Since the start of the year, the Philadelphia Semiconductor Sector Index (SOXX) is up 33% compared with the broader market, which is up only 4%. The primary rationale for the significant outperformance appears to be the insatiable demand for AI and a shift in its usage. Unlike the past couple of years, in which Nvidia and its GPU production for the development of large language models (LLMs) led the AI chip market, CPU usage is gaining ground as AI agentic models become more popular. Accordingly, CPU producers like Intel and AMD are now playing catch-up to Nvidia, the primary GPU producer. The graphic below shows that agentic AI is equally reliant on CPU and GPU chips, unlike the GPU-centric development of LLMs.

While Nvidia may lose some market share as CPU usage grows relative to GPU usage, there is another facet to consider that favors Nvidia. Profit margins on GPUs are almost double that of CPUs. For example, Nvidia has a profit margin of about 75%, while Intel and AMD are in the low- to mid-40 % range. There are two primary reasons for the distinct advantage as follows:

- Inelastic AI demand — Hyperscalers like Microsoft, Google, Meta, and Amazon are willing to pay premium prices for GPU chips because the alternative (delayed AI deployment) is costlier.

- Monopoly pricing — NVIDIA controls ~80–90% of AI GPU supply, giving it enormous pricing power.

CPUs are much more of a commodity than GPUs. As such, they face much more intense competition, which compresses margins. There are also ARM-based alternatives that offer further competition. So while CPU usage will increase relative to GPUs, profit margins will likely further compress for CPU makers, while remaining abnormally high for Nvidia.

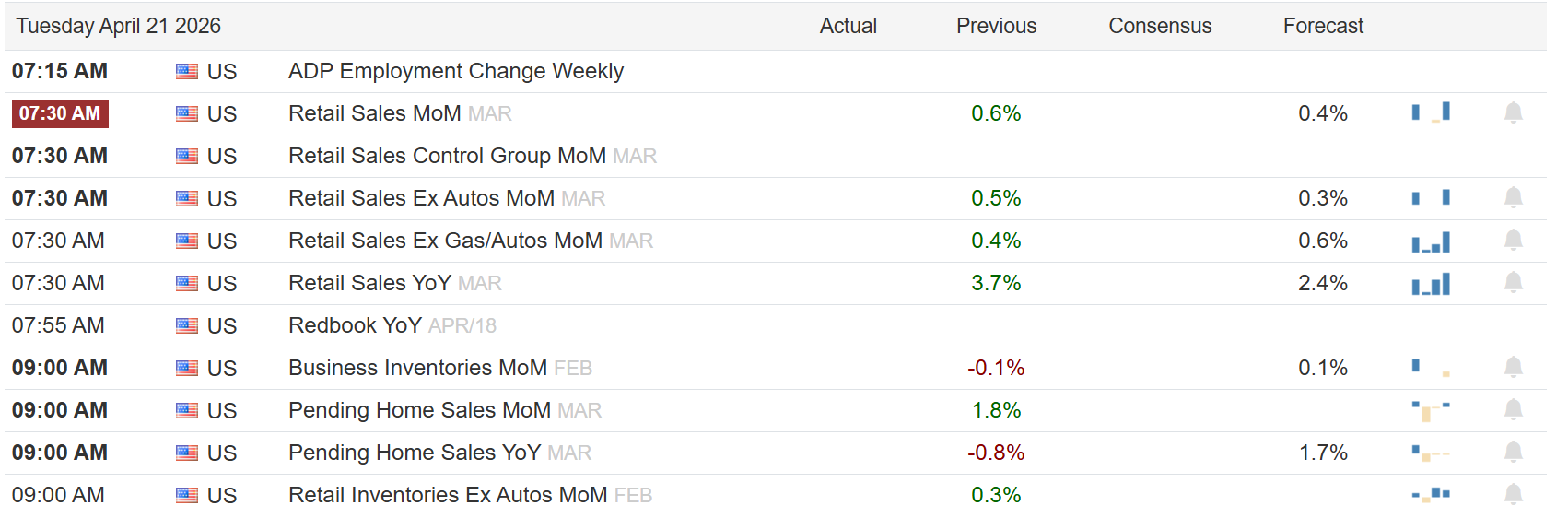

What To Watch Today

Earnings

Economy

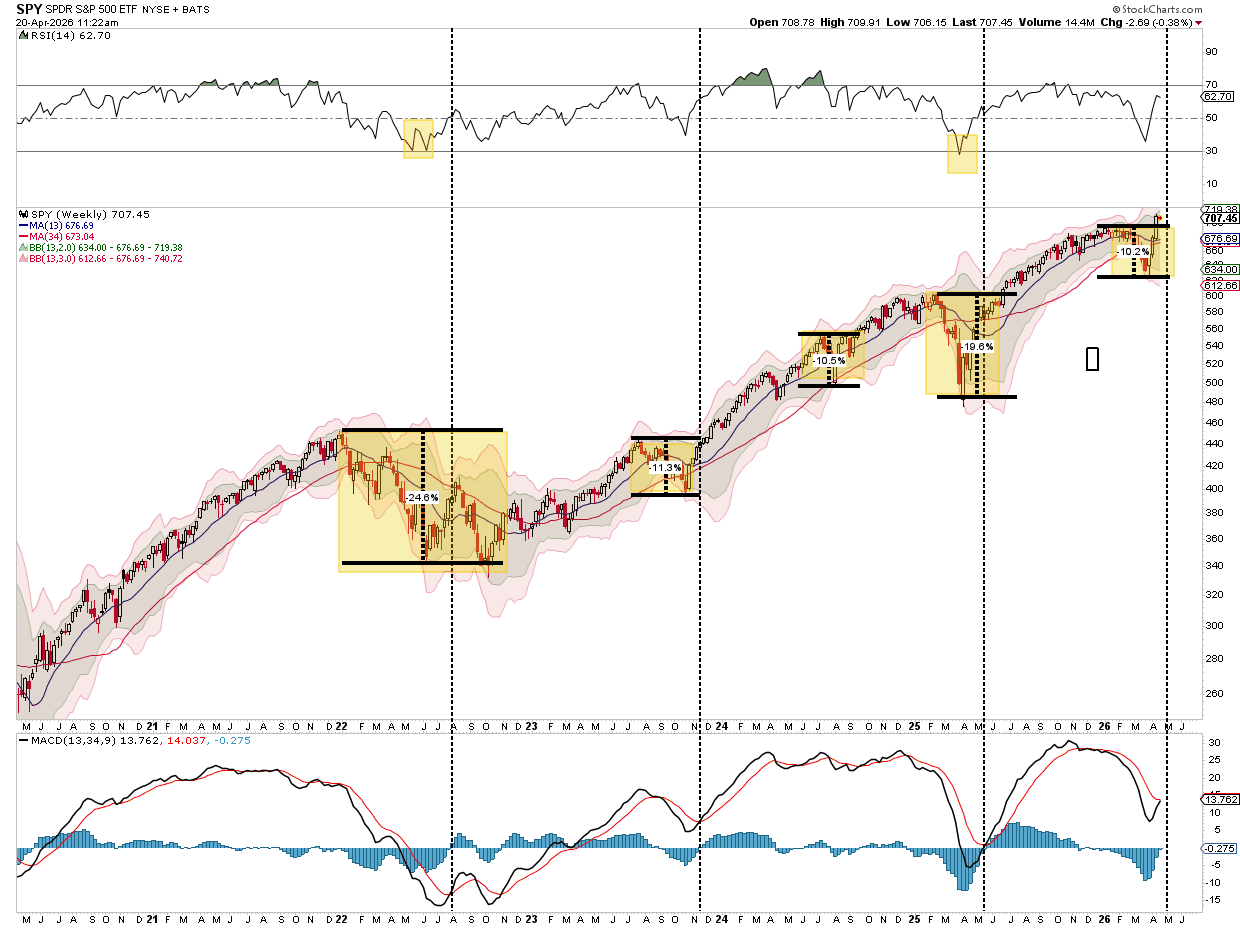

Market Trading Update

Friday’s tape told you everything you need to know about narrative-driven markets. The S&P 500 sprinted another 1.2% to fresh all-time highs above 7,100, crude crumbled 12% to $83, and the 10-year yield eased seven basis points to 4.24%. As noted yesterday, the catalyst was a single headline from Iran’s foreign minister declaring the Strait of Hormuz “completely open” — a statement that, within hours, proved to be more wishful thinking than policy. As such, after 11 consecutive advances, the market pulled back yesterday, as expected.

With momentum and relative strength significantly reversed on a weekly basis, the market surge looks much like we have seen at previous bottoms. What is notable is that in every previous case, once the momentum indicator returned to a buy signal, the prior correction phase was complete. That appears to be the case this time.

However, that sharp an advance is “properly primed for a pull back.” The technical tailwinds that powered this leg higher, such as large macro short-covering and systematic CTA demand, are coming to an end. Prime brokerage data tells the story. Overall book gross leverage sits at 310%, the 92nd percentile over one year and a near-record 98th percentile over five. Net leverage is more moderate at 75%, but fundamental long/short funds just posted their best three-week run since COVID, up 8.2% month-to-date and 7.1% on the year. In other words, the shorts have covered, the underweights have chased, and the engine driving this rally is likely to pause.

As such, use the current rally to rebalance portfolios, stop chasing the index, start hedging the tape, and look where no one else is looking. More importantly, raise cash levels to provide you an opportunity to add to equities further on any pullback to recent support.

Technology Leads As Breadth Deteriorates

A 13% rally in 13 days is quite the feat. Within the sharp rally, there is also a sharp divergence in returns. Hands down, technology led the market higher, while many other sectors relatively languished. As we show in the SimpleVisor analysis below, over the last three weeks, technology stocks (XLK) have moved from the bottom left, indicating oversold conditions on both an absolute and a relative basis, to overbought on both. At the same time, two of the more recently favored sectors, staples (XLP) and utilities (XLU), have moved lower. Their absolute scores haven’t changed much, but their relative scores have fallen quite a bit.

The market was in a topping pattern of sorts from November until a few weeks ago. During that period, lower-beta sectors led the way, while technology and communications faltered. The recent rally, as we noted, is being led by the sectors that powered the market before November. This again raises the question of whether the recent outperformance of technology and other large-cap growth stocks signals that the upward trend is back on track, or a brief respite before value and low beta take over and prices consolidate or even decline.

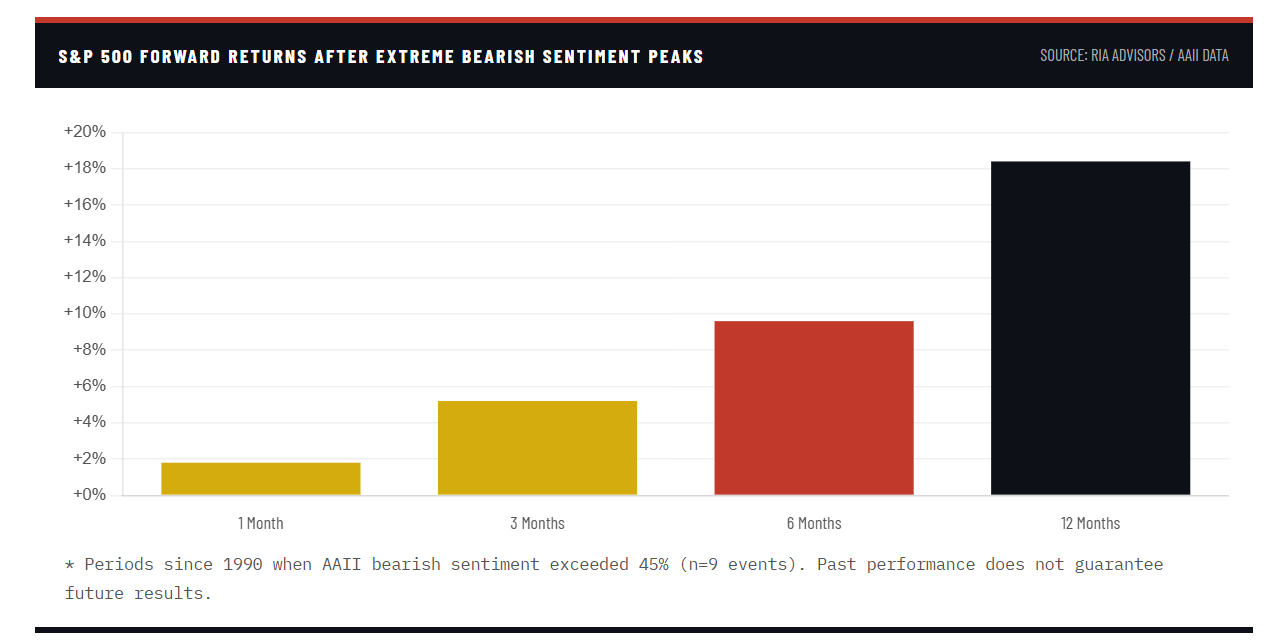

Market Lesson: Why Panic Is A Costly Mistake

The stock market selloff between February 28 and April 14 produced one of the more instructive market lessons in recent memory. It isn’t because of what the market did, but because of what investors did in response. By April 2nd, the AAII Sentiment Survey showed bearish sentiment at 51.4%, the highest reading in years, well above the historical average of 31%. Put option volume surged, and the financial media ran daily coverage of worst-case oil scenarios, recession projections, and S&P 500 targets as low as 3,800.

However, when you have that combination of bearishness, as we discussed in 5-Consecutive Weekly Declines, markets tend to perform better.

What was surprising was that the S&P 500 recovered completely in two weeks and is now setting all-time highs.

That sequence is not a reason to relax, but it is a valuable market lesson. It is also a good reason to examine what happened to investors who panicked, why the pattern repeats with such regularity, and, most importantly, what a well-constructed portfolio actually looks like when the next stock market selloff arrives. Because it will arrive. The only uncertainty is the catalyst.

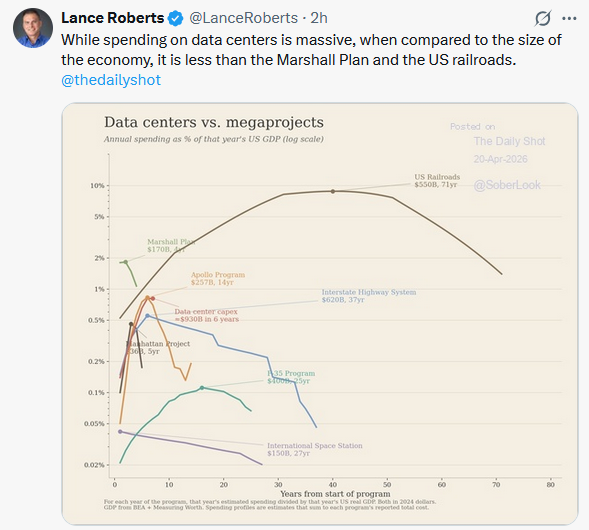

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.