Amazon (AMZN)

This week, we look at one of the great growth stories of the internet era. Amazon went public in May of 1997 with a mere 256 employees. Adjusted for stock splits, the IPO price was 7.5 cents a share. That equated to a market cap of $438 million at the time. Today its market cap is a hair over $2 trillion. The stock has returned an average annual return of 34%.

While AMZN looks excellent in the rear-view mirror, let’s see what its prospects are going forward.

Fundamentals

Despite its massive market share in online shopping, Amazon continues to grow its revenues at a substantial clip. Furthermore, its growth is much more significant than the economy’s aggregate growth rate and that of online shopping. While its 5-year revenue growth rate has slowed considerably, it still stands at 19%.

The second graph shows that EPS is also slowing, but its growth rate is still considerable at 23%.

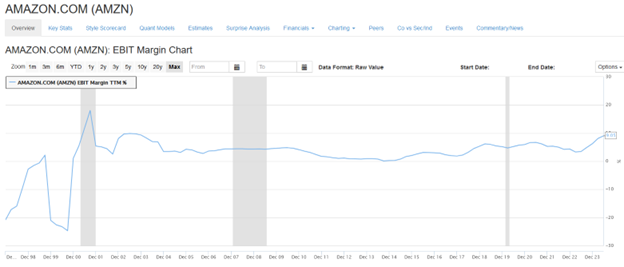

The graph below, courtesy of Zacks, shows that its margins are improving. While most of the goods it sells on its website have low margins, its Amazon Web Services (AWS cloud services) division has substantial growth with high margins. However, the market is slowly becoming saturated with cloud services. Revenue growth will slow considerably in time due to weaker volume growth and more price competition. Currently, they manage about a third of the cloud market. The Zacks chart shows the bump to its margins, which started in 2014 due to AWS. Over time, the margin growth will moderate and likely begin to decline as its cost and sales advantages for AWS dissipate.

The following graph, courtesy of Statista, is a good reminder that Amazon is much more than an online retailer. Accordingly, their valuations deserve to be higher than those of other large retailers like Walmart, Costco, and Target, often considered their competitors.

Currently, AMZN has a P/E of 45 and a P/S of 3.40. Walmart has lower valuations with a P/E of 33 and a P/S of 0.96. However, AMZN has a PEG ratio of 1.75 compared to 5.17 for Walmart. The PEG ratio factors expected earnings growth into the P/E calculation. Therefore, compared to Walmart, AMZN has a much lower valuation when future growth is considered.

One potentially significant risk to be aware of is legal. The FTC and 17 state attorneys sued the company in 2023 for anticompetitive actions and unfair strategies to illegally maintain its monopoly power. It would not be surprising to see more attacks from the government, especially if Kamala Harris wins and follows Biden’s stricter stance on monopolistic behaviors.

The short-term graph below shows AMZN heading back to its pre-August highs. However, its MACD and RSI are starting to get overbought. The stock may hit a new record high, but it could see a short pullback or period of consolidation afterward.

The weekly longer-term graph is more bullish. It shows the weekly MACD is just turning up on a buy signal after the stock bounced off its 100-week moving average. The RSI is a little high but still has plenty of room to improve, and it could potentially stay overbought for a period as it has in the past. On September 23, we added 1% to our AMZN position in the equity model.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.