Stanley Black & Decker (SWK)

Stanley Black & Decker, Inc. is a widely recognized manufacturer of industrial tools and household hardware in the US and internationally. Our Equity models currently have a long position in SWK.

Business Transformation

SWK started underperforming the small and mid-cap benchmark indices in the third quarter of 2021. The company’s margins suffered due to supply-chain and manufacturing-related challenges. Its relative performance worsened throughout 2022 as rising interest rates sparked an exodus from small and mid-cap stocks. In July 2022, SWK announced business transformation plans to optimize its manufacturing footprint and serve customers better. The critical aspects of the plan are shown below.

It’s not uncommon for companies facing growth challenges or economic uncertainty to introduce cost-reduction plans to boost stock performance. However, execution separates the turn-around stories from the stocks that continue lagging.

Thus far, SWK is executing its plans by delivering run-rate cost savings of $1 billion by the end of 2023. Furthermore, the company remains on track to reach its $2 billion target cost savings by year-end 2025. In addition to the cost savings, SWK has bolstered its free cash flow by reducing inventory by $1.7 billion since the plan’s inception. Although SWK has thus far delivered results, the battle is far from over. Achieving the second half of its goal may prove to be more challenging than the first.

“We successfully advanced our strategic business transformation in the third quarter. Our focused execution resulted in improvements versus the prior year in adjusted gross margins* and earnings per share* as well as free cash flow*. These performance improvements provide a solid foundation for additional investments in innovation and market activation to capture the compelling long-term growth opportunities in the markets we serve.”

Fundamental

The fundamental picture today is not great. However, what we find very appealing is its strategic transformation plan. If they can execute as they claim, the fundamental picture would improve significantly, and its stock price would likely follow.

- The P/E on SWK is very high at 215. However, as noted above, this is primarily a function of the costs of executing their business transformation. A more accurate valuation is their forward P/E, which is 20.9. The forward P/E is slightly higher than the pre-pandemic average, but the transformation should improve profitability, which typically deserves a higher valuation.

- While its P/E valuation is elevated, its P/S is low at 0.87. The ratio is the lowest it has been in over ten years. Assuming the company can reduce its expenses, paying a low price for sales should lead to improved profit margins and profitability. In such a case, the P/S ratio could return to its longer-term average of 1.5.

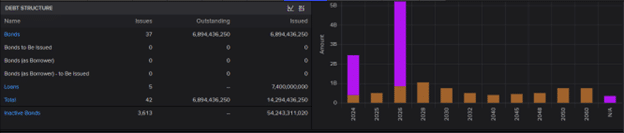

- The table/graph below from Refinitiv shows SWK’s debt structure. 5% of their debt (orange) matures this year. Therefore, the cost of rolling over debt and incurring higher interest expenses is minimal. The loans outstanding (purple) are credit lines that have not been used. Unlike many small and mid-cap stocks, SWK is not at much risk of sustained higher interest rates.

Technical

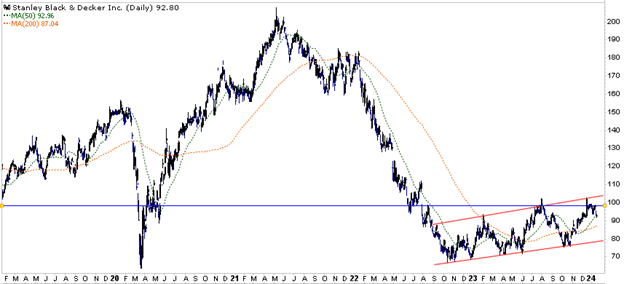

The chart below shows the steep decline in SWK throughout 2022 and the modest recovery that has followed. The red trendlines illustrate that SWK formed a series of higher lows and higher highs throughout 2023. Meanwhile, the horizontal blue line marks support that turned into resistance in mid-2022, which the stock is currently bumping against. SWK may test support in the low 80’s before making another run for the top of the channel.

It’s worth noting that the 50-day moving average recently crossed above the 200-day moving average. This Golden Cross, combined with a break above the uptrend resistance, would be a bullish signal. Setting a lower low would be worrisome.

While the technical picture is helpful in the short run, the drivers of performance over the next four quarters will be dominated by whether the company delivers on its transformation plans. Technical patterns are a good barometer for how the market feels about SWK’s execution of its goals.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)