There’s a growing uproar fueled by simultaneously increasing health insurance premiums and claim denials by the largest insurers. The claims aren’t unfounded- this trend is visible in the data. Per Reuters,

Recent data show that patients are now even more likely to have their claims denied, pay more for premiums and medical visits, and face unexpected costs for care they thought was covered by their health plan. Insurers say they work to negotiate down increased fees from doctors and hospitals, as well as costly prescription drugs and medical devices.

With United Healthcare in the headlines lately due to the assassination of the insurer’s CEO, we will examine the company’s stock this week and investigate whether this trend is showing up in its fundamentals.

Fundamental

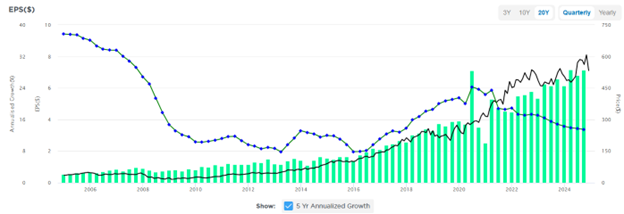

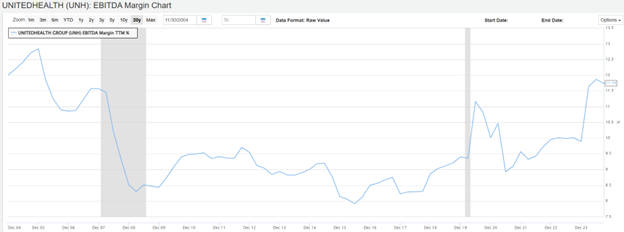

UNH has a solid track record of revenue growth over the last 20-year period. The 5-year average annual growth rate has trended higher over the past few years and sits at a healthy 10.5% as of UNH’s latest quarterly earnings report. EPS also exhibits a solid growth trend, rising slightly faster than revenue over the past 5-years with a compounded annual growth rate of 13.5%. Share repurchases do play a part in the higher EPS growth rate, albeit not significantly. UNH’s share count has declined by less than 1% annually over the last 5 years. The main driver appears to be its expanding profit margins, as shown in the third chart below. Over the past ten years, UNH has expanded its EBITDA margins by a remarkable 2.75% to 11.74%. This margin expansion is partly due to the seemingly effective cost controls mentioned in the introduction.

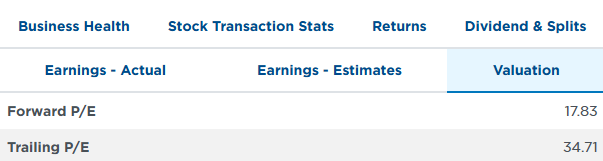

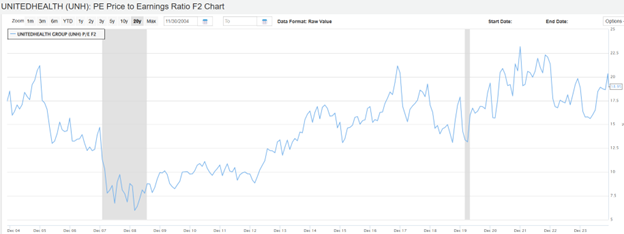

UNH is priced at a significant discount to the target price predicted by the Simplevisor Average Fair Value model. The company trades at a modest valuation from the perspective of its Forward P/E, as shown in the second chart below. However, it trades at a relatively high PEG ratio of 2.67. Accordingly, investors are paying somewhat of a premium given its expected 3- to 5-year growth prospects. This is also evident in the third chart below, showing that UNH has been trading in the upper range of its valuation over the past 20 years. Nonetheless, the valuation is hovering near the average over the past 5 years.

Technical

The UNH stock appears to have a favorable technical setup. It recently broke out of a multi-year consolidation pattern, as shown in the first chart below. It held support once after the breakout and is testing it again. Its MACD and RSI are fairly oversold, and the support coincides with the stock’s rising 200-dma. If support can be held once again, it should provide a solid foundation for a further rally.

The second (weekly) chart below further supports the bullish setup. Although the weekly MACD has turned to a sell signal from an overbought level, the previously mentioned support level also coincides with the stock’s 50-week moving average, and the RSI has dropped below 50. The weekly MACD has turned to a buy signal near this level several times over the past five years. However, we want to see the MACD begin establishing a bottom before getting too confident.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Customer Relationship Summary (Form CRS)