T-Mobile (TMUS)

Last week’s Friday Favorites ran a stock screen to help identify stocks with high P/E ratios but high anticipated growth rates. In other words, we were looking for GARP, growth at a reasonable price. The results were limited per the paragraph below:

Our screen seeks to find established companies displaying consistent earnings and sales growth. It hinges on a P/E higher than the market, which is justified by expected growth. The screen returned four stocks: Amazon (AMZN), NVIDIA (NVDA), T-Mobile US (TMUS), and Booking Holdings (BKNG).

In this edition, we will dive into T-Mobile (TMUS).

Fundamental

TMUS has grown by purchasing smaller wireless network operators. Its largest purchase was Sprint in 2020. Over the last three years, it has bought four more.

TMUS is the second largest wireless provider, with 126 million subscribers. Only Verizon, with 156 million, is larger. The Statista graph below shows that TMUS has increased its growth while Verizon and AT&T have been relatively stable.

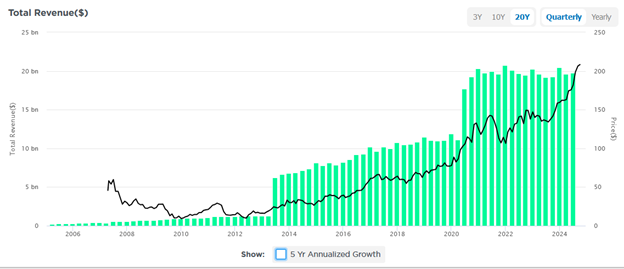

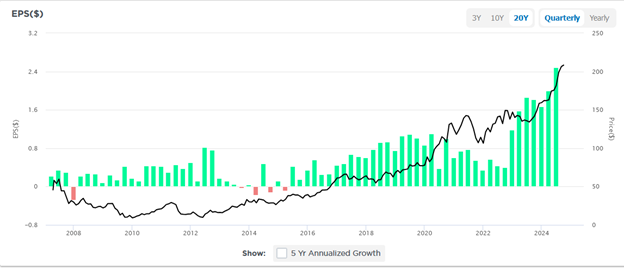

Given its high P/E, can we justify the valuation with high earnings growth prospects? The first graph below offers caution in this regard. Revenues jumped with the Sprint acquisition but have been flat since. Conversely, earnings have been accelerating rapidly, as shown in the second graph below.

Not surprisingly, given flat revenue growth and surging earnings growth, TMUS operating margins have nearly doubled over the last year from 10% to 20%. TMUS carries much less debt than Verizon and AT&T, allowing it more flexibility, especially with higher interest rates. Less debt also enables them to buy back shares, which helps grow EPS.

TMUS also has lower churn rates than its competitors. This allows them to make more money per subscriber as they avoid some of the costs of marketing and onboarding new subscribers. Furthermore, TMUS has reduced its workforce by 7%, further reducing costs.

The industry is very competitive. Accordingly, TMUS must continue to buy market share and reduce its expenses whenever possible. We suspect its recent EPS growth will be more challenging to attain than it has been.

Technical

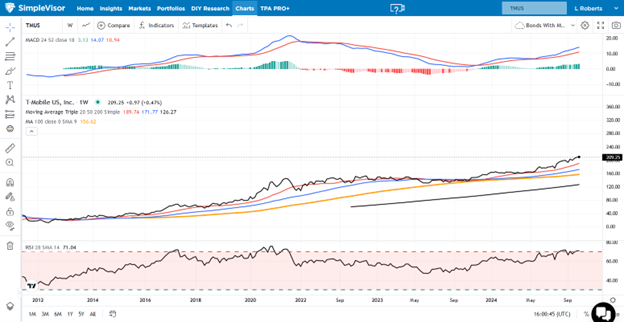

TMUS is considerably overbought from a weekly point of view. While its RSI has been overbought for most of this year, its MACD is significantly higher than in the past 5-years. The good news is that it isn’t showing signs of turning over. If a more significant correction materialized, the first line of support would likely be the prior resistance near $165. Below that, the stock would likely find stability at the longer-term uptrend near $155. Investors looking for an entry point would be better served to wait for a pullback near the 50-dma around $195. If the stock doesn’t catch support at the 50-dma, exercise caution for a larger correction, as mentioned above.

TMUS is also very overbought from a longer-term perspective. While the upward trend can undoubtedly continue, shareholders should be prepared to take profits if the stock starts breaking down.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.