As we wrote in our last Five for Friday of 2023, we are changing the format of this weekly report. From now on, we will spotlight a stock, sector, factor, or theme each week. The content may vary from a fundamental to a technical deep dive on a stock of interest, or as we do in our initial report, both. On occasion, we may run a scan or address a reader’s request.

United Healthcare (UNH)

The first Friday Favorites is on United Healthcare (UNH). We held UNH through part of last year but sold it as it struggled to keep up with the market. Healthcare stocks opened strong on the first days of trading in 2024. If the trend continues, we may consider repurchasing UNH as its fundamentals remain strong.

Technical:

UNH struggled versus the broader markets through most of last year.

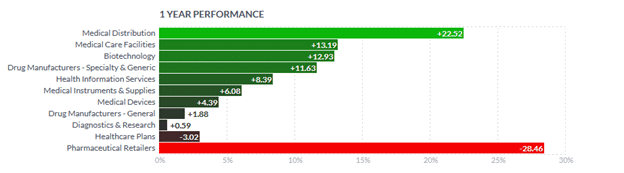

One of the main reasons for the underperformance was that healthcare stocks were out of favor. In 2023, the healthcare sector rose 4.18% compared to the S&P 500 +18.51%. As shown below, healthcare plans (UNH included) fell by 3.02%, making it the second-worst industry within the sector.

Further weighing on the share prices, its CEO raised concerns about a significant uptick in seniors choosing to undergo elective surgery.

The technical graph at the bottom shows that UNH has been consolidating between $440 and $540 for almost two years. We prefer a break above the consolidation for a healthy, longer-term buy signal. Otherwise, trading the consolidation range may be profitable and allow you to be on board if it breaks out higher.

Its MACD will likely bullishly cross and turn higher in the near term. This occurs as the S&P 500’s MACD is high and just bearishly crossed and is turning lower. Such may help UNH outperform the market in the coming month or two.

Fundamentals:

- Revenues continue to trend consistently upward. They have grown 11% annually over the last ten years.

- Earnings are also trending upward at a 6.5% annual clip.

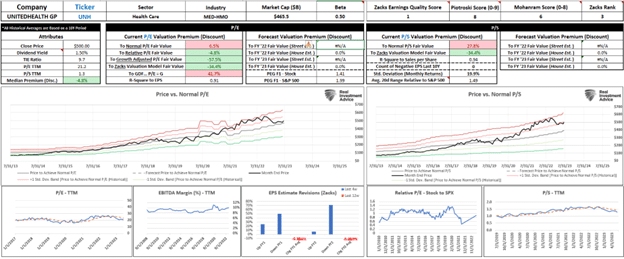

- Its P/E (ttm) is 23.34, which is relatively high compared to its history of the last ten years but below the 25-27 range during 2021.

- Its P/S of 1.38 is also relatively expensive but cheaper than in 2021.

- UNH’s long-term debt to equity at 67.43% stands at an 8-year high but not much above where it has been. Higher interest rates should not weigh heavily on their margins as UNH only has $3 billion of maturing debt in 2024, of $62 billion outstanding. They also have $46 billion in cash, so they may not have to refinance debt until rates decline further. Additionally, they are earning 5%+ on their cash balances.

- UNH has a healthy PEG ratio of 1.66 versus the S&P at 3.03. This is a function of a lower P/E and a higher expected growth rate than the market.

- The SimpleVisor average valuation model (first graphic) shows its current price is about 10% below fair value. The second graph similarly indicates that its price aligns with historical P/E and P/S valuations.

- UNH continues to buy back shares, albeit at a slow clip. That should bolster EPS on the margin.

- UNH has a dividend yield of 1.36%, just slightly below the S&P 500 (1.44%)

Business Outlook:

Rising medical costs and aging demographics are likely to weaken margins over the next ten years, but there is nothing imminent that will likely change their earnings trajectory significantly. Given the political climate and coming election, we think the odds of healthcare reform this year are nil.

Summary:

Given its hefty weighting in the S&P 500 and the dominant role that passive investing plays, UNH is a good long-term holding, especially as it trades close to its fair value.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)