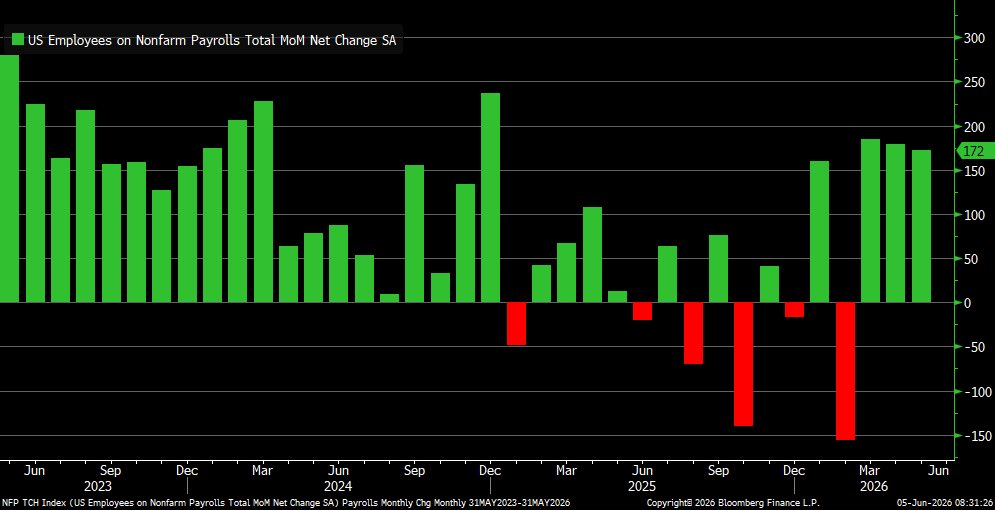

New Fed Chairs are often tested early in their terms. For instance, two years after Bernanke took over the Fed, the Financial Crisis kicked into full gear. Janet Yellen was tasked with addressing stock market weakness as the Fed was navigating an exit from QE. Powell’s early test was a rate-hiking cycle that spooked markets in 2018, followed by the Pandemic two years later. Kevin Warsh, who took the Fed Chair just weeks ago, may have received his first test with last Friday’s employment data.

Warsh inherits a Fed that has kept rates at restrictive levels as inflation has remained stubbornly high, even before the additional boost from the Iranian conflict. Furthermore, consumer confidence is near pandemic lows, and bond yields are pushing higher. On top of that, as we share in “The Week Ahead” section below, May’s nonfarm payrolls came in at 172,000, almost double expectations. Yields jumped immediately, and stocks sold off. The market reactions were a function of rising odds of a rate hike. Any thoughts that Fed Chair Warsh has about being dovish, whether in tone or action, will not sit well with bond investors, who are witnessing high inflation and a resurgence in the labor market. Simply, the Fed Chair has no credible path to cutting rates in the near term. Warsh’s first meeting will likely be a “hawkish hold.”

The question for investors is not whether Warsh holds rates steady on June 17. He most likely will. The question is whether he can soothe bond market concerns, and whether investors believe him. As shown below, Fed Funds futures are now pricing in a 50% chance that the Fed hikes rates by October.

What To Watch Today

Earnings

Economy

- No economic reports today

Market Trading Update

As we noted last week in Parabolic Semiconductor Rally: What Breaks The Trade?, Broadcom’s earnings were the single most important test for this advance, because the trade you can’t sustain forever is the one that snaps first. Broadcom delivered the catalyst. It beat on the quarter but guided next-quarter AI revenue to about $16 billion against the $17.2 billion the Street wanted, and the sell-the-news reaction was textbook for a stock priced for perfection. So, has the semiconductor rally ended? The parabolic phase has.

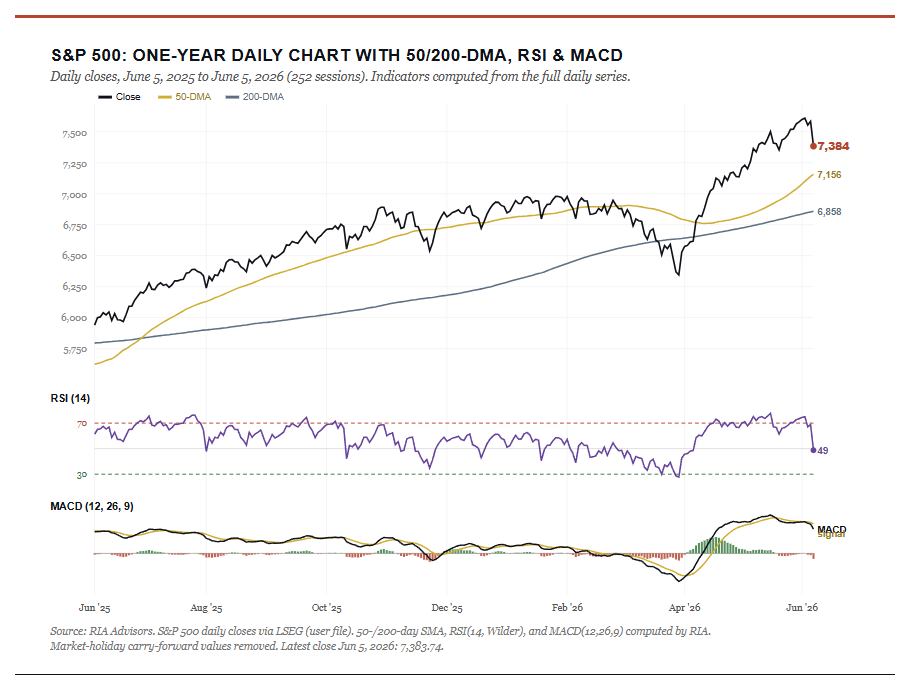

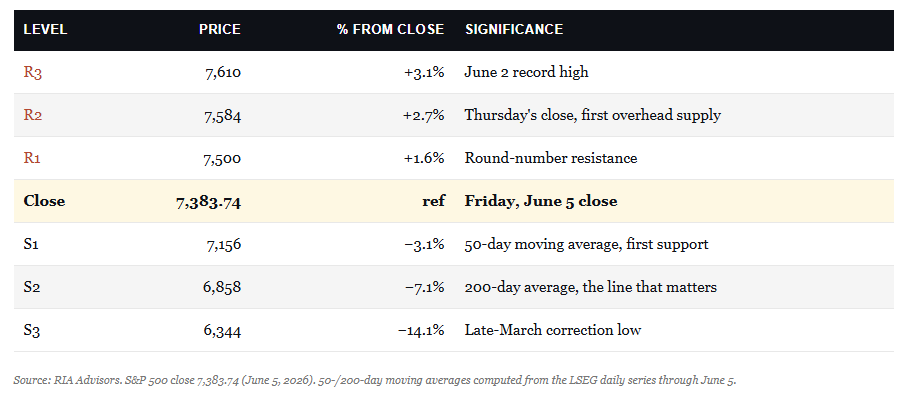

Step back from the noise. At Friday’s close of 7,384, the S&P 500 still sits about 3.2% above its rising 50-day moving average near 7,156 and roughly 7.7% above its 200-day average near 6,858, so the primary uptrend remains intact even after a hard week. The damage so far is to momentum, not to the trend itself, but as we discussed on Friday, leverage is an underlying issue to pay attention to.

The momentum picture is where the warning signs live. The 14-day RSI tagged 75 at Tuesday’s record, deep into overbought territory, then collapsed to roughly 49 by Friday as the selling accelerated, a violent four-session reset from euphoria to neutral. Worse, the MACD has now crossed below its signal line with the histogram flipping negative, the classic loss-of-thrust that follows a vertical run. Breadth tells the same story. Only about 56% of S&P 500 members trade above their 50-day average, meaning this record was carried by a shrinking handful of names.

The chips are the tell. The Philadelphia Semiconductor Index fell 5.21% on Thursday, its worst session since early 2025, and Broadcom alone surrendered roughly 14% after an 88% run over the past year. When the generals retreat, and the troops are already thin, the index rarely powers straight back to new highs. It digests first.

For traders, the playbook is mechanical from here on out. Use any bounce to trim the most extended semiconductor and AI names back toward their respective target weights, and respect the levels that lay below as many of these stocks are extremely deviated from their long-term means. However, for the board market, the table lays out the next support and resistance levels.

The level to watch into next week is 7,156. Hold the 50-day on the CPI print, and the dip buyers are likely to step back in, keeping this a correction within an uptrend rather than a top. Lose it, and the 200-day near 6,858 becomes the conversation.

The Week Ahead & Jobs

The BLS jobs report showed continued strength in the labor market for the third month in a row despite higher oil prices. As we share below, payrolls increased by 172k jobs. Moreover, March jobs were revised up by 29,000, from +185,000 to +214,000, and April was revised up by 64,000, from +115,000 to +179,000. With these revisions, employment in March and April combined is 93,000 higher than previously reported.

This week, the market will get a fresh inflation update via CPI and PPI. Headline and core CPI are expected to come in at 0.4% and 0.3%, respectively. Core PPI, which rose much more than expected last month, is expected to slow to 0.3%, compared to last month’s 1.0%. The inflation data is tricky to forecast due to the volatility in energy prices and the many ways they impact the prices for other goods and services. We suspect the markets will take both inflation figures with a grain of salt, believing that the impact of Iranian inflation is temporary.

Also on the docket are the US Treasury’s 10 and 30-year bond auctions. We will look to see how demand stacks up now that yields are higher. While not well followed, the 7-year auction a week ago was met with extremely strong foreign demand.

Stronger Dollar Trade: The Most Unexpected Macro Bet (Part 2)

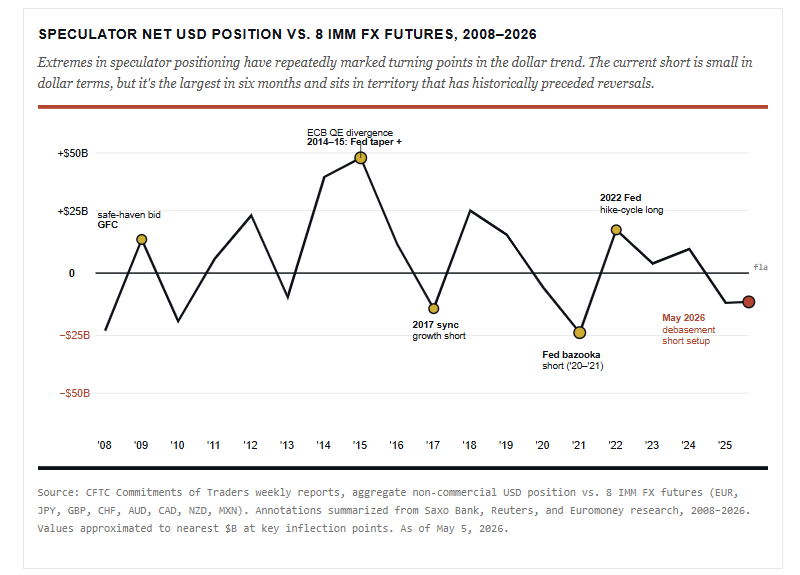

The most crowded short position on Wall Street right now isn’t tech. It isn’t the S&P. It’s the U.S. dollar. Speculators piled into eight straight weeks of dollar selling earlier this year, and asset managers flipped to a net-short DXY position for the first time in months. Every macro fund I read is leaning the same way: a weaker dollar, higher gold, higher commodities, and debasement everywhere you look. The stronger dollar trade, the trade against that consensus, is the pain trade of 2026. Make no mistake. When everyone leans the same way, the unexpected move tends to come from the other side.

Positioning is the most useful tell in macro, because it tells you who is already wrong. Right now, almost everyone is on one side. Saxo’s COT review for early January showed the non-commercial dollar short across IMM FX futures running near $11.9 billion, the largest bearish bet in six months. Asset managers had flipped to net short DXY for the first time since mid-October, lining up with leveraged funds in a bearish view. As Bob Farrell’s Rule #9 reminds us, when all the experts and forecasts agree, something else is usually about to happen.

Here’s the problem with that argument. The debasement thesis assumed the Fed would cut. It assumed inflation would soften, and the euro, yen, and emerging-market currencies would catch a bid as global growth picked up. None of that has happened. April CPI ran 3.8%, the hottest since May 2023, and Producer prices (PPI) came in at 6% year over year, the fastest pace since 2022. Core PPI, excluding food and energy, hit 5.2%. Traders have priced out Fed cuts for all of 2026, and the odds of a year-end rate hike have climbed back to near 35% to 39%. The thesis behind the dollar short has fallen apart.

Tweet of the Day

New UPDATED Trading Rules With Desktop Printout

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.