The latest U.S. Energy Information Agency (EIA) report shows that gasoline demand in the U.S. plummeted to its lowest seasonal level in nearly 25 years. The recent spike in gas prices, along with storms in the Mid-Atlantic and New York City, weighed on demand. But, they do not fully account for the steep decline. The graph below shows gasoline prices (blue) are now near the lowest levels in the last two years. At the same time, crude oil prices are about $15 a barrel above their two-year lows. It’s too early to tell if the demand decline for gasoline is due to weakening economic activity.

The recent plunge in gasoline prices should ease some worries at the Fed about a resurgence in inflation. Energy accounts for 7% of CPI. Gasoline accounts for half of that. Home fuels like heating oil and natural gas comprise the remainder. Gasoline is down over 25% from its early August peak. Heating oil is down 18% from its September peak, and natural gas prices have been relatively flat over the prior two months. BLS energy price data tends to lag real-time data by three months. Therefore, expect CPI energy to decline later in December and January.

What To Watch Today

Earnings

- No notable earnings releases today.

Economy

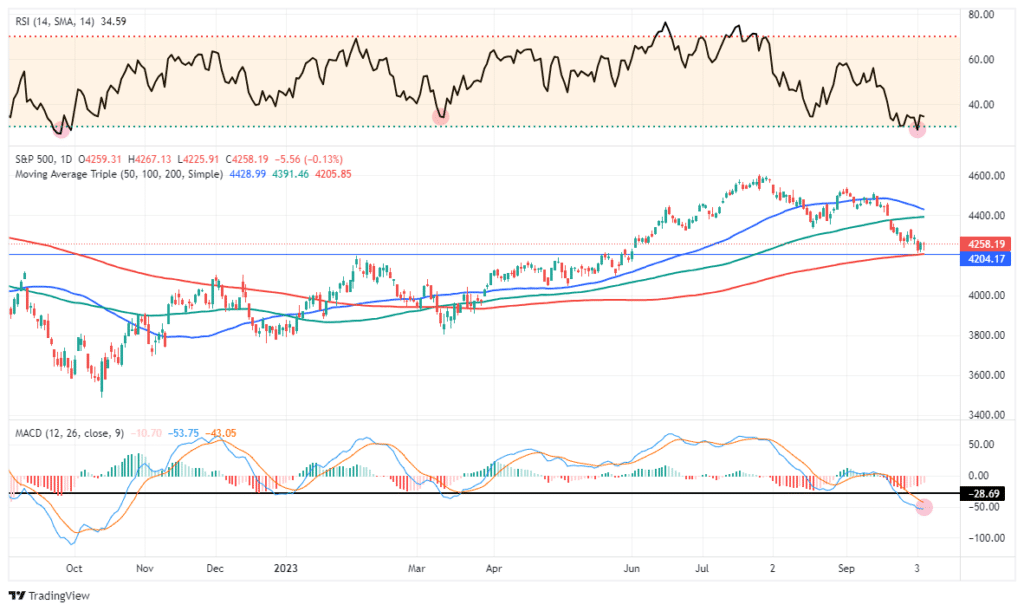

Market Trading Update

Over the last few trading sessions, we continue to see late-day buying to reverse early market weakness. That is a bullish sign, even though market action overall remains weak. Next week should be the last sloppy trading week, as earnings season kicks off next Friday. However, today, all eyes are focused on the employment report. A “hot” employment number will send stocks lower and yields higher on concerns the Fed will need to hike rates again at the end of the month. A “soft” number for stocks and bonds will be bullish, suggesting the Fed is done.

Yes, this is the same game we have played since last year. The reality is that the economy is slowing, and the Fed is likely done hiking rates. They just can’t let the markets know that. So, for now, it remains “Whack-A-Mole” with economic data and the Fed. As noted yesterday, the 200-DMA remains the key support level, and with the markets oversold, a rally is likely. However, the jobs report could detail that this morning, so continue to manage your risk accordingly.

Managing Your Biases In Volatile Markets

Given the recent volatility in the stock and bond markets, the table below is worth reviewing. Often, when markets are volatile, our cognitive biases take control of our decision-making. Bad decisions can be made when this occurs, as our emotions trump solid fundamental or technical analysis. Understanding our biases can prevent irrational trading.

Net Zero Impact on Metals and Greenflation

If the global goal for net zero carbon usage is met, the world must find and produce many more key metals. The graph below shows the estimated amount of three critical metals used for alternative energy sources. Mining and refining of lithium, an essential component of electric vehicle batteries, must grow nearly ten-fold to meet net zero impact goals. Copper production is relatively much closer to where it needs to be in 15 years. However, copper has a significant number of other industrial and commercial uses. As such, it is heavily mined, so finding new sources will come at higher costs. Cobalt production, another critical component in electric vehicles, will need to increase threefold to meet net zero goals. A net zero carbon emission world may have environmental benefits, but it may come at the cost of significant “green-flation.”

Commodity Prices Lead Yields

Given the strong correlation between inflation and bond yields, commodity prices, an important component of CPI, also tend to correlate well with yields. The graph below shows that while the relationship is imperfect, commodity prices tend to lead Treasury yields by 15 months. With year-over-year commodity prices back to their normal 2-3% growth rate, we should expect yields to follow lower, as the graph from LSEG suggests.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 0

2023/10/06