Entergy (ETR)

Entergy (ETR)

Entergy is primarily engaged in distributing electric power and natural gas services in Arkansas, Louisiana, Mississippi, and Texas.

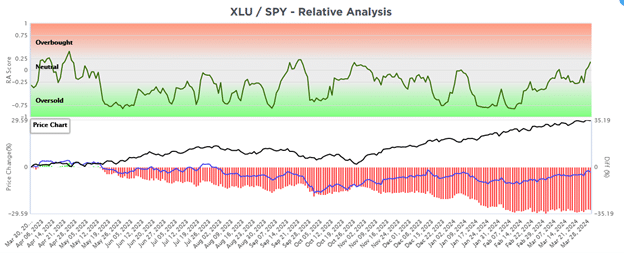

The Utility sector has grossly underperformed the S&P 500 over the last year. The SimpleVisor graph below shows the relative score of the XLU-SPY price ratio, which has been oversold (<0) since last October, although it recently turned positive. Further, XLU has stopped giving up ground to the S&P 500 since February.

We hold a 4% stake in DUK in our equity model and 4% of XLU in the sector model. We are considering adding to both. Accordingly, we will review ETR in this week’s Friday Favorites as it could diversify our existing holding.

Valuations

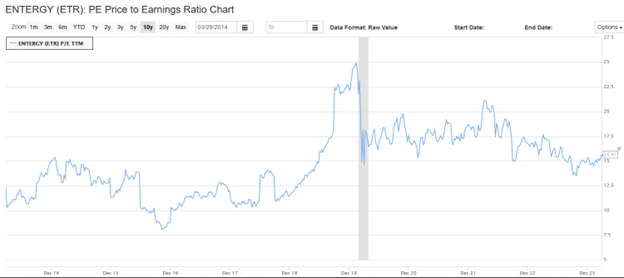

ETR’s P/E is 15.61, the lowest since 2018, albeit higher than its levels in the five years before that. For context, XLU’s P/E is 19.31. Higher interest rates have dragged on valuations in the utility sector as investors have demanded higher dividend yields (lower prices) due to competition from the bond market.

ETR has a debt-to-equity ratio of 176%. That is generally higher than its competitors. For context, consider the largest utility companies below:

- Nextera (NEE) 128%

- Constellation (CEG) 83%

- Southern 178%

- Duke (DUK) 159 %

Fundamental

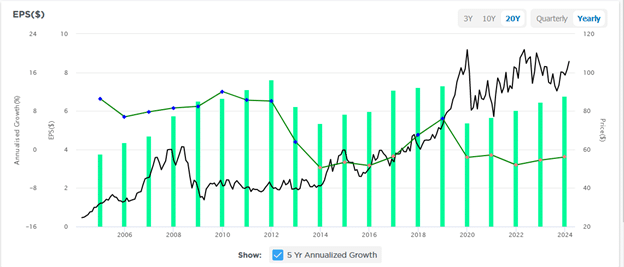

Like much of the utility sector, earnings and revenue growth are low. Investors will overlook meager growth for cheaper valuations and higher-than-market dividend yields. As shown below, ETR’s EPS growth is slightly under 4%. Its current EPS has been trending higher for the last five years but below its prior peaks. Its revenue growth has been flat over the last five years, and, like EPS, it is below previous peaks.

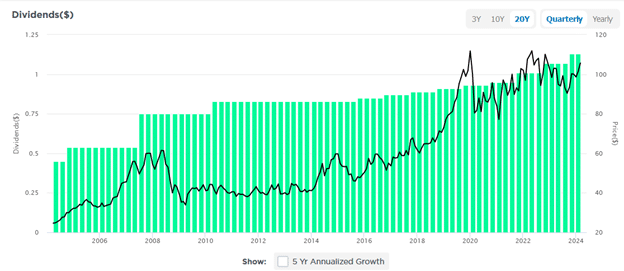

The graph below highlights that ETR has steadily increased its dividend since at least 2005. Further, since 2016, they have improved it annually. The current dividend yield is 4.11% compared to 3.32% for the XLU sector ETF.

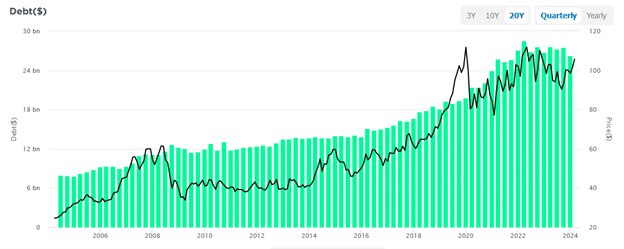

As noted earlier, utilities tend to have higher debt levels. ETR’s debt level, which was trending higher, stopped increasing over the last two years. Higher interest rates will weigh on ETR’s interest expenses. However, of their approximate $25 billion in debt, less than $4 billion matures in 2024 and 2025. Thus, refinancing existing debt at higher rates shouldn’t be too accretive to its interest expense. Over half of their debt matures in 2034 and beyond.

Technical

The chart below is probably the most important regarding ETR’s past and future performance. The correlation between ETR and ten-year Treasury yields has been decidedly negative since 2023. As yields rose, ETR declined. While valuations and fundamentals are critical to evaluating ETR, the direction of yields may be the most essential factor for ETR today. If yields continue lower, ETR should do better or at least outperform the broader market. Given its higher-than-average debt levels versus peers, falling yields may also result in outperformance within the sector.

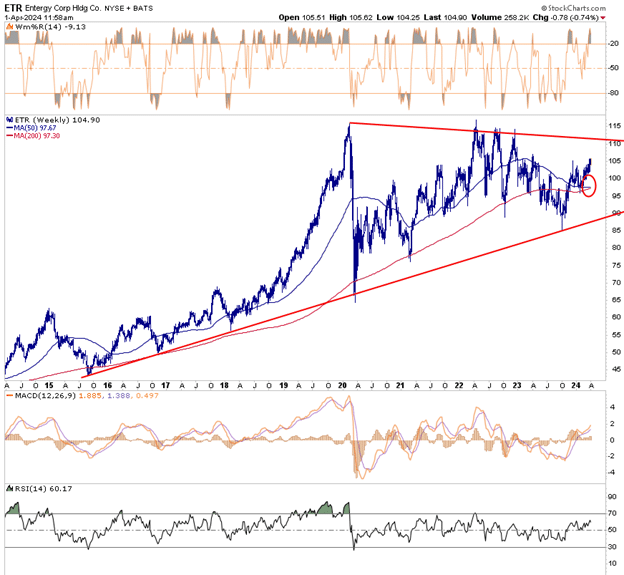

The weekly chart below shows that ETR has been in a long-term uptrend, but it has been oscillating in a 25-point range over the last four years. The Williams %R and RSI point to slightly oversold conditions and argue for a pullback. Also of concern is that its 50-week moving average is in danger of crossing below its 200-week moving average.

While the technical graphs are not as positive as we would prefer, there are other considerations. First is the possibility of a broad sector rotation from mega-cap stocks to those sectors, like utilities, that have been underperforming. Further, as we note, the price of ETR and utilities generally correlate well with yields. Therefore, the direction of yields over the coming months should be followed closely. If inflation or employment data in the coming months are weak, the markets may start pricing in more Fed rate cuts, pushing yields lower and presumably ETR higher.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.