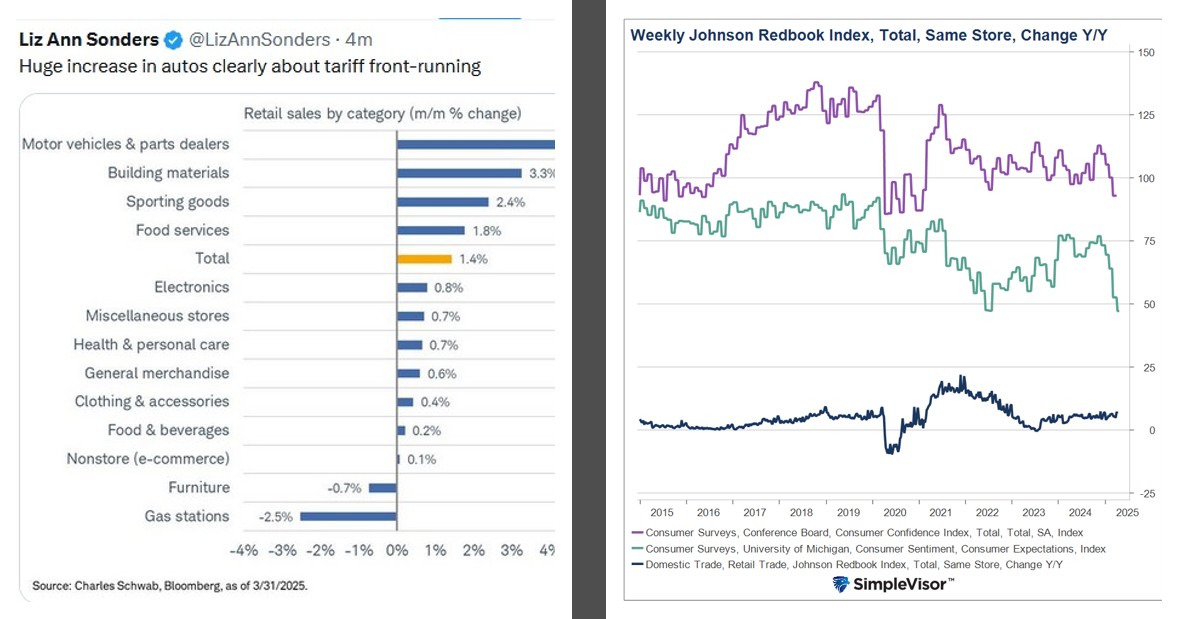

Recent consumer sentiment readings have been horrendous. For instance, the University of Michigan’s latest consumer expectations and the Conference Board’s consumer confidence index are at or near their lowest levels in ten years. However, despite poor sentiment and concerning outlooks, recent consumer spending reports show increased spending. We, and many economists, believe this is a function of consumers frontrunning tariffs. If you think that tariffs will increase the price of goods appreciably, frontrunning, or buying more than you need, or in advance of a need, makes sense.

The latest Johnson Redbook weekly retail sales index argues consumers are frontrunning tariffs despite having historically poor sentiment. This odd divergence can be seen on the graph on the right. The Johnson Redbook index measures year-over-year same-store sales growth for a sample of large U.S. general merchandise retailers, covering about 9,000 stores. Because the index is released weekly, it provides one of the most real-time indicators of consumer spending. The change in spending over the last two weeks is near its peak for the last few years. Further confirming the Johnson Redbook data was Wednesday’s Retail Sales data, showing the largest gain since January 2023. Motor vehicles, a likely candidate for tariff frontrunning, drove the strong spending.

Remember, the surge in spending today, especially that related to front-running tariffs, will result in less spending tomorrow as consumer needs are sated.

What To Watch Today

Earnings

Economy

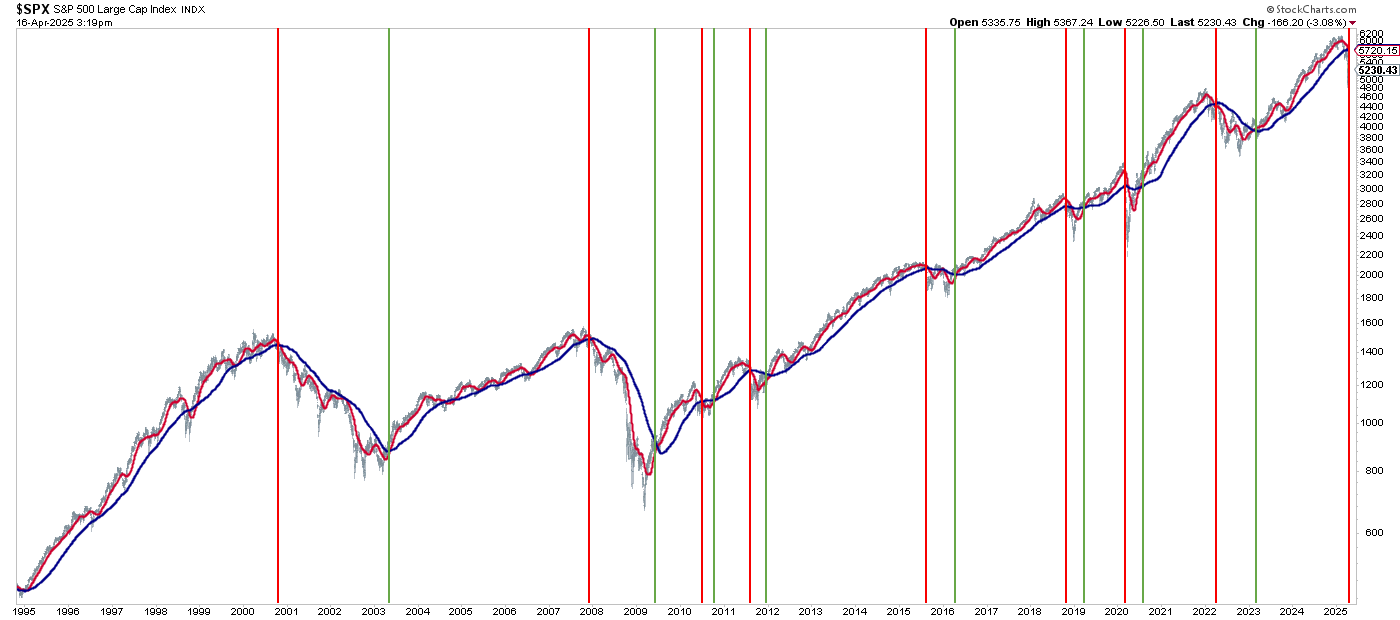

Market Trading Update

In yesterday’s update, we discussed the decline in the dollar relative to the “bear porn” parade of people trying to get clicks and views by promoting the “death of the dollar.” The next “bear porn” headline will be the “death cross” of the S&P 500. It sounds ominous when couched in those terms, but all it means is that the 50-dma has crossed below the 200-dma.

I don’t want to dismiss the importance of that negative crossover, as it does provide significant overhead resistance to market prices during its tenure. But also, as is ALWAYS the case, the crossover will end and markets will begin to rise once again. For investors, the “death cross” is the duration during which such negative price pressure will remain applied to the market. Sometimes, the “death cross” is associated with more significant bear markets; however, it usually tends to occur in shorter-term corrections. I will discuss this in more detail in Monday’s blog post, but the chart below shows the S&P 500 versus historical “death crosses.”

There were three periods when the “death cross” signaled a larger risk-off environment. In 2000, it was the beginning of the Dot.com crash, in 2008, the “Financial Crisis,” and in 2022, as the Fed hiked rates. Other than those three periods, the other “death crosses” triggered near correction period lows.

What is important is to separate out the difference between an “event” driven downturn and a “structural” downturn. 2000, 2008, and 2022 were structural in nature as companies collapsed during the dot.com crisis, banks were on the brink of failure in 2008, and recession risks were elevated with high inflation in 2022. Those structural events cause a significant repricing of earnings and valuations, requiring more time for markets to realign with future expectations. “Event-driven” downturns like the 2012 Eurocrisis, Brexit in 2016, and the Fed’s taper tantrum in 2018 typically evoke short-term market corrections as the markets quickly return their focus to future expectations once the event passes.

While the current downturn and triggering of the “death cross” are certainly worrisome, this “event-driven” downturn will quickly pass as economic policy uncertainty fades. As the Administration begins repealing tariffs and negotiating deals with China, the relief of tariff fears will become supportive of deeply negative market sentiment and oversold conditions.

The point is not to overreact to the surge in “death cross” stories. They are important, but more often than not, they are indicative of near-term market bottoms rather than the beginning of a larger bear market cycle.

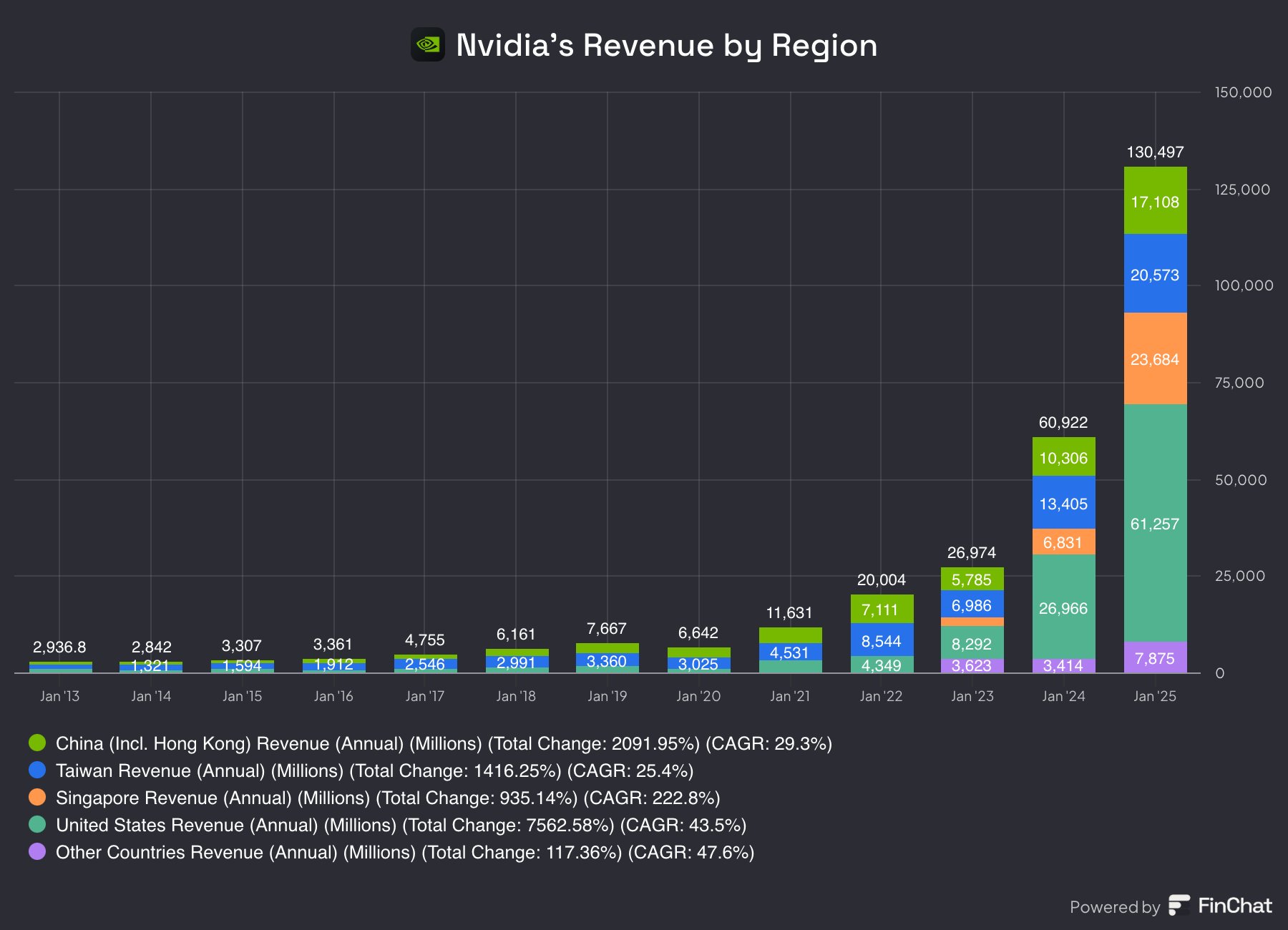

China Trade Restrictions Make NVDA Attractive

Nvidia shares (NVDA) are again under pressure due to tariffs and trade-related restrictions. On Tuesday afternoon, they announced that the US government would indefinitely ban them from selling their H20 chips to China. Consequently, they are taking a substantial charge-off to first-quarter earnings. Per the company:

First quarter results are expected to include up to approximately $5.5 billion of charges associated with H20 products for inventory, purchase commitments, and related reserves.

The graph below shows that 10-15% of Nvidia’s revenue is from China. Losing Chinese revenue, even if temporary, will sting. But is the stock price already pricing in the bad news and not factoring in NVDA’s growth potential?

While we do not know the ultimate resolution regarding tariffs and trade restrictions, we do know NVDA is cheap. The Tweet of the Day at the bottom of this Commentary shows NVDA valuations are at or below their respective 10-year means. NVDA has a forward P/E of 18, below the S&P 500 (21). Furthermore, NVDA is growing its earnings and revenues at many multiples of the market. Accordingly, NVDA has a PEG ratio of 1.15, less than half of the S&P 500. NVDA shares may stay under pressure for the foreseeable future, but they present investors with the rare opportunity to buy a value stock with high growth potential.

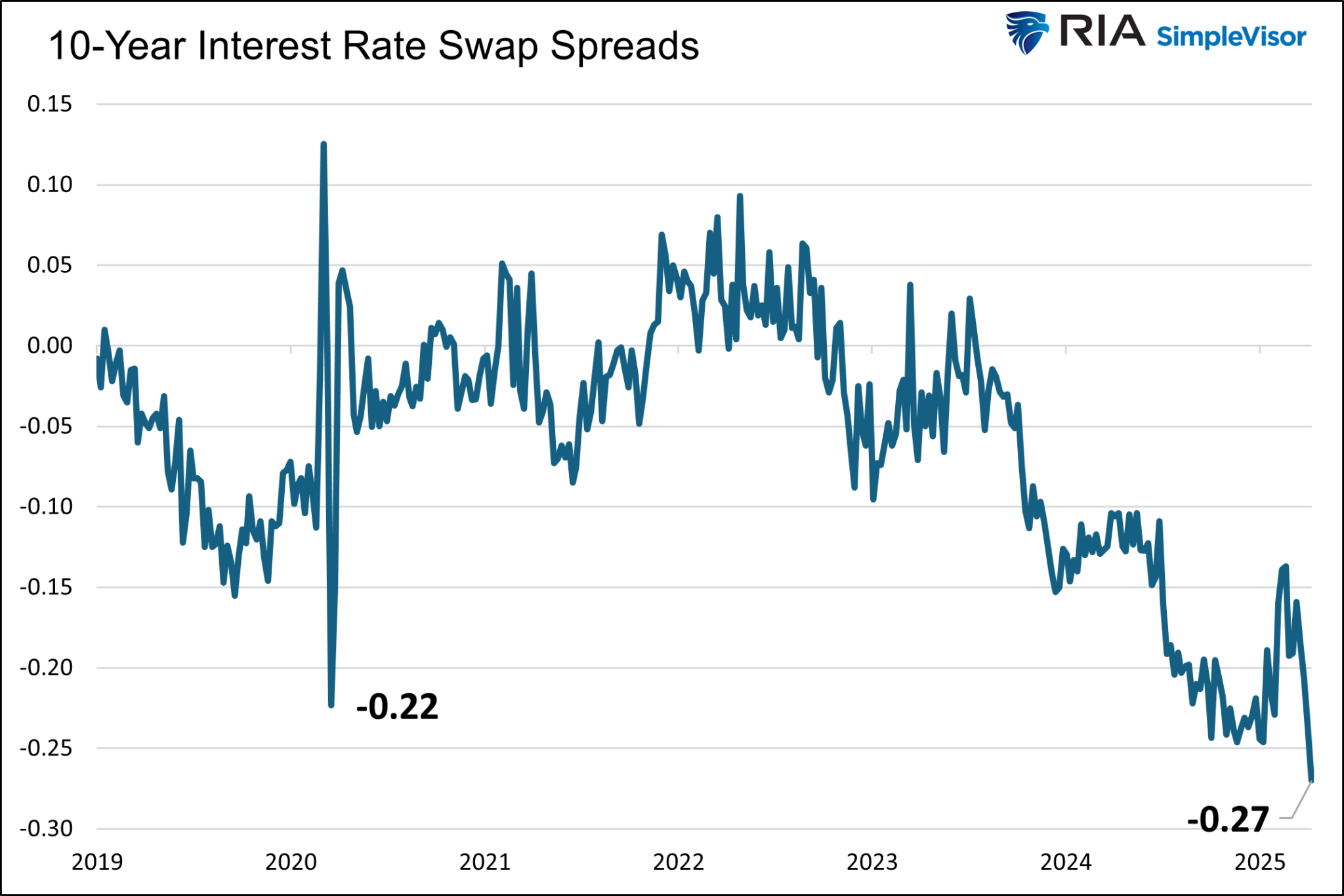

Swaps And Basis Trades Warn Of Mounting Liquidity Problems

Extreme volatility in a highly leveraged financial system inevitably results in liquidity issues. Hence, recent instability is generating mounting signals that liquidity is becoming scarce. This is most evident in the sharp increase in risk-free Treasury yields over the last week. Before the yield surge, liquidity problem warnings appeared in lesser-followed places like Treasury basis trades and interest rate swap spreads.

As we have learned repeatedly, the Fed will take extensive emergency measures if it perceives liquidity problems. Even above their Congressional-mandated objective of managing employment and prices, the Fed’s top priority is preserving the banks. Accordingly, following markets that can provide early notification of liquidity problems will go a long way toward foreshadowing the Fed’s next action and ultimately effectively managing wealth during this volatile period.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.