Increasing corporate credit spreads, or a growing divergence between corporate bond yields and similar-maturity Treasury yields, can be an omen of stock market weakness. Recent troublesome defaults in the private credit markets are showing signs of spreading concern to the more liquid corporate debt markets. Thus, it’s appropriate to review corporate credit spreads. in the process, we are taking advantage of this opportunity to give you a sneak peek at the new SimpleVisorAI. We are aiming to release this enhanced version with AI capabilities in the coming months.

Credit spreads have recently been widening, potentially signalling financial distress in the system. However, spreads are nowhere near concerning levels. The top table below shows the current yield spreads (versus US Treasuries) for investment-grade-rated bonds (AAA, AA, A, and BBB) and junk-rated bonds (BB, B, and C). Moreover, we provide historical context showing how the current spread ranks in the short- and long-term. For instance, A-rated bonds, at a 70bps credit spread, are nearly as wide as they’ve been over the last three months, ranking in the 94th percentile. But it ranks very low (6.7%) over the last 20 years. The short-term graph at the bottom left shows the recent uptick in spreads, but on the long-term graph to the right, the increase is barely perceptible.

Spreads are widening but are not yet concerning. Given the importance of credit spreads to the economy and their role as a seer for the stock market, we advise keeping an eye on them. Current yield spreads and the historical percentiles can also be found on the current version of SimpleVisor.

What To Watch Today

Earnings

Economy

Market Trading Update

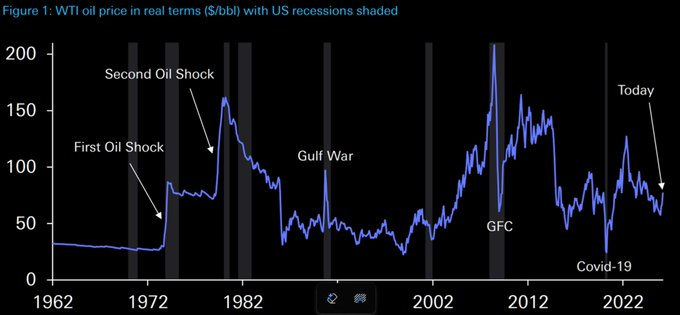

Yesterday, we discussed the current rally in the US Dollar and its implications for other asset classes. The market is adapting very quickly to the military conflict overseas. After an initial spike in oil prices on Monday and Tuesday, those prices are already stabilizing. As we noted yesterday morning, a longer-term look at previous military engagements and events relative to oil prices suggests the current move is hardly worrisome yet.

More notably, the decline in volatility has also been very pronounced. After an initial spike on Monday, the VIX index has already retraced much of its move, and investors are unwinding their hedges. While the attack on Iran was seemingly unsuspected, volatility had already been on the rise since the beginning of the year. In other words, traders were concerned about market risk and were hedging for it, and the attack on Iran was just the catalyst that crystallized those concerns.

With progress in Iran moving quickly, concerns over oil shipping being reduced, and economic data in the U.S. coming in stronger than expected, the market seems to be stabilizing at recent support levels. The long consolidation since the beginning of the year has reduced much of the previous overbought conditions, and most of the market’s “growth sectors” are now trading at decent discounts to forward earnings.

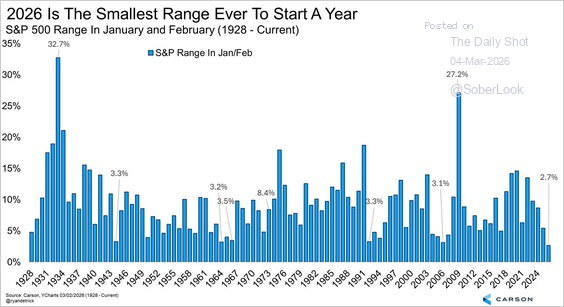

While it is still too soon to tell where the market is likely headed next, the compression of the trading range is notable. In fact, this is the smallest trading range for the market at the beginning of the year, ever. Does that mean the market is about to crash? No. However, as that range expands, it will likely be quite explosive, so the breakout direction from the current compression will be critical for traders to watch.

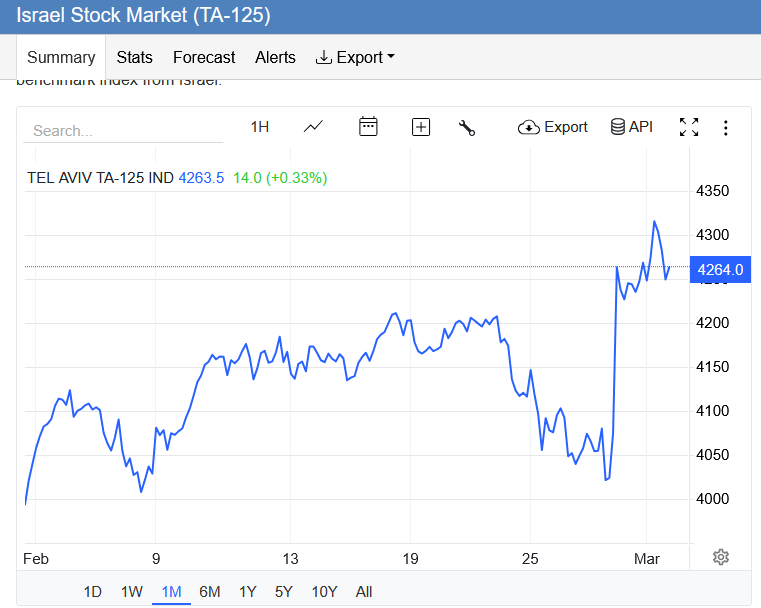

Israeli Investors Price In A Brighter Future

Unlike the US or many other global stock markets, the Tel Aviv stock market has rallied since the Iran conflict started. The graph below shows that the Tel Aviv 125 surged by nearly 5% to an all-time high at the start of the conflict. Such a strong upward move is counterintuitive given that Israel is in the direct line of fire from Iran. Also of note, Israel’s currency, the shekel, strengthened against the dollar, reinforcing the perception that Israeli assets are benefiting from the geopolitical developments.

The primary reason for the enthusiasm is that investors appear to be pricing a long-term political strategic shift rather than the immediate economic and physical damage. Investors are betting heavily that a successful military campaign could weaken Iran’s regional influence and reduce the long-standing security risk hanging over Israel’s economy. In other words, while war is typically negative for economies in the short run, the equity market is forward-looking and appears to be pricing the possibility that the conflict ultimately improves Israel’s long-term security environment and boosts key domestic industries.

The Passive Agressive Market: Bogle’s Warning Came True

John Bogle is known as the “father of indexing.” In 1976, he launched the First Index Investment Trust at Vanguard. His fund, tracking the S&P 500, was the first index mutual fund available to retail investors. The fund was mocked by competitors as “Bogle’s Folly.” Today, Vanguard manages over $12 trillion in assets, a testament to the power of Bogle’s low-cost, buy-and-hold passive investing philosophy. Ironically, Bogle warned that ETFs’ intraday liquidity would tempt investors into the active trading behavior he had spent his career arguing against.

In 1993, the SPDR S&P 500 Trust (SPY) became the first ETF available to US investors, enabling intraday trading in passive indexing securities.

Passive investment strategies and associated securities were designed to bring discipline and longer-term strategic thinking to investors. Instead of actively buying and selling individual stocks to beat the market, passive strategies are comfortable matching market returns.

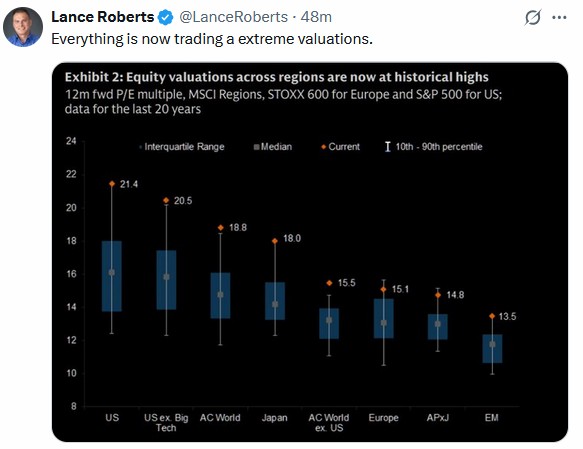

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.