Leggett & Platt (LEG)

Recently, a reader asked us to evaluate Leggett & Platt (LEG) stock. They were curious to see if it was worth owning, given the nearly 9% dividend yield.

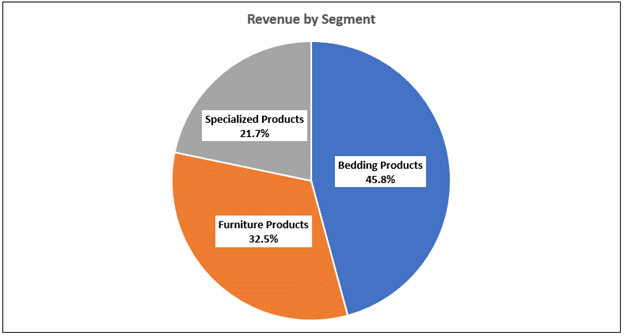

LEG designs, manufactures, and sells home furnishings and appliances worldwide. It operates through three segments: Bedding Products (45.8%), Furniture, Flooring & Textile Products (32.5%), and Specialized Products (21.7%). The stock has a market cap of $3.1 billion and belongs in the Consumer Discretionary sector.

The company is sensitive to housing market trends, including existing and new home sales. Existing home sales are happening at the slowest pace in at least 20 years. Meanwhile, durable housing-related goods sales face headwinds from inflation’s impact on the consumer. Households may choose to delay discretionary purchases in response to waning excess income.

Conversely, falling interest rates could be a boon to both sales and profitability. It’s unlikely that the company will see another period like the pandemic, where stimulus checks and boredom led to widespread home renovation.

Fundamental

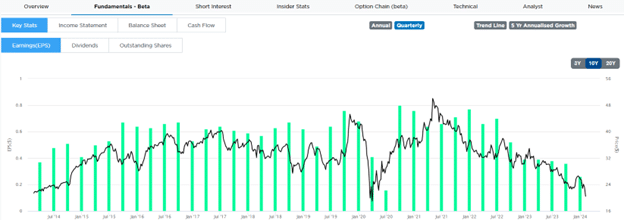

LEG trades at a P/E of 15, at the lower end of its range over the past 15 years. Despite its relatively low valuation, low growth expectations result in a PEG of 3.6. Revenue growth has matched the industry’s 3% CAGR over the last 15 years. On the other hand, earnings have been coming in weak on the back of higher raw materials prices and weakening demand, as shown below.

Its long-term debt-to-equity has been on a consistent uptrend over the past 15 years. Furthermore, about 15% of the debt on LEG’s balance sheet matures in November. The coupon on the maturing debt is 3.8%, while the debt currently yields 6.37%. This leaves the company vulnerable to rolling over debt at higher rates, an additional margin threat. Furthermore, the company is rated BBB- leaving it vulnerable to a downgrade to junk status.

As mentioned above, the dividend yield is nearly 9%. However, weak cash flow trends have put that dividend into jeopardy. Over the past ten years, LEG has paid 50%-70% of its earnings via dividends. The payout ratio eclipsed 100% in the 2nd quarter of 2023 and currently sits at 130%. LEG has raised its dividend annually for 52 years, so management will likely pull out all the stops before cutting the dividend. This could result in layoffs, or other restructuring means to maintain LEG’s dividend aristocrat status.

Technical

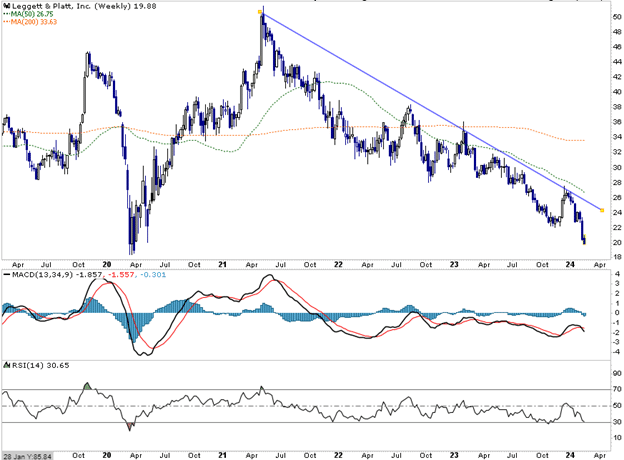

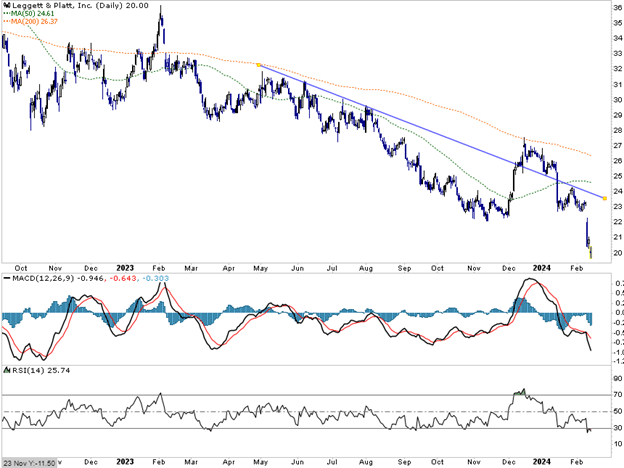

The first chart below highlights the downtrend forming since mid-2021 on a weekly timeframe. The second chart is on a daily timeframe and confirms that the extended weakness is not showing signs of reversal. The RSI is approaching oversold levels on the daily and weekly charts, arguing for a countertrend rally, perhaps to downtrend resistance near $23.50 or $24. The weekly MACD is in oversold territory but still has room to decline more. Meanwhile, the daily MACD is very oversold, but there’s no indication of it beginning to turn up.

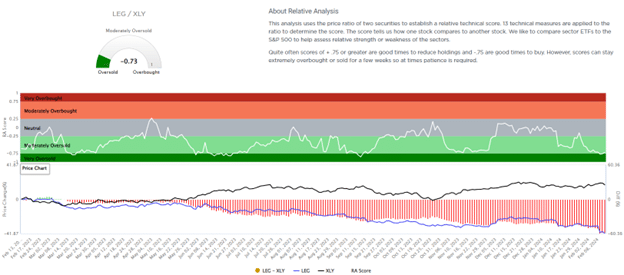

Lastly, the stock is very oversold compared to the Consumer Discretionary sector. LEG may outperform the broad sector and market in case of a market correction due to its relative cheapness. Despite the tempting dividend yield, the challenging fundamental and technical aspects make this stock one to avoid for the time being.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.