Two Ways to Achieve the Same Outcome?

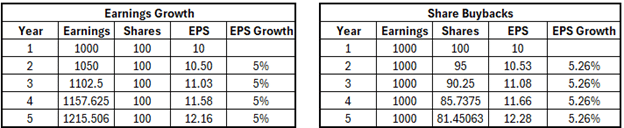

Companies can grow earnings per share (EPS) by pulling on the two levers that make up the ratio. They can attempt to grow earnings by reinvesting in their core business or use that cash flow to repurchase shares. What’s the difference? For a naïve example, assume that a company has two options. Option one is to reinvest its earnings to achieve 5% annual growth. The other option is repurchasing 5% of the shares outstanding yearly. As shown below, from a purely mathematical perspective, there isn’t a meaningful difference between the two approaches to EPS growth. From this simplified perspective, an investor would be relatively indifferent between share buybacks and reinvestment in the business. Unfortunately, the same logic doesn’t hold in reality.

Back To Reality

While there is only an insignificant difference in the source of EPS growth from a purely mathematical perspective, there are substantial differences overall. We will discuss a few reasons, but let’s start with the obvious. Share repurchases aren’t a sustainable method of driving EPS growth, and they may not maximize shareholder value, as is required of the board of a public company.

Taken to the extreme, share repurchases have a finite limit before the company essentially takes itself private. Those repurchases may drive the share price to the point of the company being grossly overvalued versus its growth prospects. At that point, the board would be violating its mandate by repurchasing overvalued shares, and the number of shares repurchased would probably limited by its low growth earnings.

Another aspect is that share repurchases are just a method of returning cash to shareholders, like a dividend. Reading between the lines, for a company experiencing slow growth, a lack of reinvestment may signal that management doesn’t perceive many worthwhile investment opportunities. Depending on the accuracy of this position, it can either be a benefit or a detriment to shareholders.

If a company chooses to buy back shares and turns down investments that would earn a return greater than the cost of capital, they are destroying value. Converesly, if a company undertakes investments that return less than the cost of capital, they are also destroying shareholder value. In that case, share repurchases would be the best action for shareholders.

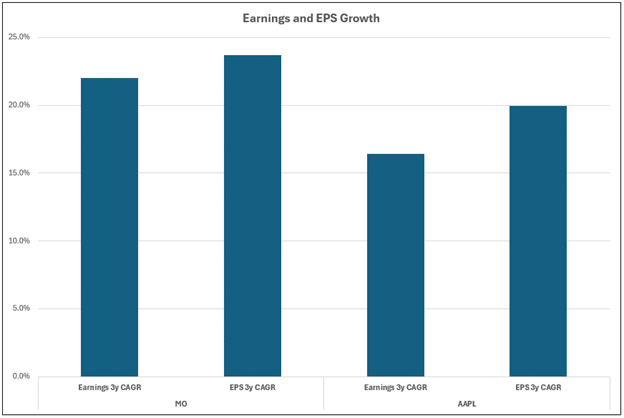

Apple versus Altria

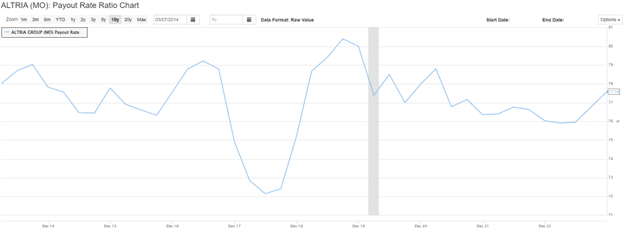

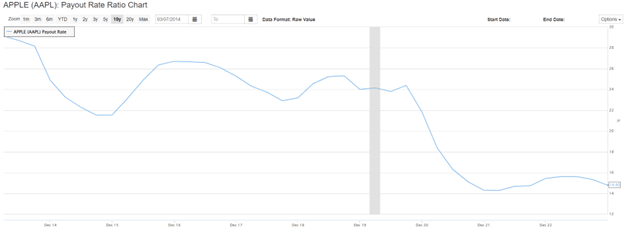

To illustrate the concepts above, we compare two companies in different stages of the growth cycle, Apple and Altria. Using the past three years of data to avoid Covid-related distortions, we’ll look at the differences in payout policy and its impact on earnings versus EPS growth. One way to measure reimbursements to shareholders is the dividend payout ratio, which measures dividends paid to common shareholders as a proportion of earnings over a period. As shown below, Altria has a much higher payout ratio (77.6%) than Apple (14.8%).

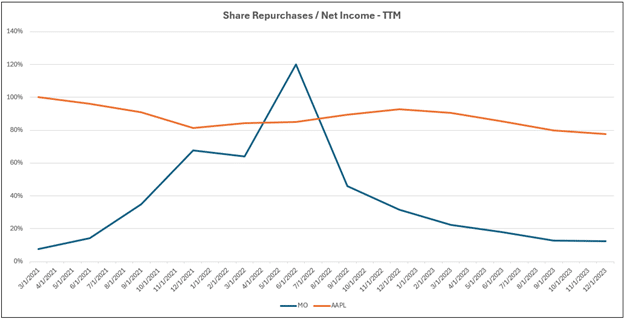

As discussed previously, share repurchases are an alternative way to return cash to shareholders. Thus, we must review both measures to get a complete picture of payouts. The first chart below cements the fact that while MO typically pays out more of its income in dividends, Apple focuses on share repurchases instead. The effect is clear when looking at the second chart comparing the annualized growth rate of earnings and EPS over the past three years. MO’s EPS growth is much closer to its earnings growth rate since dividends are its primary avenue to return cash to shareholders. Meanwhile, Apple creates the illusion of faster growth in its EPS by using share repurchases to return funds to shareholders.

The bottom line is that AAPL trades at valuations consistent with a growth company, while Altria trades like a cash cow. Connecting the dots on payout policy, however, we can see that Apple and Altria behave similarly in that respect. The question we would ask Apple’s shareholders is, do they really understand what they’re buying, and do they think Apple is reinvesting enough to justify its current valuations?

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.