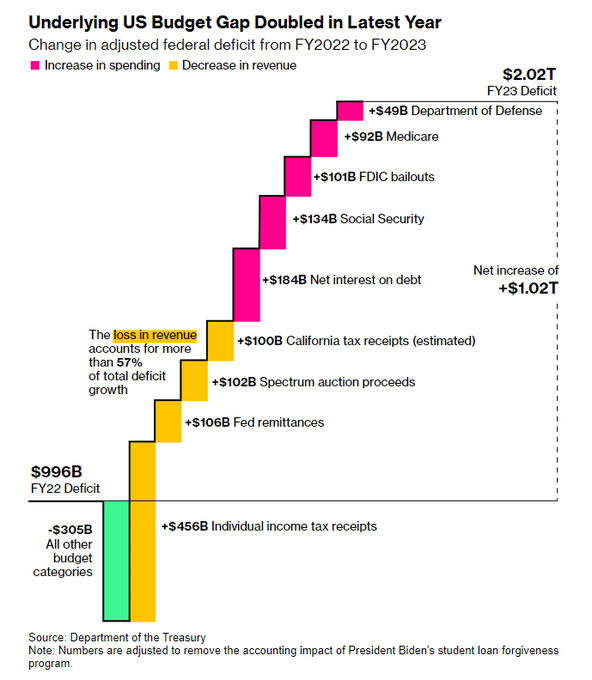

The Bloomberg graphic below and their article entitled Deficit Doubling as U.S. Economy Grows provide excellent insight into factors that account for the significant deficit growth for the fiscal year ending October 2023. The most significant contributor to the deficit growth was a sharp decline in tax revenue. Specifically, individual tax receipts fell by $456 billion from the prior year. Bloomberg credits much of the lost tax revenue, ergo deficit growth, on the financial markets. In 2021, stocks rose by nearly 30%, while stocks and bonds declined in 2022. Further, there was a delay for some 2022 tax revenue due to extensions granted in disaster areas. As shown below, Bloomberg estimates California alone accounts for about $100 of delayed revenue.

Increasing interest rates accounted for nearly $200 billion in additional interest expenses versus the prior year. If interest rates rise or stay near current levels, this expense will keep rising through the current fiscal year. That said, rates could drop quickly if economic growth slows or declines and inflation normalizes. Consequently, the net increase in interest expenses could be less than in 2023. Social Security and Medicare expenses increased due to the sharp 8.7% cost of living adjustment. Lastly, the Treasury did not receive remittances from the Fed as the Fed lost money. While the deficit growth is large, some of the increases are temporary.

Per the article, The deficit for the fiscal year that began Oct. 1 will likely shrink, thanks in part to the positive performance of financial markets in the 2023 calendar year — which ought to boost revenues when taxes are paid in 2024. The delayed California receipts will also help.

What To Watch Today

Earnings

Economy

Market Trading Update

Over the last few days on our Before The Bell video, we discussed that overreacting to an initial break of the 200-DMA can be detrimental. There are many instances where some support level is broken, and then the market immediately recovers. Such was the case yesterday as earnings pushed stocks higher into the afternoon, with the market reclaiming the 200-DMA. With the market oversold on multiple levels, there is fuel to catalyze a reflexive rally to the 50-DMA. A retracement to that level will be a more opportunistic level to reduce equity risk and raise cash levels if needed heading into year-end.

As we discussed in yesterday’s blog post:

“Heading into year-end, the historical probabilities of a year-end advance, particularly following summer weakness, outweigh bearish possibilities. There are many “possibilities” bearish investors are betting on, which are unlikely to manifest themselves before year-end.”

- Inflation is about to surge higher, needing a more aggressive Fed response.

- The economy will drop into a recession, as suggested by the inverted yield curves (shown below.)

- The housing market is going to crash.

- Unemployment is about to increase.

- Households are drastically cutting spending.

- Corporate earnings and profits are going to reverse.

“Each concern is valid, and many will likely manifest themselves in 2024. Notably, since most of this year’s market advance was valuation expansion, the markets must eventually correct to accommodate higher rates.”

The point to be made is that while a rally into year-end is likely, next year will likely be another tough year for stock investors.

Value In Small And Mid-Cap Stocks

The graph below shows the substantial divergence in the forward valuations of large-cap stocks versus small (S&P 400) and mid-cap stocks (S&P 600). As shown, forward valuations are off their peaks for all three indexes, but small and mid-cap valuations have been cut in half from the 2020 peak and are not far from the 2020 and 2008 lows. While it may be tempting to buy small and mid-cap stocks, the concern is that higher interest rates are problematic for many highly indebted small and mid-cap companies. Further, credit spreads, or the difference between lower-rated corporate bond yields and Treasury yields, are still near historical lows.

If a recession hits, those spreads could widen significantly and more than offset a decline in Treasury yields. There are stocks with great value propositions in small and mid-cap space. Still, one must be careful of the debt situation and the possibility that valuations cheapen further as economic activity slows and credit spreads widen.

RTX Rallies On Good Earnings

Shares in RTX opened up over 5% yesterday as it beat analysts’ earnings expectations across the board. The graphic below summarizes its earnings. Earnings are clearly benefiting from Ukraine, rising tensions in Taiwan, and the Israeli war. Per the CEO:

“The historic demand across our commercial aerospace and defense businesses drove 12 percent organic sales”

Most importantly, they “made significant progress on our assessment of the Pratt Whitney metal manufacturing matter,” and they conclude the costs are in line with previously announced expenses. RTX was trailing competitors like LMT and GD as investors were concerned the issue would be more expensive than initially budgeted for. Thus far, that does not appear to be the case.

The graph below the earnings highlights shows that RTX did make up some ground on its competitors yesterday, but it still has a ways to go.

Higher Mortgage Rates and House Purchase Cancellations

As we wrote in yesterday’s Commentary:

30-year mortgage rates just eclipsed 8 percent. With higher mortgage rates, housing affordability tumbles. And, not surprisingly, the Mortgage Bankers Association (MBA) mortgage application index is at a multi-decade low

The graph below further confirms the housing market is troubling due to higher mortgage rates. 53k home purchases, equating to 16.3% of all home purchases, were canceled in September. Such is the highest cancellation rate since October 2022 and the peak of the pandemic shutdown before that.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 0

2023/10/25