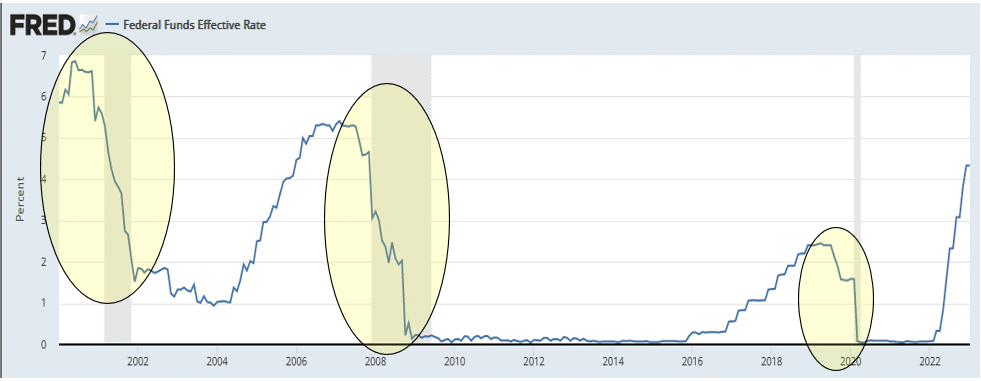

The Fed Funds Futures market implies the Fed will raise the Fed Funds rate to 5%, keep it there for a few months, and then gently lower it by nearly 50bps before year-end. Such is referred to as the goldilocks forecast. Goldilocks portend little volatility in the Fed Funds rate. In economic terms, it means the economy will avoid a recession, inflation will fall quickly, and there will not be meaningful financial instability. Unfortunately, economic growth does not gently cycle higher and lower. As a result, the Fed tends not to adjust Fed Funds up and down gradually. The graph below shows the last three times the Fed cut interest rates, and they do so materially and quickly.

- In 13 months from November 2001 to December 2002, the fed cut rates by over 5%.

- From July 2007 to December 2008, they reduced Fed Funds from 5.25% to 0%.

- Hedge fund instability in late 2019 and the covid crisis resulted in rates plummetting quicker than the prior two instances.

We hope history is wrong, but the reality is that the Fed tends to tighten too much as they underappreciate the lagged effect of their rate hikes. As a result, they must loosen monetary policy rapidly to prevent a sharp economic slowdown and financial market disorder. Goldilocks believers think this time will be different. We hope they are right, but history argues otherwise.

What To Watch Today

Economy

- 8:30 a.m. ET: Change in Nonfarm Payrolls, December (200,000 expected, 263,000 prior)

- 8:30 a.m. ET: Change in Private Payrolls, December (183,000 expected, 221,000 prior)

- 8:30 a.m. ET: Change in Manufacturing Payrolls, December (8,000 expected, 14,000 prior)

- 8:30 a.m. ET: Unemployment Rate, December (3.7% expected, 3.7% prior)

- 8:30 a.m. ET: Average Hourly Earnings, month-over-month, December (0.4% expected, 0.6% prior)

- 8:30 a.m. ET: Average Hourly Earnings, year-over-year, December (5.0% expected, 5.1% prior)

- 8:30 a.m. ET: Average Weekly Hours All Employees, December (34.4 expected, 34.4 prior)

- 8:30 a.m. ET: Labor Force Participation Rate, December (62.2% expected, 62.1% prior)

- 8:30 a.m. ET: Underemployment Rate, December (6.7% prior)

- 10:00 a.m. ET: ISM Services Index, December (55.0 expected, 56.5 prior)

- 10:00 a.m. ET: Factory Orders, November (-1.0% expected, 1.0% prior)

- 10:00 a.m. ET: Factory Orders Excluding Transportation, November (0.8% prior)

- 10:00 a.m. ET: Durable Goods Orders, November Final (-2.1%prior)

- 10:00 a.m. ET: Durables Excluding Transportation, November Final (0.2% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Orders Excluding Aircraft, November Final (0.2% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Shipments Excluding Aircraft, November Final (-0.1% prior)

Earnings

- No notable earnings reports today.

Market Trading Update

After a brief rally on Wednesday, those gains were fully reversed following a strong ADP employment report and a steep drop in jobless claims, which will pressure the Fed to keep hiking rates. As we noted yesterday, the market is currently trading along a rising uptrend from the October lows, but that level is being threatened by yesterday’s decline.

Today is the BLS Employment report and a strong showing will likely send stocks lower. Such will break the market’s recent consolidation range and send lower stocks. A much weaker-than-expected report will send stocks sharply higher toward 3900 to challenge that cluster of moving averages acting as resistance. With today being the end of the week, remain cautious and wait for the market’s reaction to the news. Most likely, traders will not want to hold long positions over the weekend, so trading could be volatile during the entire session.

ADP Jobs Report

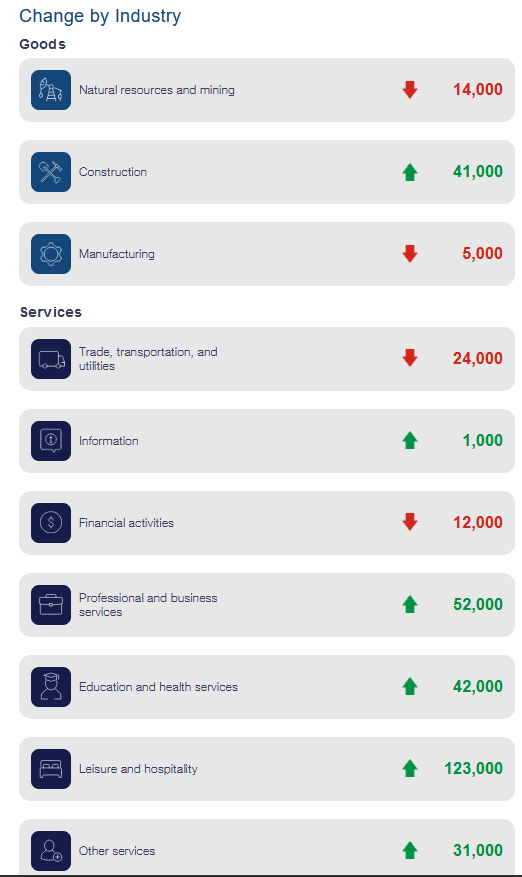

ADP reported a healthy labor market. Per their data, the economy added 235k new jobs, about 100k more than in November and economists’ expectations for December. Almost the entire gain came from the services sector. Small businesses led the way with 195k new jobs. Conversely, large companies shed 150k jobs.

According to ADP, the leisure and hospitality sector added more jobs in the last month than all combined tech layoffs announced. While the headlines fret about job losses at technology firms, they are being offset, albeit with lower-paying jobs.

The following is from Zacks Advisor Insights:

A newish ADP metric is Wage Gains: people who remained in their private-sector jobs last month averaged pay gains of +7.3% — down month over month, but still high — while those who left their jobs and found new employment in the private sector averaged wage growth of +15.2%. This speaks to the inflationary aspects of our labor market, and that wage gains remain remarkably robust.

Key S&P 500 Support Is In Sight

The graph below shows the S&P 500 with its 50 and 200-week moving averages (WMA). The 200 WMA has proven good support for the market over the last thirty years except during the drawdowns of 2000 and 2008. In both cases, a decline below the 200 WMA, followed by a bearish crossover, whereby the 50 WMA falls below the 200 WMA, has proven troublesome. Currently, the S&P 500 is about 125 points above its 200 WMA. Meaningfully breaking below the 200 WMA would be concerning. More troubling would be a bearish crossover. Currently, about 380 points are separating the 50 and 200 WMAs. The gap is closing, but at the current pace, it would take 22 weeks, or almost half a year, for a crossover to occur.

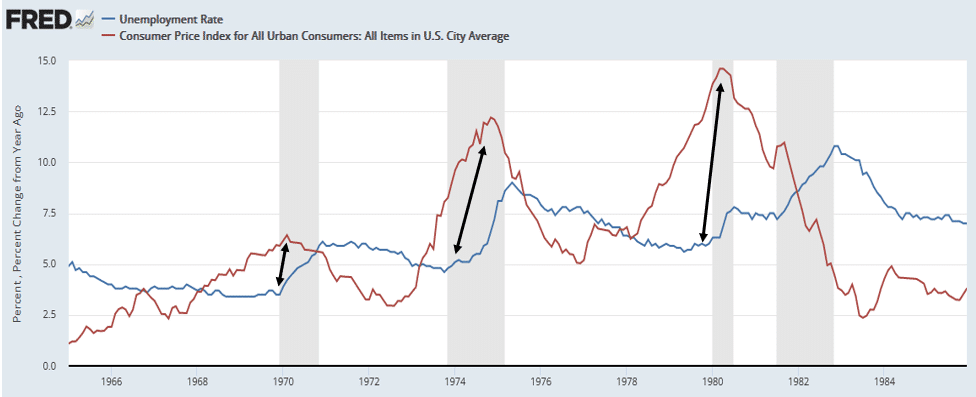

Lessons From The 1970s

The Fed has been outspoken about lessons it has learned from the three bouts of inflation in the 1970s and the tight labor markets’ role in fueling inflation. The graph below highlights that each peak in inflation occurred shortly after the unemployment troughed. Conversely, inflation fell as the unemployment rate rose. As such, with the unemployment rate lingering at 40-year lows, the Fed will likely want to see it rise for a while before declaring victory on its war against inflation.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.