Bitcoin’s sharp rally following the election has reinvigorated interest in the Cryptocurrency. Bitcoin’s accessibility to various classes of investors has evolved over the past few years. Investors can now gain exposure to Bitcoin on stock exchanges through Bitcoin ETFs, but in the past, equity investors had to get creative to gain exposure to Bitcoin (BTC). In this week’s Friday Favorites, we check in on one of the original Bitcoin proxies, MicroStrategy (MSTR). MSTR is a leveraged bet on the price of Bitcoin, given that the company issues debt and uses the proceeds to purchase Bitcoin.

The company is the fourth-largest holder of BTC, owning 402,100 BTC. However, it started as a software company and evolved into a leveraged bet on BTC. In October, we wrote the following in our Daily Market Commentary:

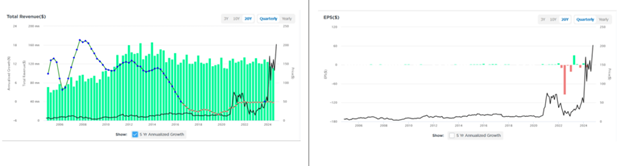

Per its website, MicroStrategy “provides software solutions and expert services that empower every individual with actionable advice.” While Microstrategy’s mission description may seem like a profitable enterprise, reality has a different opinion. Since 1997, the company has a cumulative net loss of $1.108 billion. Accordingly, the graphs below show its revenue has been flat to slowly deteriorating for over ten years. Its EPS on the right also shows the company’s poor fundamental status. However, as both graphs show, the price of Microstrategy has risen by over 1,300% over the last five years.

Fundamental

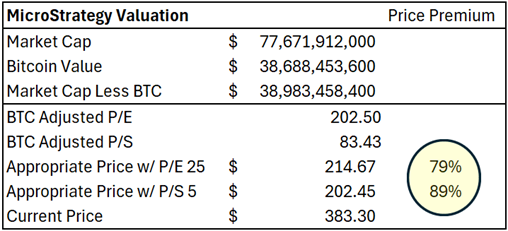

We previously mentioned that MSTR has become a vehicle for making a leveraged bet on the value of BTC. Below, we dissect the company’s valuation to evaluate the premium investors are paying for the underlying company. The company’s market capitalization, less the market value of its BTC holdings, gives us an idea of the value placed on the underlying company. Combining that metric with the TTM recurring EPS, we see the underlying business trades at an astronomical P/E of 202.5. Similarly, P/S is “headed to the moon” at 83.4.

Next, we make a naive assumption that the appropriate P/E and P/S ratios for the underlying business are 25 and 5, respectively. These are very generous assumptions, given that the underlying business has exhibited very little revenue and EPS growth over the long run, as shown in the second chart below. Under these conditions, we calculate the fair value price of MSTR, including its BTC position, to be somewhere between $202.45 and $214.67. Thus, even with generous growth assumptions, investors are paying an 80%-90% premium over fair value to hold shares of MSTR. With both leveraged and unlevered Bitcoin ETFs now available on stock exchanges, it’s mind-boggling that investors would pay such a premium for MSTR.

Technical

MSTR traded in a range for most of this year, but the price began taking off heading into the election. After Trump’s victory, the stock exploded, commensurate with the price of Bitcoin. As shown below, the MACD recently turned to a sell signal from a high level, and RSI is cooling off. However, the price appears to be forming a symmetrical triangle. If the price of BTC breaks out above $100k, the stock will likely break out of the triangle and continue its bullish trend. If the stock trades below the blue support line, it should find resistance around $300.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.