Diamondback Energy (FANG)

On December 15, 2023, we added Diamondback Energy (FANG) to our equity model to boost our holdings in the energy sector. Diamondback’s cheap valuations and exposure to the Permian Basin, with its abundant shale oil, were key factors in our decision-making. Additionally, we suspected that FANG’s Permian Basin assets might be desirable to a larger energy company. As such, we thought the odds that FANG could be purchased at a premium were moderate.

Since then, FANG has risen over 15% despite the energy sector (XLE) increasing by a mere 2% over the same period. The strong outperformance is not the result of the rationales we share above. Instead, FANG purchased one of its largest competitors, Endeavor Energy Resources. Endeavor is a private company, so its financial situation is not readily available.

The deal is estimated to be valued at $26 billion and should result in $600 million in annual cost savings. The combined company will have about 840,000 acres and 6,100 profitable drilling locations if crude oil is above $40 a barrel.

From what we have been able to ascertain, FANG bought Endeavor for a cheaper than market price. For example, management estimates that post-deal EBITDA should surpass $5 billion, reducing its EV-to-EBITDA ratio from 5.6 to slightly below 5.0. Typically, the acquirer’s shares in a merger fall in price, but in this instance, the market seems to concur with management that they bought Endeavor cheaply.

Given the intense competition for resources in the Permian Basin, FANG may now be a bigger prize for one of the larger oil exploration companies.

We reduced our allocation to FANG on Wednesday as the stock is technically overbought.

The following sections on valuations and fundamentals do not include the addition of Endeavor.

Valuations

Despite the recent price action, FANG’s P/E is 9.67, on par with its two-year average. Its P/S is 3.91, well above that of the larger energy producers but in line with FANG’s recent trends. FANG is susceptible to higher interest rates, especially if they borrow to help fund the Endeavor transaction. However, they plan on using Endeavor’s cash to help minimize its borrowing needs. Its long-term debt-to-equity ratio was 36.68% before the transaction. Such is well below the 65% mark it stood at in 2020.

Fundamental

FANG’s growth rate commensurate with their drilling growth in the Permian Basin is slowing. However, revenue has grown at a 30% annualized rate over the last five years. Such is much higher than its larger competitors. The depletion of shale wells is much quicker than that of traditional wells; thus, FANG needs to consistently add properties to maintain high growth rates.

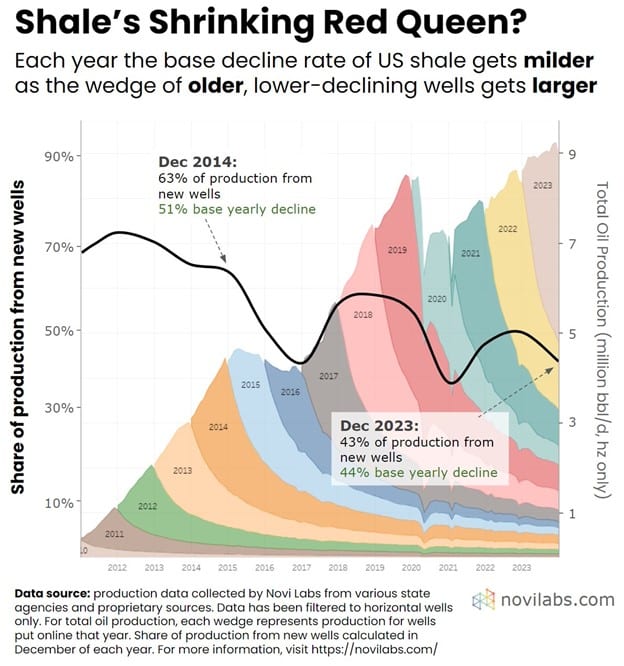

The graph below helps highlight the growth problem with shale oil production. Shale wells decline much more rapidly than non-shale in the first year of drilling. The graph shows that wells drilled in 2023 account for four of the nine million barrels per day produced in 2023. While finding new wells gets more difficult each year, the base production from older wells grows and provides an excellent long-term revenue source.

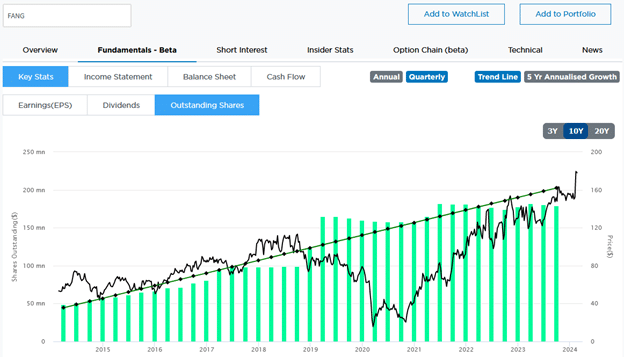

FANG’s share count has remained relatively stable, but they are expected to issue shares to fund the transaction partially. In the future, when less money is devoted to new exploration, excess earnings may be used for share buybacks.

Technical

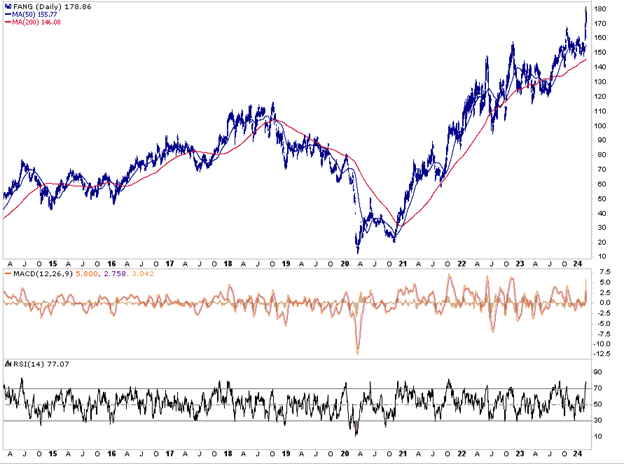

As shown below, FANG is overbought with its RSI and MACD at prior peak levels. Further, it is extended by over two Bollinger Bands from its trend. A pullback is likely short-term, which might provide a better price to initiate or add exposure.

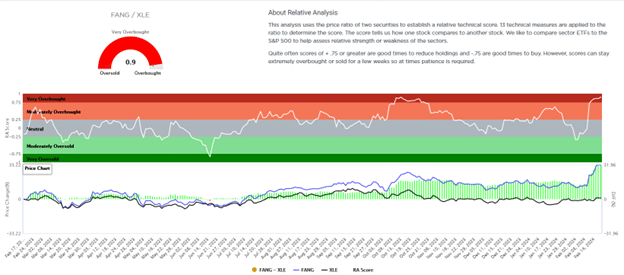

The second graphic shows its SimpleVisor relative score versus XLE, now .90. Simply FANG is grossly overbought versus the industry.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.