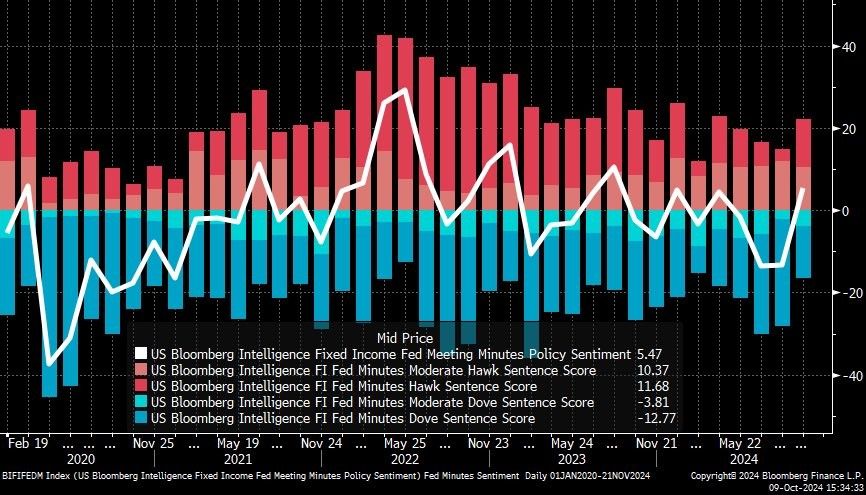

The graph below, courtesy of Bloomberg, shows their Intelligence data rates the latest Fed meeting minutes as the most hawkish since April. Qualifying the minutes as hawkish is pretty ironic, considering the Fed’s 50bps rate cut three weeks ago was the most dovish action they have taken in a few years.

Is it possible for the dovish Fed to be hawkish simultaneously? Based on the recent FOMC minutes, pushback appears to be against cutting rates by 50bps. While all but one Fed member voted for the increase, many hesitated. Accordingly, in getting the first cut of 50bps, Powell may have given leverage to others arguing for a slower, wait-and-see approach. The following quotes from the minutes show the hawkish and dovish views on the board.

Some participants emphasized that reducing policy restraint too late or too little could risk unduly weakening economic activity and employment.

Several participants remarked that reducing policy restraint too soon or too much could risk a stalling or a reversal of the progress on inflation.

Some participants noted that uncertainties concerning the level of the longer-term neutral rate of interest complicated the assessment of the degree of restrictiveness of policy and, in their view, made it appropriate to reduce policy restraint gradually

Given the co-existence of hawkish and dovish views, we should prepare for more stock and bond market volatility around economic data and Fed speeches.

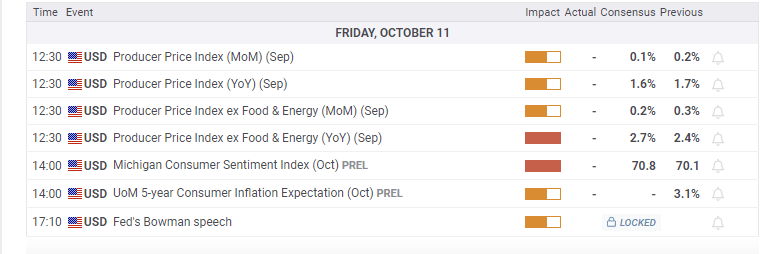

What To Watch Today

Earnings

Economy

Market Trading Update

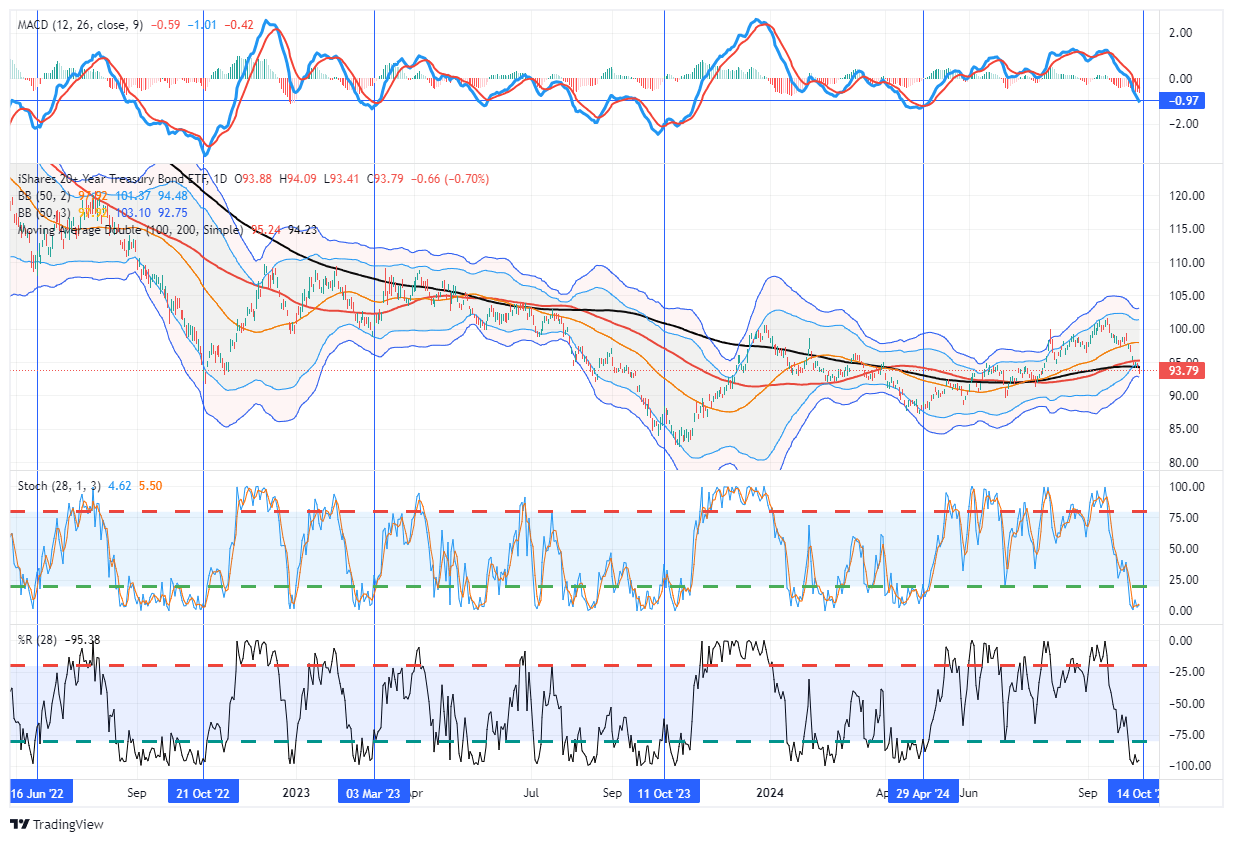

Yesterday, we discussed how the market remains contained in a bullish rising wedge pattern, which remains the case heading into this morning’s trade. However, the once notable move yesterday was in bonds following the latest CPI report. Several weeks ago, we noted that investors should NOT buy bonds given their extreme overbought condition heading into the September Fed meeting. Since that meeting, the reversal has sent bonds into extreme oversold conditions.

As shown, bonds are trading well into 3-standard deviations in oversold territory, and their relative strength and momentum are becoming very negative. As noted by the vertical lines, previous similar conditions have provided decent bond trading opportunities. Once election uncertainty is behind us, such may well be the case heading into year-end. There is still additional downside risk to bonds between now and the end of the month. However, most of the selling is likely complete.

From a trading perspective, there is a decent opportunity for adding bonds to portfolios. If you are a long-term holder of bonds, with rates back to 4% on a 10-year paper, the opportunity to add bonds to portfolios is also compelling.

CPI

The BLS CPI report was a little hotter than expected, with the monthly and annual headline and core numbers coming in at a tenth of a percent higher than expected. However, the year-over-year rate is down to 2.4%, which aligns with pre-pandemic inflation rates, as shown below.

Transportation (auto insurance) and health care drove the rate higher. Moreover, rents remain firm despite real-world evidence that they are flat to declining. However, an alternate measure of underlying core inflation, services less rent, healthcare, and transportation, showed zero monthly inflation. The CPI number has something for the inflation bulls and bears.

Our take: Inflation continues to decline, and while the month-to-month numbers do not show a perfect trend lower, the macroeconomic dynamics impacting inflation will likely keep inflation near current rates or lower. If the economy slows, inflation is likely to follow.

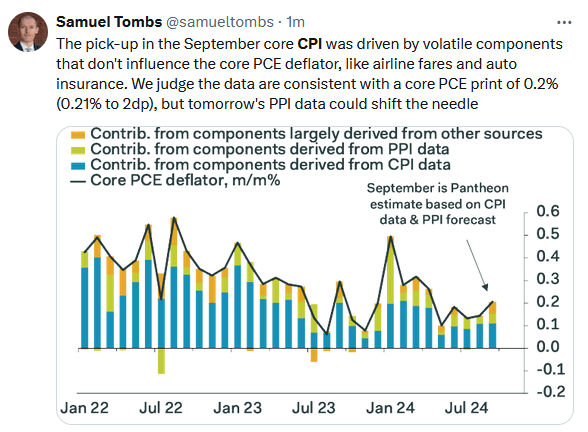

The Tweet of the Day below shows that despite the higher-than-expected CPI, the Core PCE inflation data, the Fed’s preferred inflation measure, will likely come in at 0.2%.

Hurricanes Helene and Milton may result in volatility in CPI and other economic data over the next few months.

Jobless Claims

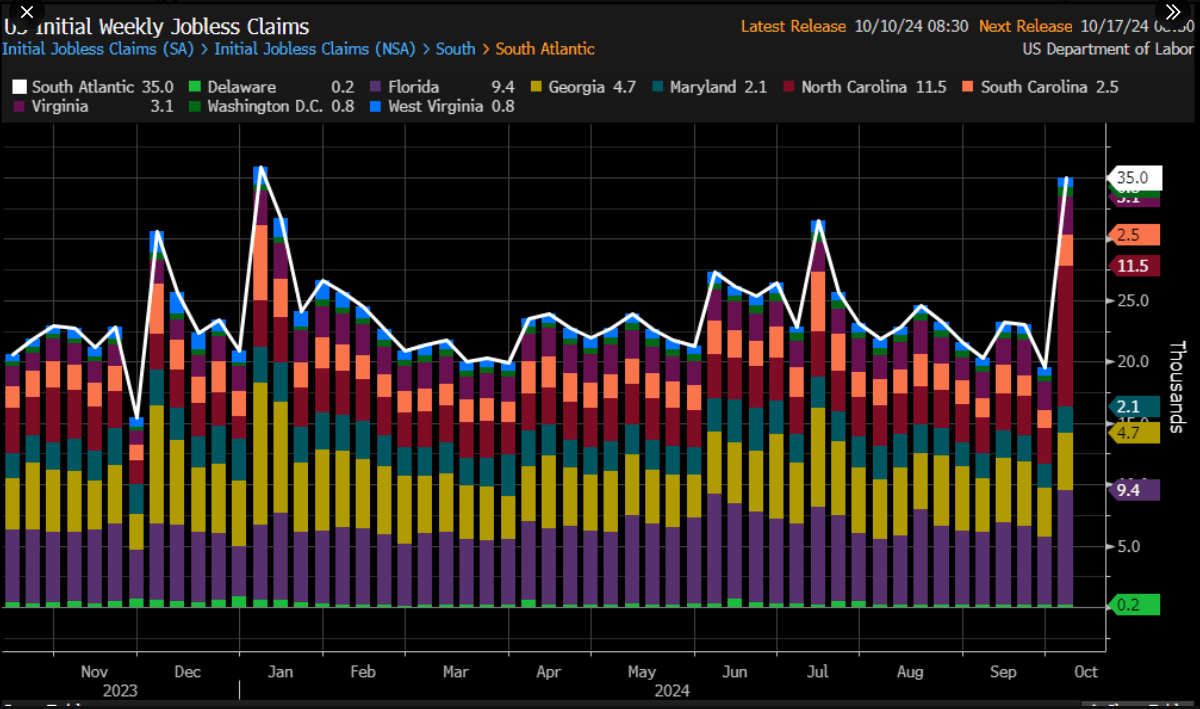

Despite the higher CPI data, the bond market had a muted reaction. It may have been because the BLS Jobless Claims data was higher than expected. The number of initial claims was 258k versus 225k last week, and the expectations were that it would rise by 5k to 230k. Measuring jobless claims this week and for the next couple of months will be complicated by the hurricanes. That said, the graph below shows that the South Atlantic region, including the areas hardest hit by Hurricane Helene, only saw a 15k increase in jobless claims. That number will likely increase over time. However, excluding the 15k, the number of initial claims was still about 18k more than last week.

Jobless claims can be whippy, so don’t read much into the increase, but as always, keep an eye to see if the number, excluding the hurricane impacts, continues higher.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 0

2024/10/11