Quanta Services (PWR)

Last week’s Friday Favorites discussed the merits of GE Vernova (GEV), the power supply-related business segments recently spun off by GE.

This week’s review follows a similar theme. Specifically, vetting companies that will benefit from the coming massive investment to upgrade and expand the nation’s power grid to accommodate AI data centers and EVs.

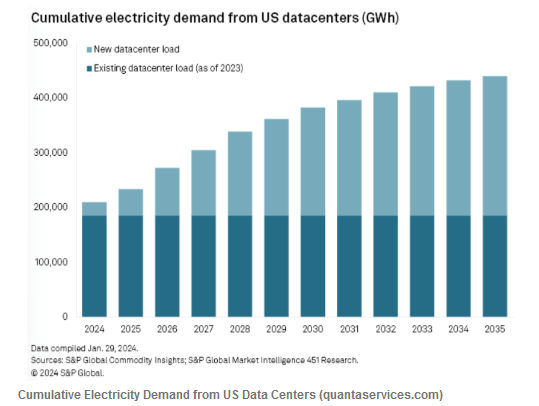

The graph below from Quanta shows that the demand for electricity from AI data centers will more than double over the next ten years.

Quanta provides infrastructure solutions for electric and gas utilities, renewable energy, communications, pipelines, and energy industries. The company’s Electric Power Infrastructure Solutions segment engages in the design, procurement, construction, upgrade, repair, and maintenance of electric power transmission and distribution infrastructure and substation facilities; installation, maintenance, and upgrade of electric power infrastructure projects; installation of smart grid technologies on electric power networks; and design, installation, maintenance, and repair of commercial and industrial wirings. The company’s Renewable Energy Infrastructure Solutions segment is involved in the engineering, procurement, construction, repair, and maintenance of wind, solar, and hydropower generation facilities, as well as battery storage facilities, and provision of engineering and construction services for substations and switchyards, transmission, and other electrical infrastructures. The company’s Underground Utility and Infrastructure Solutions segment offers design, engineering, procurement, construction, upgrade, repair, and maintenance services for natural gas systems for gas utility customers; fabrication services for pipeline support systems and structures and facilities; and engineering and construction services for pipeline and storage systems, and compressor and pump stations.

Quanta and GE Vernova will be direct competitors in many products and services listed above.

Fundamental

Over the last three years, Quanta’s revenue growth has picked up. This is impressive, given that it is relative to an already high annualized growth rate of 12.8% over the previous ten years. Its EBITDA has followed a similar path, which is affirmed by its consistent EBITDA margin of around 9%.

Quanta’s long-term debt-to-equity ratio has fallen recently, from 70% to 50%. This is good as it appears the company can increase its debt balances to help fund the expansion of its services if need be. Furthermore, debt may also be required if it elects to grow via acquisitions, as it has in the past.

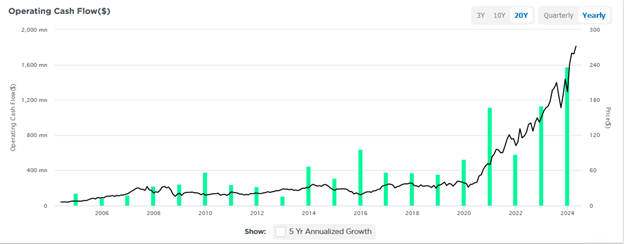

Since 1999, Quanta has acquired 33 companies, spending $5.6 billion on acquisitions over the last fifteen years. Free cash flow can also help fund expansion and acquisitions. As shown below, it has risen rapidly over the past two years.

Earnings growth should continue robustly, especially over the coming five years, as utilities try to keep pace with AI data center growth. While Quanta was previously considered a slow-growth stock for many years, that characterization has changed. PWR is now a high-growth company. However, with double-digit growth come high valuations. Still, its P/E factored for expected growth is reasonable at 1.87, as illustrated by the PEG ratio. Quanta’s P/S is 1.82 (not shown), well below the S&P 500 (2.79).

Technical

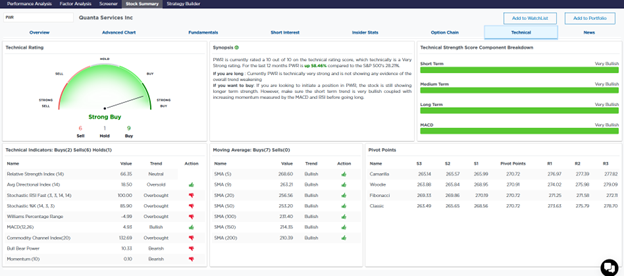

PWR shares have been on a tear. Over the last 12 months, PWR has been up more than 2x the S&P 500. The table below sums up its technical outlook. It is on a strong buy signal, and its technical strength is bullish. However, many shorter-term technical indicators in the table on the bottom left point to overbought conditions.

PWR is due for a pullback or consolidation. Ideally, buying the stock at its 200-DMA ($210) would be nice, but given the market narrative about the substantial growth of AI and the related data centers, investors will likely have to settle for its 50-DMA ($253).

Despite its shorter-term technical situation, a small starter position may be advisable at current levels. As we have seen with other AI-related companies, such as NVDA and AMD, their stocks can become much more overbought.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.