Snow is a data storage platform that allows its clients access to data and analysis of their data from the cloud. SNOW shares have been up about 50% over the last few weeks on strong sales and an optimistic outlook, as reflected in its most recent earnings report. However, despite the robust performance, it is still slightly lower for the year and well below its peak in late 2021.

Fundamentals

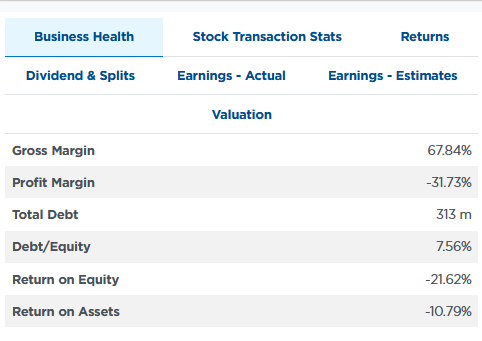

In addition to earnings, recent optimism stems from their partnership with Anthropic. Their joint product allows customers to build generative AI applications and utilize AI models without coding. Furthermore, they have partnerships with Nvidia and Amazon Web Services (AWS) that have helped them achieve a high but not likely sustainable 68% gross margin.

While its gross margin is very high, its net and profit margins are negative as they are not profitable.

Because they have negative earnings, traditional valuation methods are irrelevant. However, earnings per share forecasts provide a forward P/E of 175. Revenue growth, shown below, is the best fundamental guide at this point. As we can see, it has been rising steadily over the last four years.

Competition is an important consideration for SNOW. Databricks has comparable products and strong partnerships as well. Further, with such high gross margins, we suspect that other larger firms are, or will be, competitive with SNOW.

There is speculative fever in the AI space. Some of it, like that for NVDA, is warranted. Some of it is hype. It’s reminiscent of the dot-com crash. Many internet companies did fabulously well, but others went out of business or languished for years after the bust.

Whether SNOW is hype and an outstanding trading stock, or a valuable long-term investment is a tough call. That said, the stock will likely remain volatile until it starts turning a profit and proves it can continue to grow revenue rapidly and turn profits. Another way of saying that is can it prove that its Enterprise Value (EV)/Sales ratio of 12 is fair? Such assumes tremendous growth will occur. An EV/Sales ratio between 1 and 3 is considered normal. Therefore, SNOW is pricing 4x+ long-term growth versus the broader market.

Technical

The graph below shows that SNOW is overbought presently and likely due for a period of consolidation or decline. We would look for support at its 50 dma or 200 dma, which are both around $138. Its MACD just entered a sell signal from levels last seen in 2021.

A break above $250 could set SNOW on course to achieve a series of higher highs. Assuming the AI market stays hyped and SNOW can deliver fundamentally, the 2021 highs are attainable. We are far from the first inning of the AI speculative boom, so we offer caution with such high return outlooks.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)