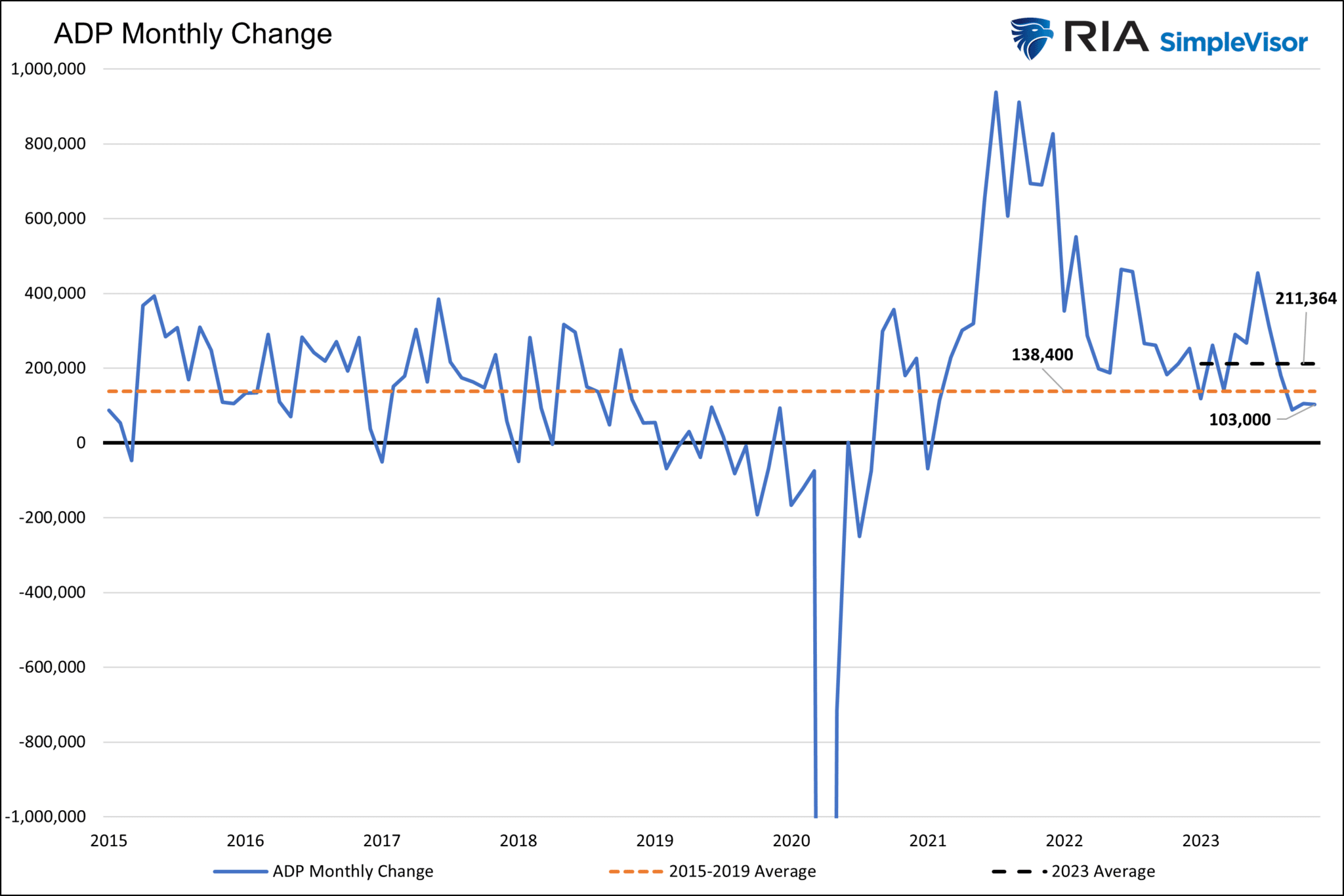

The ADP jobs report came in at 103k versus the expected 130k. The ADP also revised the jobs count from October to 106k from 113k. Over the last three months, the average gain has been just under 100k. Unlike the BLS, which surveys companies about their employment activity, ADP uses actual payroll data, including more than 25 million private sector employees. Its methods avoid double counting employees with multiple jobs and estimates, which are often provided to the BLS for their surveys. While the BLS is much more closely followed, ADP is more likely to give us a more accurate state of the jobs market.

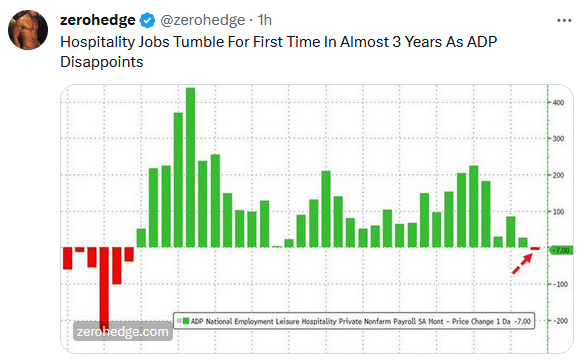

100k ADP new jobs a month is still decent but below the 138.4k pre-pandemic average and half of the average for 2023. Within the report, a couple of indicators show that the key drivers of job growth and wages are quickly normalizing. First, ADP’s chief economist notes: “Restaurants and hotels were the biggest job creators during the post-pandemic recovery.” “But that boost is behind us.” The leisure and hospitality industry lost 7,000 jobs in Thursday’s report. The Fed has been very concerned that higher wage growth feeds inflation. To that end, ADP says the rate of pay increases for “job-stayers” and “job-changers” is the lowest in over two years.

If Friday’s BLS report shows similar labor conditions, the Fed is done raising rates, barring an unexpected jump in inflation.

What To Watch Today

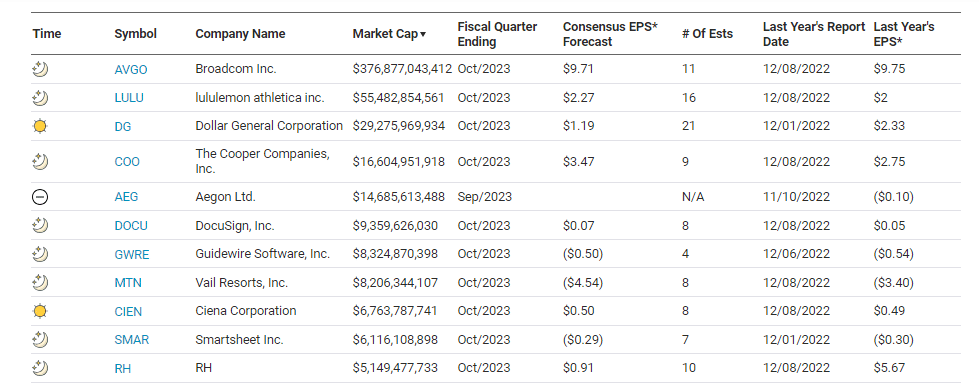

Earnings

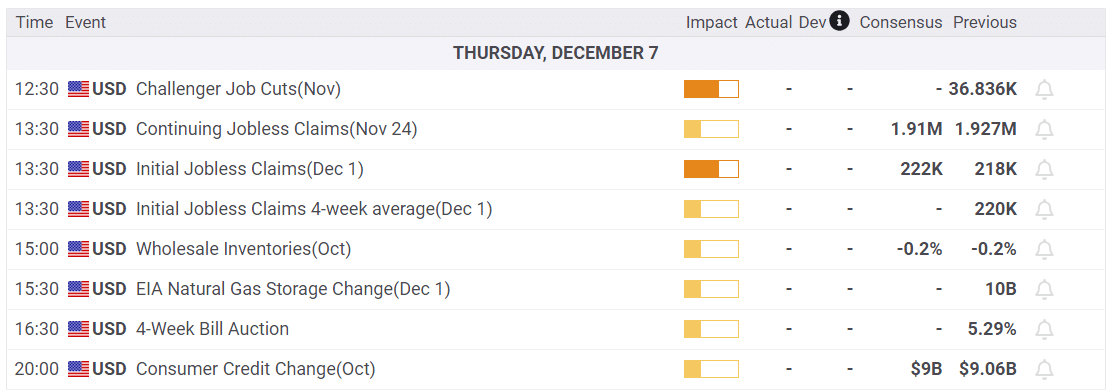

Economy

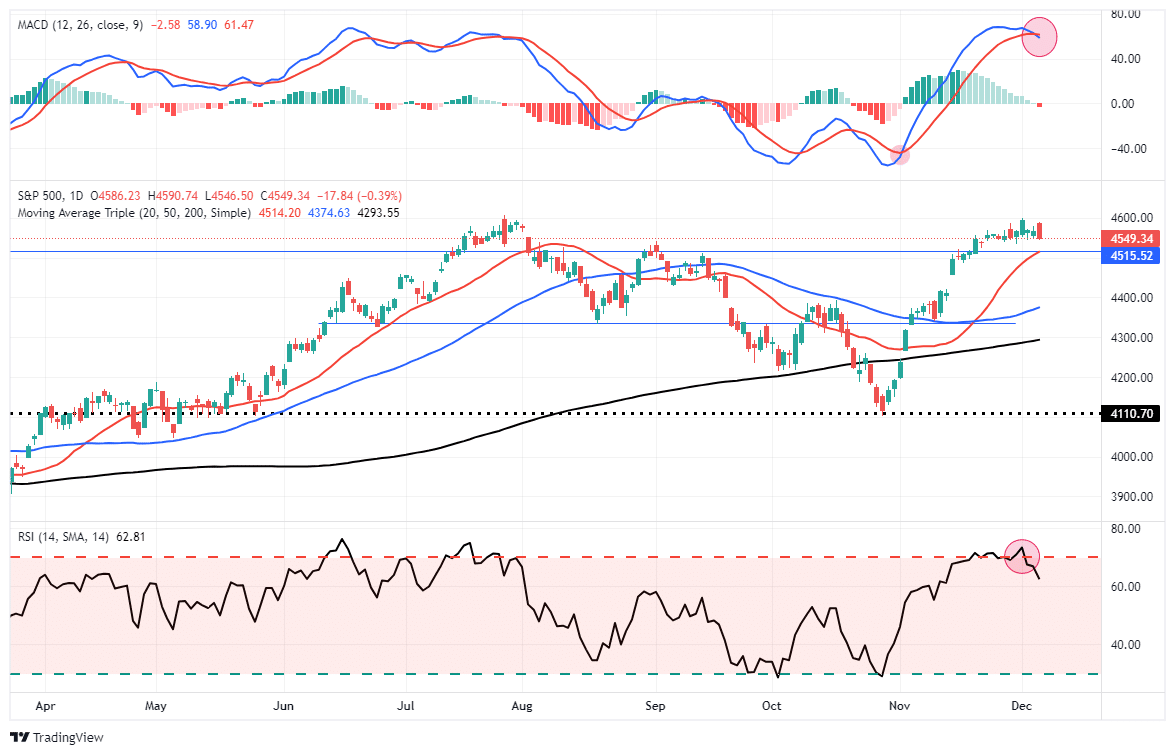

Market Trading Update

While the market tried to start the day out on the upside, the selling pressure continued throughout the day, with the market ending near its lows. Importantly, the sell-off yesterday triggered the MACD “sell signal,” and the RSI index moved solidly into correction territory. While this does NOT mean that markets must decline precipitously, it does suggest that upside is outweighed by downside risks.

As we have noted over the last several days, the risk/reward has not been in the investor’s favor, so we have suggested completing tax loss selling and portfolio rebalancing at these more elevated levels. As noted, whatever pullback we do get over the next week or so, particularly as stock buybacks go into “blackout” on Friday, will likely be limited. Use any pullback to add exposure as needed for now.

The next big driver for both bonds and stocks will be Friday’s employment report.

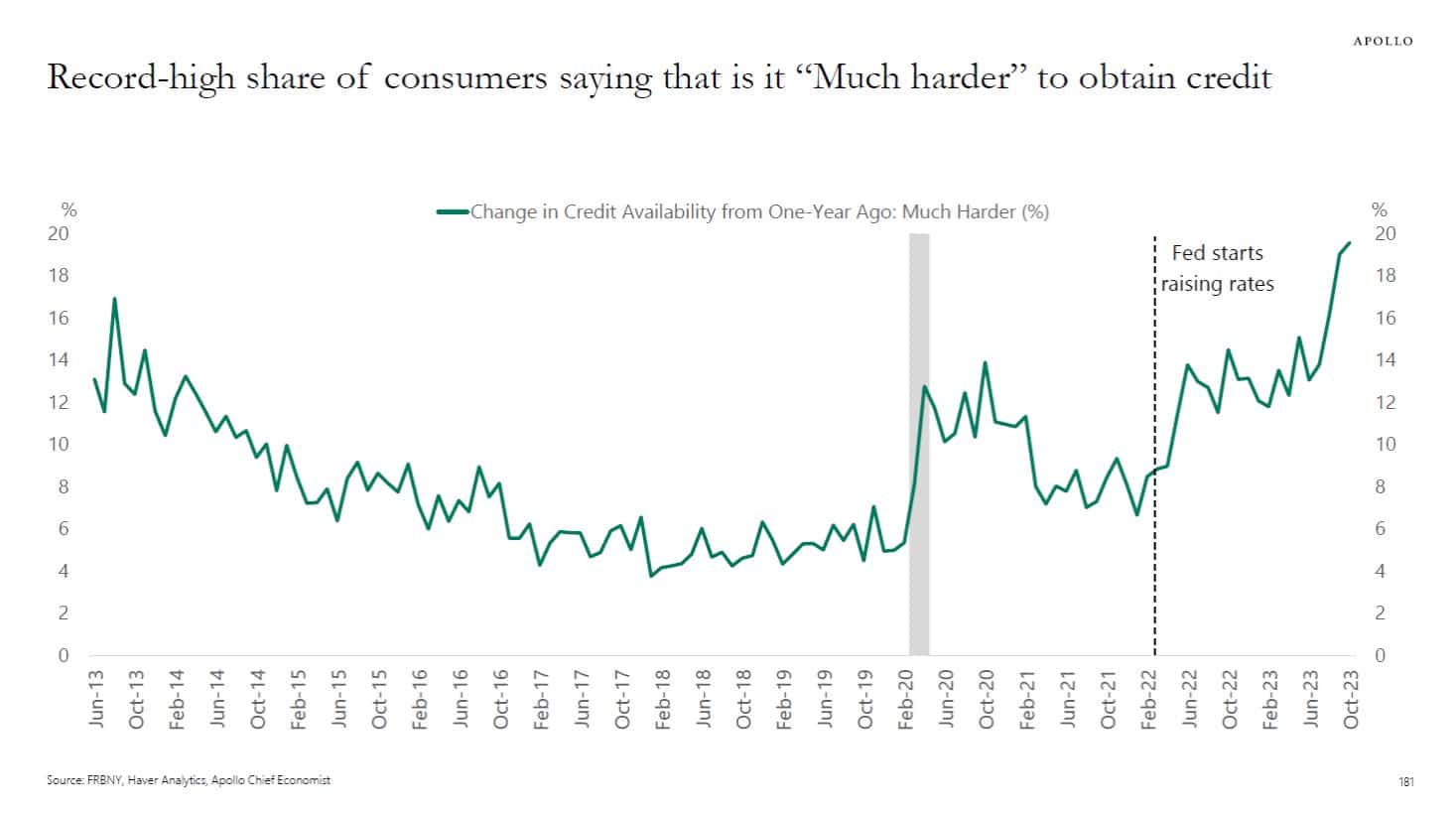

Consumer Credit Is Getting Difficult To Obtain

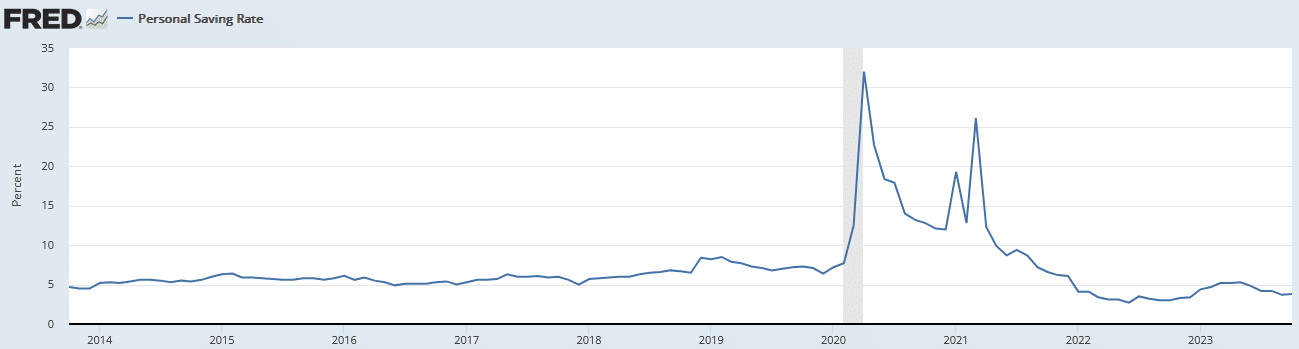

Accounting for about two-thirds of GDP, personal consumption is the most important economic factor to consider when assessing future growth potential. Given that, the means for consumers to consume are vital to follow. The first graph below, courtesy of Apollo, shows that consumer credit is now more difficult to obtain than at any point in the last ten years. Additionally, it is the most expensive. The second graph shows that personal savings spiked due to direct checks from the government in 2020 and 2021. Since then, consumers have been saving less. While dipping into savings fueled growth in the past, consumers now need to rebuild savings. Lastly is wage growth. As we share in the opening, ADP wage growth is now the slowest in two years. That said, it is still robust. Further weakness in wages, along with credit and savings trends, will weigh on personal consumption and GDP.

More On Consumer Credit

Consumer credit has been growing rapidly, but as the WSJ points out in their article, American Borrowers Are Getting Closer To Maxing Out, those trends may ending. Per the article:

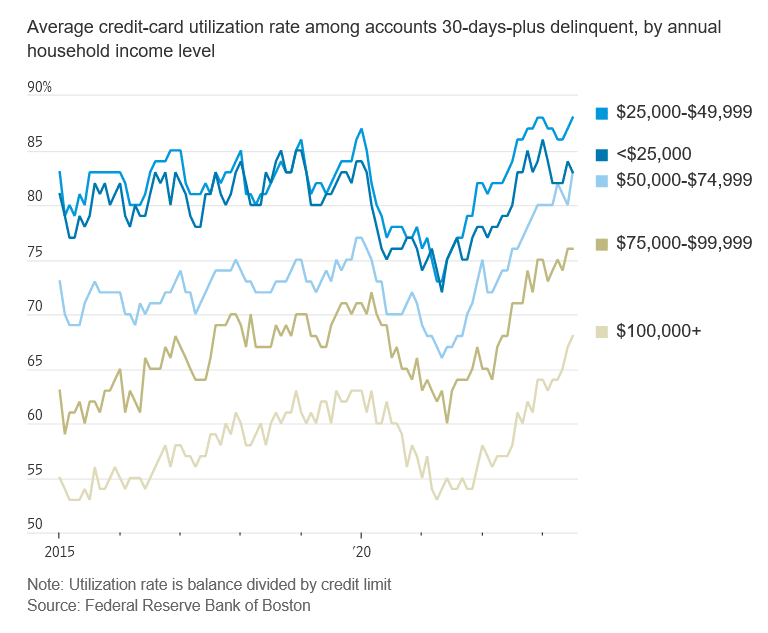

A recent note published by the Federal Reserve Bank of Boston found that as of July, consumers with annual household incomes of less than $50,000 whose accounts were delinquent were on average utilizing 80 to 90 percent of their available credit. This leaves “those consumers with a very small amount of credit left on their accounts to cushion against a deterioration of their financial situation,” according to the paper. Across all cardholder income groups as of July, average utilization rates—the ratio of outstanding card account balance to the account’s credit limit—were above February 2020 levels.

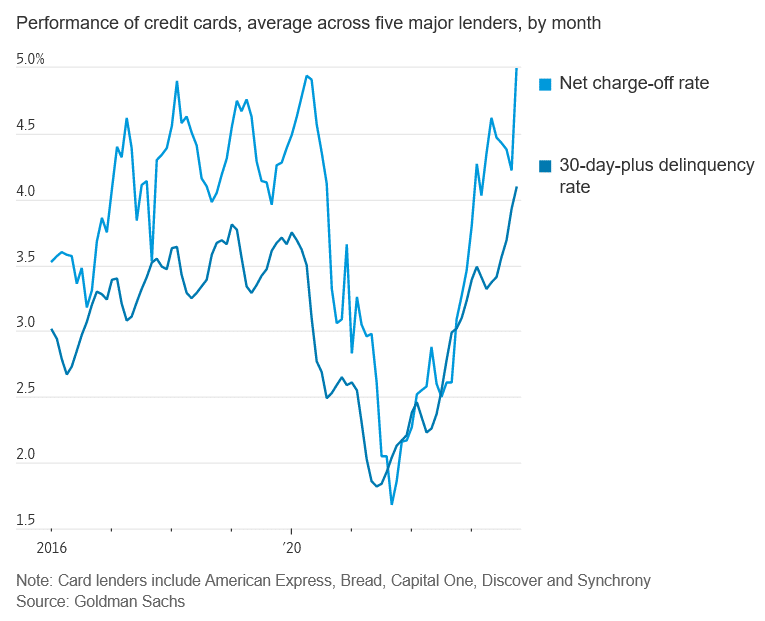

As evidence that consumers are starting to struggle with credit, consider that credit card charge-off and delinquency rates are now at seven-year highs.

The strong job market and rising wages will deflect some of the credit card woes noted in the article. However, credit delinquency and defaults will continue to rise if the labor market weakens. As a result, banks will offer more stringent terms on credit, including lower credit lines.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 50

2023/12/07