Campbells Soup (CPB)

We recently sold Philip Morris (PM) in our Dividend Equity Focused portfolio and have been looking for a replacement. One potential addition that we have been researching is CPB. Accordingly, we think it’s worth sharing our fundamental and technical thoughts on the stock.

Fundamentals

Like PM, CPB is a low-growth company. Over the last fifteen years, its revenues, as shown below, have grown annually on average by 1.5%. Moreover, earnings per share also exhibit meager growth. CPB is trading about 15% above its average fair value.

CPB is buying back its shares but not at a pace that is meaningful enough to alter its EPS growth. CPB pays a $1.48 annual dividend, costing the company approximately $450 million per year. Its free cash flow tends to fluctuate between $750 million and $1 billion, leaving plenty of room to continue offering the dividend and possibly increase it. While its ability to pay its dividend is strong, the dividend yield is approximately 3%. It is about 1.75% higher than the S&P 500 but below that of similar companies, offering little earnings and sales growth. See the next section on the dividend yield analysis for more on fair value pricing based on its dividend.

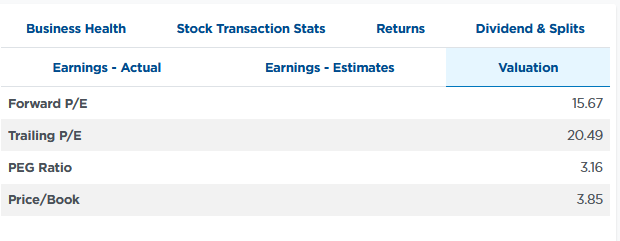

CPB has high valuations, considering its minimal growth. We would prefer to see the PEG ratio much closer to 1. Its price to sales of 1.60 is near the highest level of the last 15 years.

The technical graphs below show that CPB has been on a nice run, which helps explain its higher-than-normal valuations. A correction would likely bring the stock back to its fair value on a fundamental and technical basis.

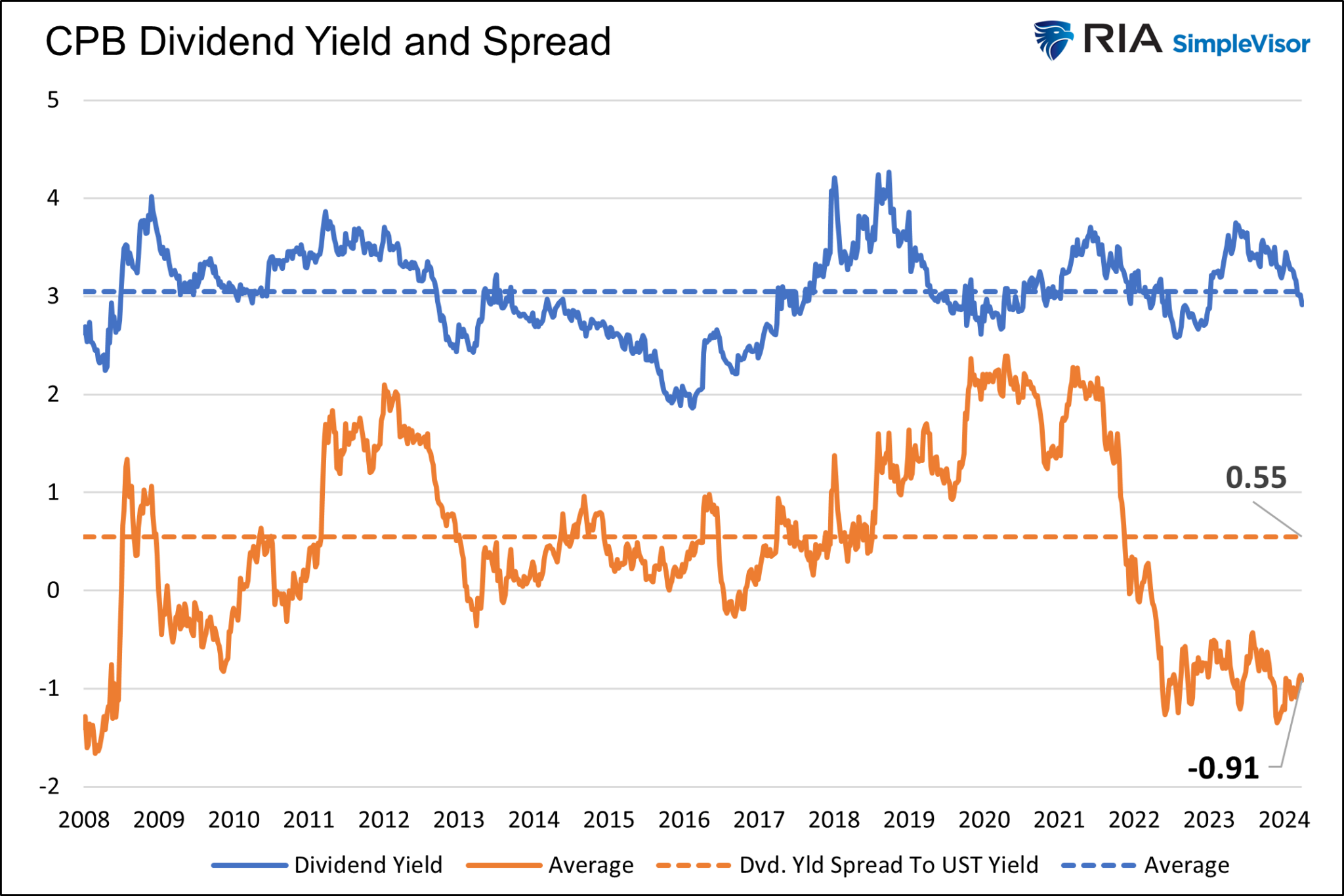

While CPB is technically an equity, its minimal growth rate and consistent dividend make the shares somewhat similar to a bond. As such, we include the following analysis to determine a fair value based on its yield difference versus a risk-free 10-year U.S. Treasury.

The following graph charts the dividend yield in blue and the dividend yield less the 10-year UST yield in orange. As shown, the dividend yield is very close to its long-term average. However, the difference, or spread, between the dividend yield and the UST yield is 1.46% below the historical average. This is troubling as a shareholder should demand a yield greater than the risk-free rate.

Either investors expect the 10-year UST yield to fall by 1.50% to 2.33%, or shares of CPB are overpriced by about 34%. The potential outcomes are not binary; there may also be a middle ground between the two options. However, barring a sharp decline in Treasury yields, this exercise argues that CPB shares are expensive on a dividend yield basis.

Technicals

The shorter-term graph below shows that CPB shares have performed well recently. It is up about 15% year to date. Since the S&P 500 peaked in mid-July, CPB has increased by about 10%. That is much better than the S&P 500, which is still below the peak. While recent history is encouraging, its MACD and RSI are significantly elevated. The MACD is likely to turn into a sell signal. The shares would be more attractive at around $45 from a technical perspective.

The longer-term graph below shows that CPB shares have gone nowhere for the last four years. While its MACD still presents some upward potential, its RSI is extreme. A dip to $40 would be a great buying opportunity, but the 50wma may provide support at $44. A decline to the low $40s would bring its valuations back to normal and boost its dividend yield. Furthermore, it would return it to the average fair value we shared earlier.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.