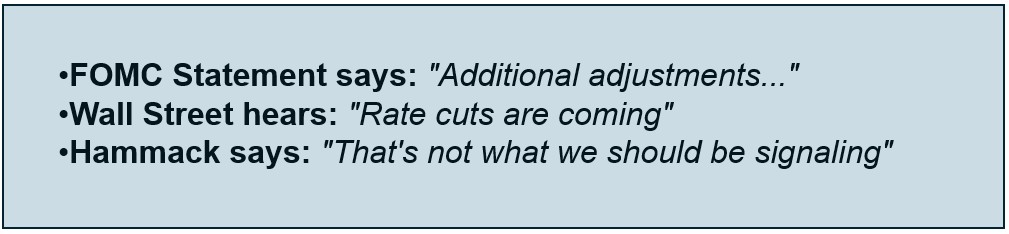

At the April 29th FOMC meeting, Cleveland Fed President Beth Hammack and two others (Logan and Kashkari) dissented. Unlike most dissents historically, the objection wasn’t about whether to change the Fed Funds rate; it was about the language in the FOMC policy statement. She specifically took issue with the wording: ” In considering the extent and timing of additional adjustments to the target range for the federal funds rate.” Hammack felt such language implied that a rate cut(s) is coming.

A week later, Hammack got a chance to explain her dissent via an NPR interview. Her views paint her as more pragmatic than hawkish. She believes the economy is resilient but has concerns about sustained inflation above the Fed’s 2% target. She notes the Fed has “been missing our 2% objective for the past five years.” Importantly, she questions whether the multiple inflationary shocks are “really independent” and wonders whether consumers and businesses are developing a higher-inflation mindset that may be responsible for higher prices.

Despite her portrayal as a hawk, her comments suggest she is much more in the neutral camp. To wit:

I think our statement should have a pretty neutral stance about whether the next move is down or up or just on hold for a really long period of time.

It’s also important to note that Hammack’s views are flexible, and in our opinion, it’s not fair to label her as a hawk or a dove. She fully acknowledges the unknown future economic and inflationary impacts of the recent surge in oil prices, as well as the possibility that prices could fall sharply due to a treaty. She states:

I need to keep an open mind about the next policy move

What To Watch Today

Earnings

Economy

Market Trading Update

The S&P 500 closed Friday at a new all-time high of 7,398.93, up 0.84% and roughly 17.5% off the March lows. But the headline masks a critical divergence. Friday’s Nasdaq surged 1.71% while the Dow gained just 0.02%. The S&P Tech sector rose 3.27% Friday and is up 35% since April 27th. Micron hit an all-time high(+25% in one week). AMD gained 15%. Meanwhile, Thursday’s internals told a different story: decliners outnumbered advancers 1.8-to-1, with only 18 new highs against 11 new lows. This week’s rally was overwhelmingly a semiconductor and AI chase, not a broad market improvement. The April jobs beat (115K vs. 65K expected) provided cover, but the money is flowing into one trade.

The 14-day RSI has surged to 74.58, deep into overbought territory and the highest since January’s peak. RSI above 70 has preceded every 2%+ pullback since June 2024. Investtech flagged the index as overbought after a break above the upper parallel channel, a condition in which past false breakouts have occurred. The index trades 7.2% above the 50-DMA (~6,863) and 8.7% above the 200-DMA (~6,753). Deviations of this magnitude historically revert within 2–4 weeks, producing pullbacks of 3–5%. The MACD is at the most extended reading of the year. Every indicator says “buy,” and that unanimity is itself a contrarian warning. As the old saying goes: “When no one is left to buy, who provides the next bid?”

The risk of corrective action is elevated. Semiconductors are flashing exhaustion on diminishing volume, the hallmark of a trade running out of fuel. Western Digital’s 8% intraday collapse this week was an early signal of what happens when the most extended names gap down. The more probable near-term outcome is not a crash but a rotation: capital moving out of exhausted semi-leaders into lagging sectors. If orderly, the S&P churns sideways while the 50-DMA catches up. If disorderly, potentially triggered by an Iran escalation or hot CPI, a 3–5% pullback to 7000, or the 50-DMA below that, comes fast.

Bottom line: This is not a market to initiate new longs at the highs. The trend remains bullish, but trends that move this far, this fast, always revert to the mean. The question is how, not if. Tighten stops, take profits in extended semi names, and build a buy list for the pullback. Patience pays. Trade accordingly.

The Week Ahead

Topping the list of economic releases is the BLS inflation update. CPI, for release on Tuesday, is expected to show a relatively high 0.6% increase in inflation but below last month’s +0.9%. The core figure, excluding food and gas, is expected to increase by 0.3%, a tenth of a percentage point above last month’s figure. PPI is expected to increase by 0.4% and 0.2% for headline and core producer prices, respectively. While inflation estimates are high, the elevated prices of oil and related items, which are driving the price increases, are currently viewed by the Fed and Wall Street as temporary. Thus, the CPI and PPI data are not likely to impact markets unless they are well above estimates.

Retail Sales for April will be released on Thursday. After rising sharply in March by 1.7%, analysts see a more subdued gain of 0.4%. Bear in mind, this is not inflation-adjusted, so higher oil prices are filtering into the data.

The earnings calendar will be relatively quiet this week, with investors’ eyes turning to Nvidia’s release on May 20.

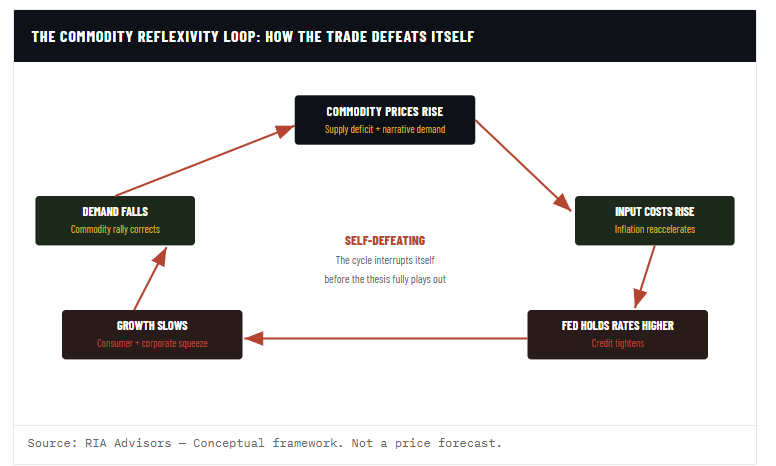

Commodity Supercycle: The Enemy Of The Bull Thesis (Part 1)

The commodity supercycle thesis is everywhere right now. Bank of America’s Michael Hartnett, one of the most widely read strategists on Wall Street, recently declared “commodities the biggest trade of the next five years,” anchoring the call on deglobalization, chronic capital underinvestment, and a world drifting away from dollar dominance. As is often the case, the narrative is extremely compelling. However, it’s also internally contradictory in ways that most investors aren’t stopping to examine.

After three decades of managing money, I have learned to be THE most skeptical of the trades that feel the most inevitable. That skepticism isn’t contrarianism for its own sake, but rather the recognition that when a thesis achieves consensus, the crowd has usually already priced the easy part of the move, and the hard part is what comes next. The commodity supercycle argument has real structural legs. But it also carries a reflexivity problem, a dollar mechanics problem, and a catastrophist assumption problem that, taken together, make the clean “go long commodities” conclusion far messier than the headline suggests.

Let’s work through each one carefully, and as always, with the data.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.