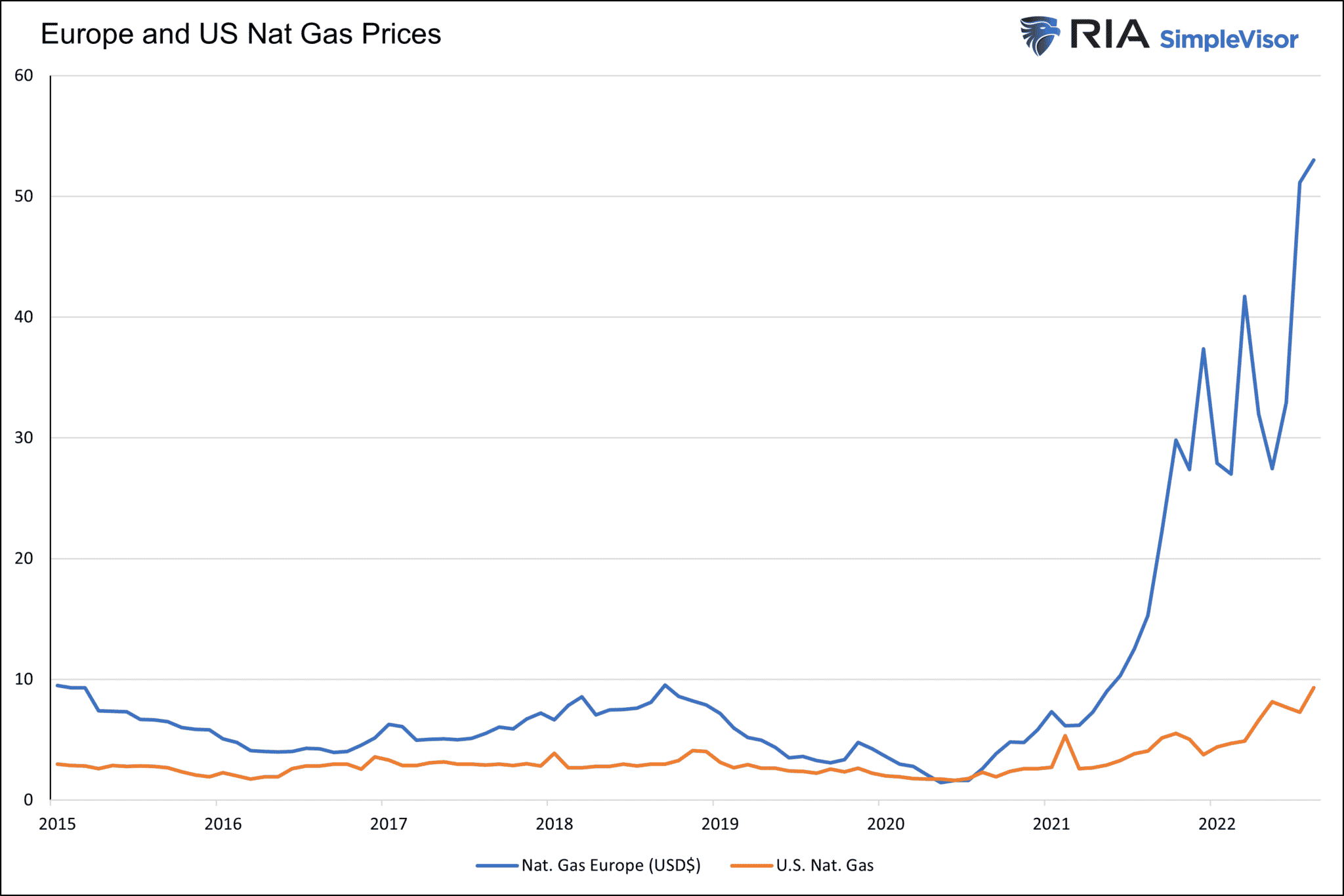

Bloomberg recently published a disturbing article entitled- A ‘Tsunami of Shutoffs’: 20 Million US Homes are Behind on Energy Bills. Per the article, approximately one in six homes, or 20 million, are not current on their energy bills. The article cites PG&E (California), which has seen a 40% increase in customers behind on their energy bills over the last two years. The culprit, the average U.S. electricity price is up 15% year over year. To wit:

It is, according to the National Energy Assistance Directors Association (Neada), the worst crisis the group has ever documented. Underpinning those numbers is a blistering surge in electricity prices, propelled by the soaring cost of natural gas. -Bloomberg

As we discussed in our 8/24/22 Commentary, Europeans have it much worse, as Russia is limiting the supply of natural gas. The problem here and abroad is not only the surging price of natural gas, as shown below, but the burden of high inflation. A cold winter here or in Europe or Asia and a slow retreat in inflation will further crimp consumers and possibly worsen the energy bill crisis.

What To Watch Today

Economy

- Dallas Fed Manufacturing Activity, August (-12.7 expected, -22.6 prior)

Earnings

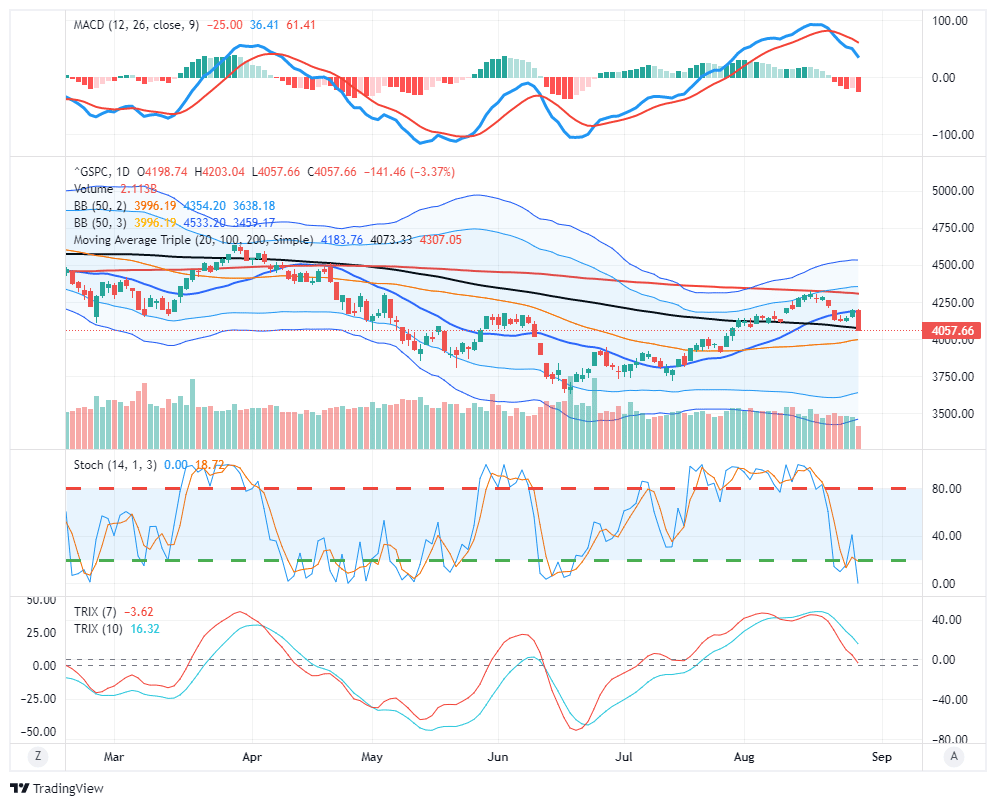

Market Trading Update

Last week, the market attempted a rally on Wednesday and Thursday in hopes that Jerome Powell’s Jackson Hole Summit speech would confirm the market’s expectations of a more “doveish” tilt.

Unfortunately, the market was wrong.

On Friday, Jerome Powell delivered a much more hawkish message than expected, stating the need to continue to hike rates to combat inflation. To wit:

“Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.” – Jerome Powell

That message was not the “pivot” the market was looking for and consequently fueled a sharp market sell-off on Friday. The break of the 100-dma also sets the market up for a retest of the 50-dma next week. As I noted in this past weekend’s “Bull Bear Report:”

“Given the sharp market sell-off on Friday, some follow-through selling on Monday would be of no surprise.”

The negative futures this morning confirm that looks to be the case.

However, with the markets once again deeply oversold, a reflexive bounce is likely. With the market failing a test of resistance at 4160ish, and with the MACD still on a “sell signal,” we continue to suggest selling any rallies for the time being.

More Selling Pressure Ahead

Interesting note on Zerohege this weekend:

Goldman’s biggest trading desk bull, Scott Rubner, who steadfastly – and correctly – encouraged the bank’s hedge fund clients to keep buying the most hated rally until its peak just below the 200DMA, joined BofA’s Michael Hartnett in turning bearish and warning that it’s time to sell and that the response to the question “are we there yet”, is “yeah we are” and that “sellers are lower.

GS estimates that CTA’s need to Sell -$8.3B worth of global equity futures over the next 1 week, assuming a flat tape. (Thresholds: ST 4091, MT 4148, LT 4105). I.e., medium-term triggers today.

The asymmetry is skewed to the downside, with $1.1B to buy in an “Up Big” tape vs. $46.6B to sell in a “Down Big” tape.

The same is true for the next 1-month, with $68B to buy in an “Up big” tape vs. $147B to sell in a “Down Big” tape. Total Systematic, our numbers increase $124.8B (up big) vs -$178.7B (down big).

Keep an eye on month-end (Wednesday), where we expect another -$9B for sale from pensions.

The Week Ahead

The pre-Labor Day holiday week should be relatively quiet other than employment data on Tuesday, Wednesday, and Friday and ISM Manufacturing on Thursday. The JOLTS report is expected to show 10.5 million job openings. That would be slightly lower than last month’s figure but well above pre-pandemic norms. ADP on Thursday will be interesting. It was not released in July as they were modifying the calculation. The ADP calculation is moving away from trying to be a predictor of the BLS jobs report and instead more accurately highlighting their proprietary data. The BLS is expected to report a 310k gain in payrolls on Friday. Any deterioration in the labor market is likely to be first seen in hours worked and the change in temp workers.

ISM will likely stay in expansionary territory. More important will be the new orders and prices subcomponents. New orders are a great leading indicator. A further decline in the prices index will help assure investors that inflation is peaking and heading lower.

Powell Stresses His Hawkish Outlook

“Today my remarks will be shorter, my focus narrower, and my message more direct.” Jerome Powell’s speech at Jackson Hole did not mince words. (Our) “overarching focus right now is to bring inflation back down to our 2 percent goal.” He fully acknowledges that successfully fighting inflation will come at a cost.

Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation.

The Fed’s aggression seems primarily based on the Fed’s experience in the 1970s and 80s. To wit:

“History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting. The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.”

The market thought Powell would not be as hawkish. Many expected the Fed to stall rate increases later this year and pivot toward lower rates by next summer. Instead, Powell thinks the pace of rate hikes will slow, but they will continue. Instead of a stall and pivot, we are more likely to see a slower assent higher into next year and no pivot. Obviously, financial and economic conditions and the state of inflation can change the Fed’s rate path abruptly.

Interestingly, Powell did not mention QT.

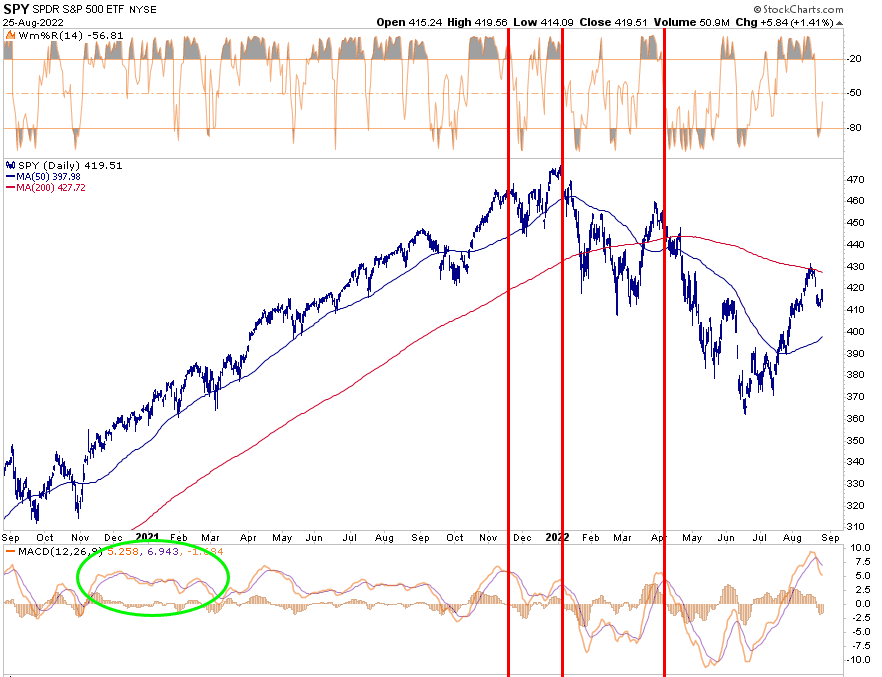

The MACD Leads the Way

The MACD, or moving average convergence divergence, is one of many technical tools we rely on. Like most technical tools, it goes through periods where it is effective and ineffective. The graph below shows the MACD was relatively ineffective during the post-pandemic rally. However, since the market topped, it has been a great tool to help time markets. The red vertical lines highlight each time the MACD lines had a bearish cross from a positive level. Selling on that signal has worked well. Buying on positive crosses has not been nearly as successful.

As noted in recent commentaries, the MACD has once again had a bearish cross. If we are in a bear market, it is likely signaling another leg lower in the market. If the market has bottomed and the bull market has resumed, we may see it exhibit the same behavior as in 2021. We are staying conservative in part due to the MACD.

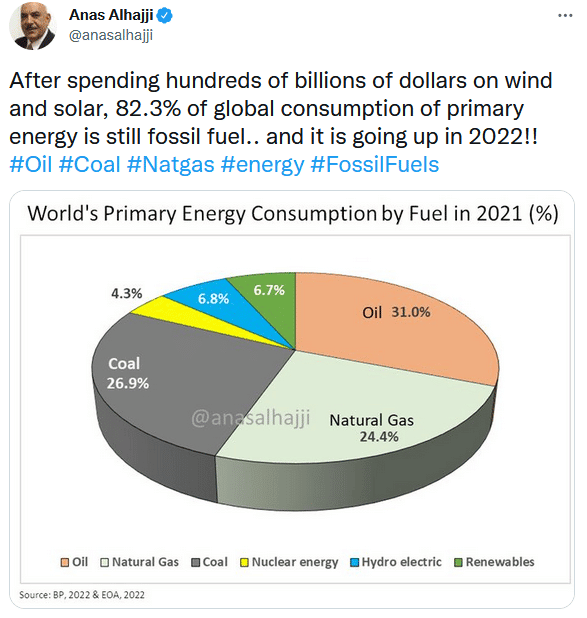

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.