FedEx (FDX)

Wednesday’s Commentary observed poor performance in the transportation sector with a focus on its weakest component, FedEx (FDX). We will follow up with a more in-depth analysis of FedEx.

Fundamental

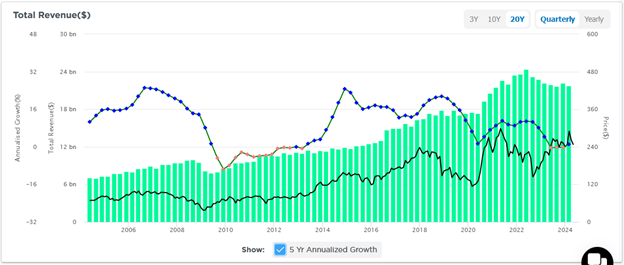

FDX earnings and revenue growth are stagnating. As shown below, revenue has been relatively flat since 2020. The dotted blue line tracking its 5-year annualized revenue growth has been decreasing since 2014 and is now flirting with 0%. Considering the recent high inflation rates, its real revenue growth has been negative for the past few years.

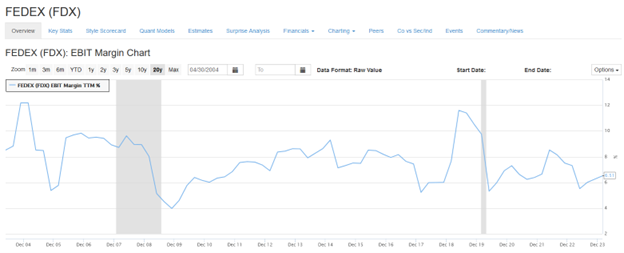

The graph below shows that its operating margins have decreased slightly over the last 20 years. Assuming the minimal revenue growth and flat to declining margins continue, we should not expect its earnings to grow appreciably.

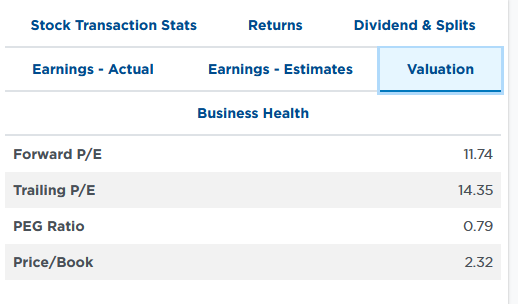

As a result of the weakness in its stock prices, its shares are priced at a low valuation, as shown below.

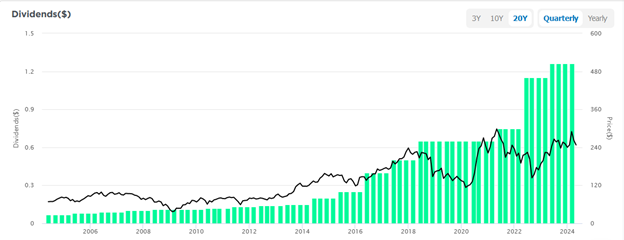

From a dividend perspective, we can be a little more optimistic about the stock’s outlook. As shown below, FDX raises its dividend almost every year. Currently, the shares boast a 2.05% dividend yield. To support future dividends, the company sits in an enviable $5 billion cash position and has had positive cash flow in only one-quarter of the last five years.

The company faces increasing pressure from Amazon. Amazon has moved away from using FedEx and its competitors in favor of its own shipping services. Given limited growth opportunities, FDX has recently been focused on cost-cutting measures. In April 2023, FDX announced its DRIVE initiative to cut $4 billion in costs by the close of 2025. Per their CEO, Raj Subramaniam:

“We are right sizing our cost base to match today’s realities and creating a more efficient and agile network,”

“We’re not simply taking out cost, we are simultaneously focused on running our business more efficiently, flexibly and profitably, which will create significant value for our stockholders in the years to come.”

Unfortunately, cost savings can only help margins and earnings so much. Without new sources of revenue or a change in the competitive nature of their industry, we worry that FDX is becoming a low-growth cash cow. While dividend hunters may appreciate that, those seeking growth could be disappointed.

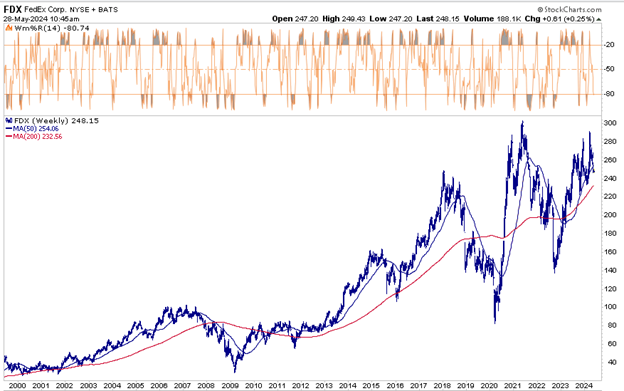

Technical

The graph below shows the share price of FDX has been flat for a year. All the while, the S&P 500 is up 26%.

The longer-term weekly graph shows a strong uptrend over the last 25 years. Furthermore, the stock is sitting on its 50-week move average, which may provide some support at current levels. However, if it breaks lower, we suspect the 200-week moving average may represent new support. A break below that and the 2022 lows may be revisited.

While the technical situation does not look bad, we are concerned that its fundamental data and heightened industry competitiveness bode poorly for its earnings and ultimately will weigh on the stock price.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)