expected, 0.2% prior)

- 8:30 a.m. ET: Personal Spending, month-over-month, January (1.4% expected, -0.2% prior)

- 8:30 a.m. ET: Real Personal Spending, month-over-month, January (1.1% expected, -0.3% prior)

- 8:30 a.m. ET: PCE Deflator, month-over-month, January (0.5% expected, 0.1% prior)

- 8:30 a.m. ET: PCE Deflator, year-over-year, January (5.0% expected, 5.0% prior)

- 8:30 a.m. ET: PCE Core Deflator, month-over-month, January (0.4% expected, 0.3% prior)

- 8:30 a.m. ET: PCE Core Deflator, year-over-year, January (4.3% expected, 4.4% prior)

- 10:00 a.m. ET: New Home Sales, January (620,000 expected, 616,000 prior)

- 10:00 a.m. ET: New Home Sales, month-over-month, January (0.7% expected, 2.3% prior)

- 10:00 a.m. ET: University of Michigan Consumer Sentiment, February Final (66.4 expected, 66.4 prior)

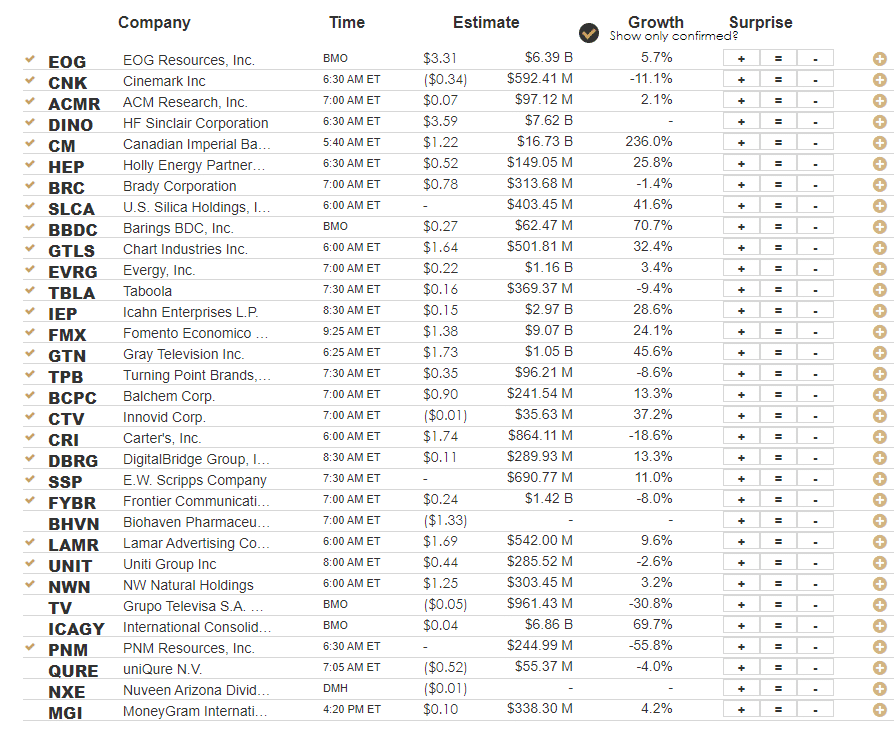

Earnings

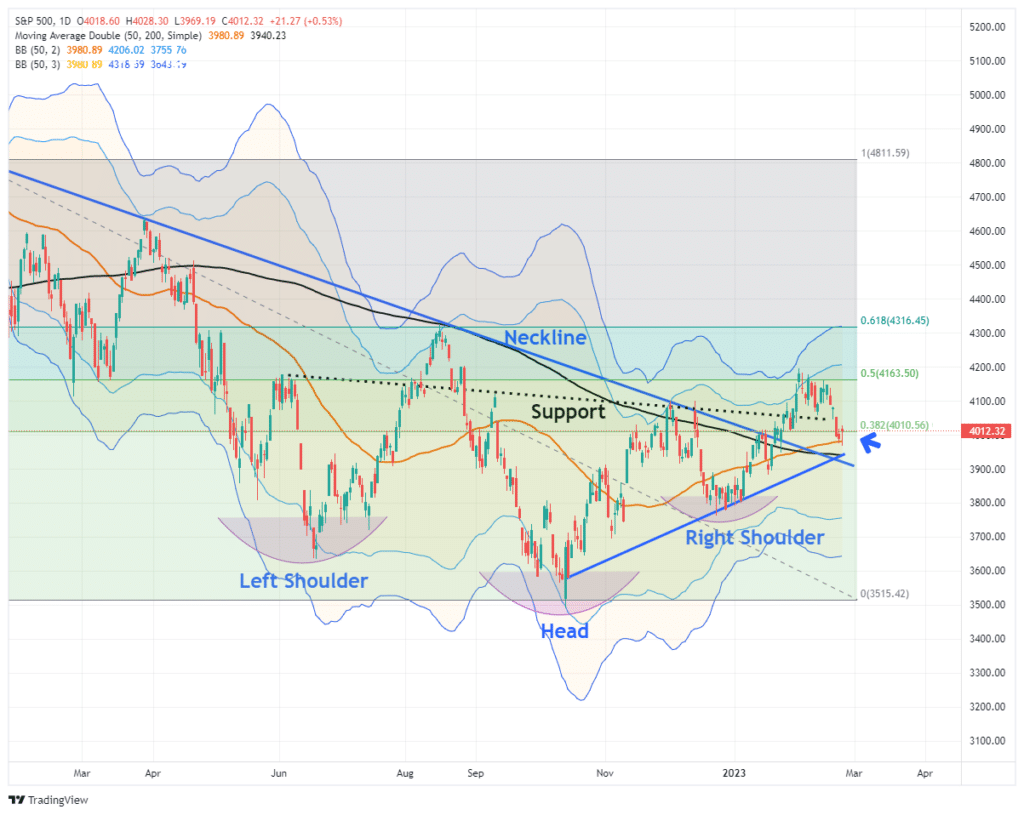

Marke Makes First Successful Test Of Support

Yesterday, as discussed in the Before The Bell video (subscribe for daily updates), futures pointed to a higher open, but I warned that such could quickly reverse. That was the case as the market sold off mid-day on a stronger GDP deflator (inflation) than expected. Such, of course, suggests the Fed will continue to hike rates further for now.

However, at mid-day, the market made its first initial test of the 50-DMA, initial support, and bounced nicely off it with buyers showing up to “buy the dip.” We are not out of the woods yet, with the MACD signal suggesting weaker market prices near term. However, after four days of declines a bounce is expected. We suggest using any bounces over the next week to raise cash and somewhat reduce equity exposure until the correction process is completed.

This morning, futures are lower, and as noted above, critical inflation data is coming out that could either be a boost or a drag. Importantly, critical support coincides with the 200-DMA, the downtrend line from the 2022 highs, and the rising trend line from the October lows. Those supports intersect around 3950, which is the make or break point for the bulls.

More Economic Data Affirms Higher for Longer

Thursday’s data will only bolster the Fed’s opinion that they must keep policy restrictive to weaken inflation. Fourth quarter GDP was revised lower to 2.7% from 2.9%, but the price index rose from 3.5% to 3.9%. The price index is used to calculate real GDP, which excludes inflation. This inflation data point confirms CPI and PPI by demonstrating that inflation is becoming stickier; thus, it will take longer to fall back to the Fed’s 2% objective.

On Thursday, we got another reminder that the labor market remains red hot. Jobless claims remain under 200k, and continuing jobless claims fell slightly. There is little evidence in the graph below of growing layoffs or signs that those laid off are having trouble finding new employment. Therefore, given the Fed’s concern that a price-wage spiral may form, this data, like the GDP revisions, argue for higher rates for longer.

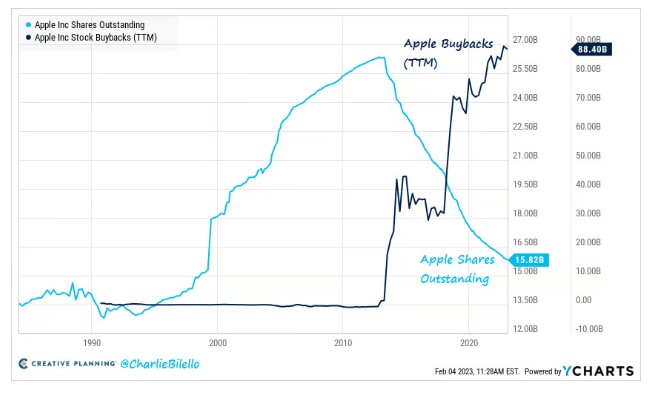

Apple Share Buybacks

The chart below from Charlie Biello shows the amazing amount of shares Apple has repurchased. Apple has repurchased over $550 billion in stock in just ten years. To fathom that number, consider Apple could have bought any company excluding the five largest S&P 500 companies with that money. Exxon, for instance, is the seventh largest company, and its market cap is $466 billion, almost $100 billion less than Apple spent on buybacks.

Gold and Yields

What drives the price of gold?

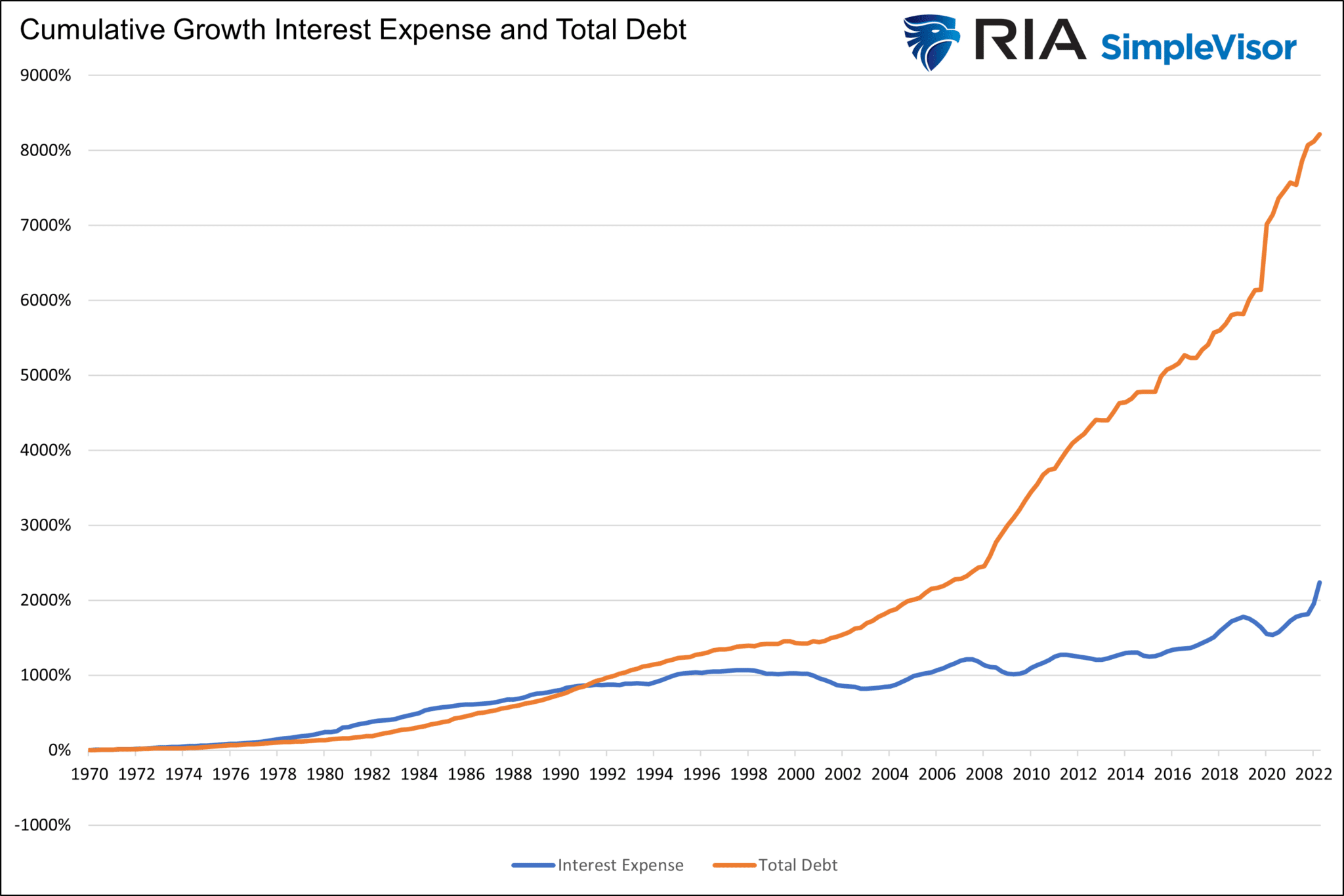

Due to the excessive growth of government debt outstanding and the desire to run perpetual deficits, the Fed is charged with keeping interest rates lower than where a free market would price them. Such allows the scheme to continue. As we have seen, with near-zero interest rates and QE, the Fed can help keep interest expenses low for the government. Since 1970 government debt has risen by about four times the government’s interest expense. Lower interest rates are magical.

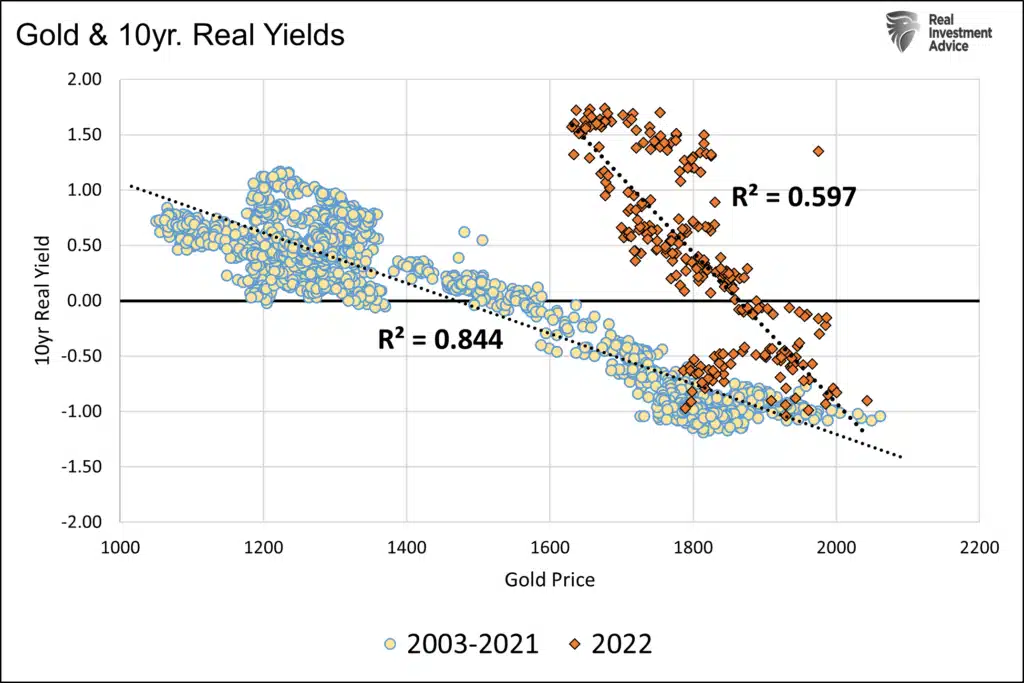

However, to help run deficits, the Fed has presided over many periods of negative real yields. In other words, the Fed has pushed rates below expected inflation rates. Given negative real yields should never happen, we believe negative real yields are a sure sign the Fed is misusing monetary policy to fund deficits. Not surprisingly, gold investors notice negative real yields. The second graph shows a significant correlation between gold prices and real yields from 2003-2021. Real yields were negative through the majority of the period. Conversely the relationship has weakened recently due to positive real yields.

Our latest article, Gold Investors Are Betting On the Fed, helps appreciate what will drive gold prices in the future. As we wrote in the article:

Said differently, gold prices increase when the Fed enacts a monetary policy that is too stimulative given the circumstances.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.