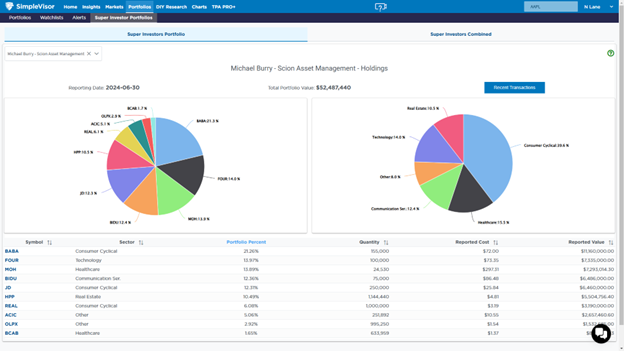

Within the Portfolio tab of SimpleVisor, we share the portfolio holdings of some of the largest and most well-known investors. The portfolios of these “Super Investors” provide insight into the stocks they like and the overall exposure to the market they are taking. We follow up on last week’s payment processing company, Fiserv (FI) with another “Super Investor” pick. This one comes straight from the portfolio of Michael Burry’s Scion Asset Management.

Shift4 Payments (FOUR) is another payment processing company and happens to be Burry’s second largest holding (~14%) behind Alibaba (BABA). His portfolio doesn’t have any exposure to Fiserv (FI), however. Let’s review the fundamentals and technicals to see if we can get an idea of why Burry favors FOUR rather than FI.

Fundamental

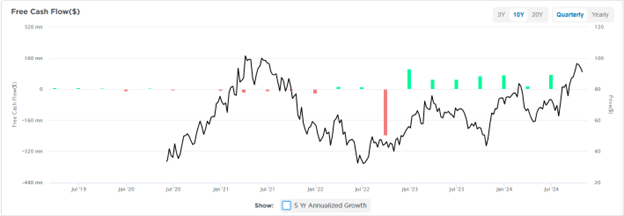

FOUR is part of the payment processing industry. The company was founded in 1999 but didn’t go public until 2020, so the fundamental and technical historical data is limited. It’s a mid-cap stock with a market capitalization of about $8.3 billion. Like FI, part of FOUR’s growth strategy involves making acquisitions. This can be seen in its free cash flow chart, specifically the outlier negative free cash flow related to two acquisitions in the 3rd quarter of 2022. Aside from one-off acquisitions, the company is generating positive free cash flow.

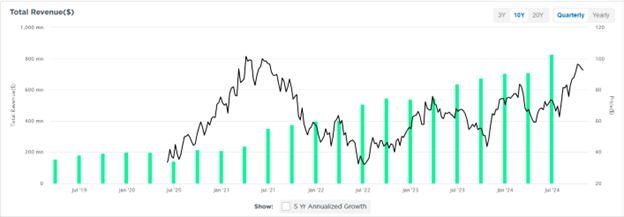

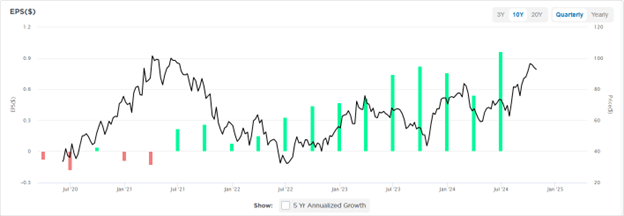

The revenue and EPS charts below show exceptional growth in both categories. There isn’t enough data to display 5 Yr annualized growth on the charts. By our calculations, the 3 Yr annualized growth rates of revenue and EPS are roughly 42% and 325%, respectively. Take the EPS growth rate with a grain of salt, as EPS was just turning positive three years ago. Still, the YoY growth rate of trailing twelve-month EPS is an impressive 42.6%. Revenue and EPS growth are both outpacing that of FI.

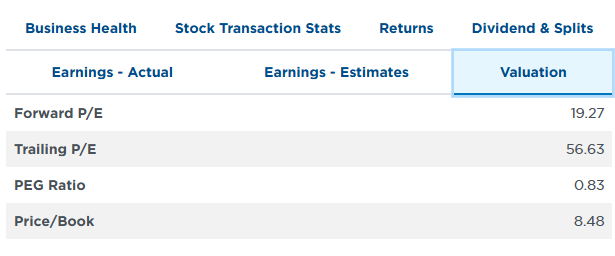

Four trades at valuations comparable with FI. Its forward P/E is slightly lower at 19.27 vs 19.78 and it also has the advantage in PEG ratio (0.83 vs FI’s 1.43) due to FOUR’s higher growth. Its trailing P/E is significantly higher than FI, but that’s justified by the growth differential.

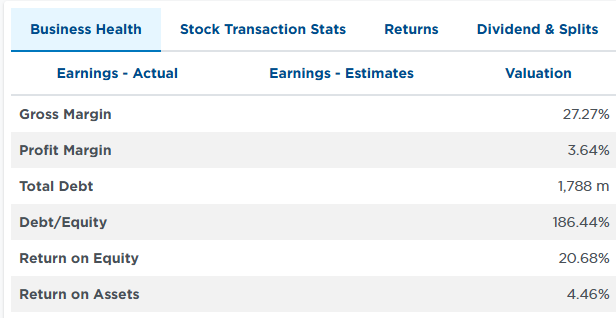

The stock boasts a relatively high ROE (20.68%), as shown in the second chart below. This is nearly double FI’s ROE, but FOUR’s Debt-to-Equity ratio is also more than double that of FI. The two stocks’ Return on Assets are roughly equal; thus, the higher ROE is simply a function of leverage. By dissecting ROA into its Net Margin and Asset Turnover components, we see that FOUR has lower margins than FI but higher asset efficiency. FOUR has an opportunity to raise margins via economies of scale if it can continue growing its market share.

From a fundamental perspective, neither company appears to have a definitive advantage. They have different characteristics, however. FOUR is a smaller competitor with higher growth rates and more risk as well. FI is more established in the industry but isn’t growing as quickly.

Technical

FOUR is working off an overbought position on a short-term basis as pictured in the first chart below. Its MACD turned to a sell signal a few weeks ago and isn’t showing signs of bottoming just yet. The stock could fall another 5% before catching support at its 50-dma ($86.71). If the 50-dma doesn’t hold then the next potential support comes in at $84.25.

The weekly chart below shows that FOUR is at a critical point from a long-term perspective. It recently broke above a resistance line that’s been forming since early 2022. However, the breakout has yet to be confirmed. Confirmation is still in the cards given that the MACD isn’t on a sell signal and RSI is elevated but not overbought. If the stock trades back below resistance, then it could be in for a large correction to continue the trend of rising bottoms. Considering the technical situation and an upcoming earnings announcement, this would be a particularly risky time to establish a position in FOUR.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.