Genuine Auto Parts (GPC)

GPC was founded in 1928 and has become a leading automotive and industrial replacement parts distributor. Approximately two-thirds of its sales come from its automotive division. The company has over 10,700 retail locations in 17 countries.

We recently added a 1% “starter” position in our equity model and hope to add more shortly.

GPC is a dividend aristocrat that has posted consecutive dividend increases for the last 68 years. Its dividend yield is about 2.50%, over 1% more than the S&P 500. GPC has grown its dividend at a nearly 6% compounded rate over the last five years. It also “pays back” shareholders via a consistent share buyback program, as shown below. Assuming a constant valuation, we estimate the buyback is worth an additional .75% yearly.

Macro Picture

Per Statista, the average age of U.S. vehicles is 12.5 years, which has steadily increased from 11.7 in 2018. With higher used and new car prices and high auto loan interest rates, car owners are likelier to hold on to cars for more extended periods. Appropriately, repair expenses tend to rise with the car age, which should benefit GPC. The possibility of a recession and higher unemployment rate should also lead some to hold onto older cars rather than buying a new car.

Fundamental

GPC is generally regarded as a value stock. It has a forward P/E of 15.8 and a P/S ratio of .97. Per the Zacks graph below, its forward P/E is at the lower end of its ten-year range. Its P/S ratio is currently in the middle of its ten-year range.

If their P/E gravitates to its longer-term average (18) over the next 3 years, and they buy back shares at the recent pace and continue to pay the current dividend, investors can expect an annual total return of nearly 8%. The potential return increases if they meet their estimated 5-8% EPS growth over the next three years.

GPC is in a solid financial position, running almost $1 billion in free cash flow annually. In addition, it has over $1 billion of cash and marketable securities on its books. Its long-term debt-to-equity ratio is 111.95%, which is high but manageable given its cash and free cash flow.

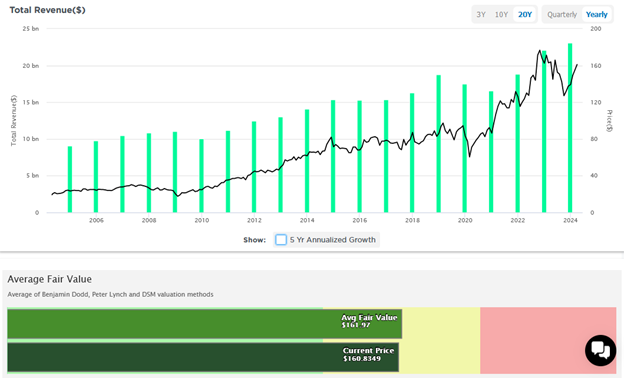

Revenue has grown steadily for the last 20 years, as shown below. The lower part of the graphic shows it is trading slightly below fair value.

Technical

Short term, GPC is slightly overbought. As shown below, its RSI, Williams %R, and stochastics all indicate the possibility of a short-term downtrend or consolidation. A retreat back to its 50-day moving average (153 -yellow) would be a good place to buy or add to GPC.

The longer-term graph looks more promising. It recently broke out of a bullish flag pattern. The third graphic shows what a textbook bullish flag looks like. A break above the flag’s upper resistance often portends another leg higher. The resistance was broken and retested two weeks ago. We would like to see GPC continue to trade above the long-term support line, which currently sits at $150.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)