The hot January CPI report bolsters the Fed’s view that inflation will not fall as rapidly as they prefer. Despite what may appear to be a slight setback, the downward trend remains intact. Year-over-year CPI is down seven consecutive months to the lowest level since October 2021. While the trend is assuring, January’s monthly data were not. Both the headline and core (excluding food and energy) were +.1% hotter than expectations. The question facing investors is what Powell thinks about the hot inflation data.

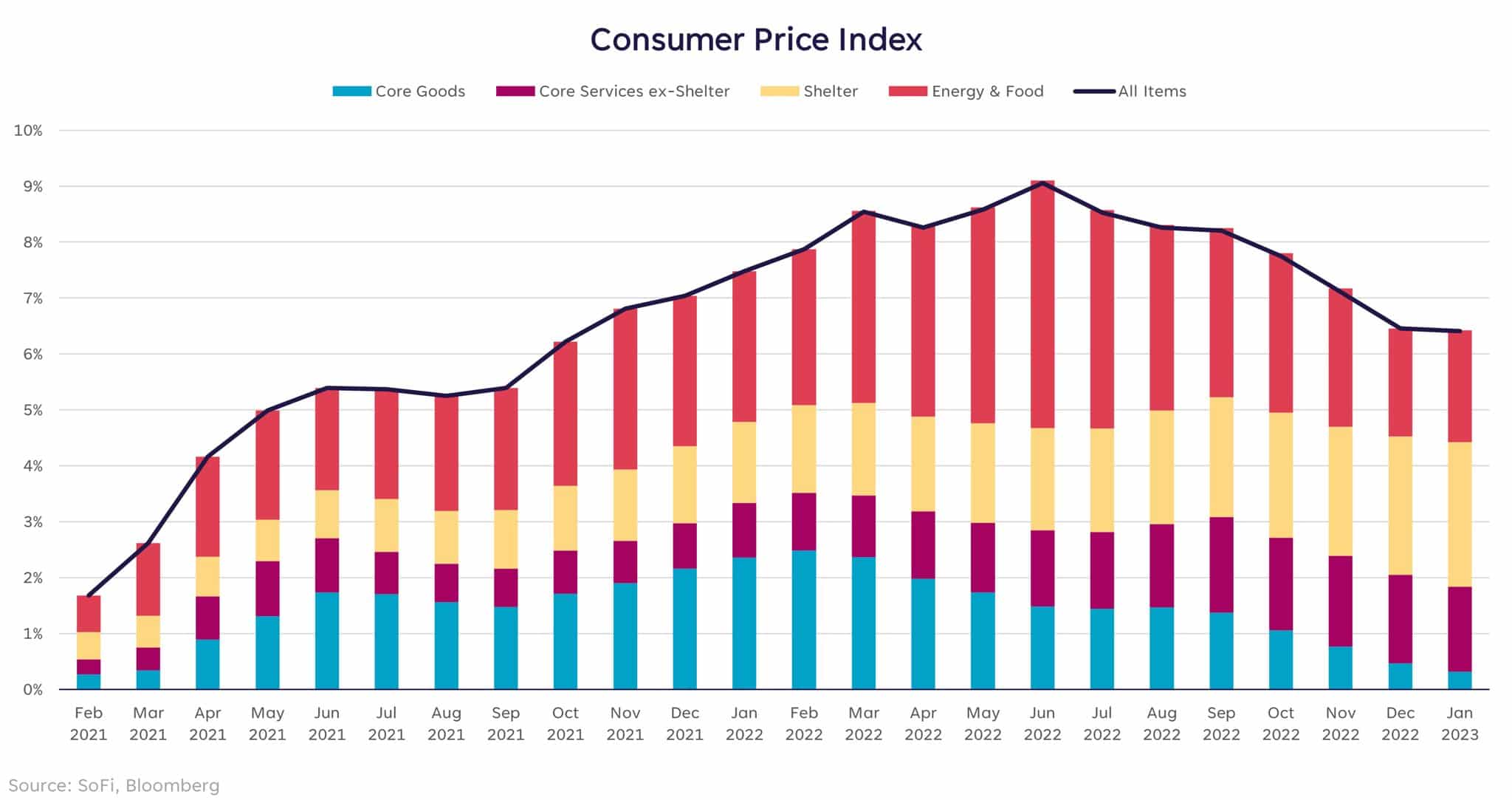

Powell has made it clear he puts a lot of weight on core services, excluding shelter prices, to guide rate decisions. That gauge was up by .29% in January but below the 0.37% print in December. The decline helps explain why the initial market reaction to the hotter inflation data was positive. The broad theme within the report is that the prices of goods continue to fall while service prices are still rising. CPI commodities less food and energy now stands at +1.4% annually, while services less food and energy rose last month to +7.2% annually. The graph below from SoFi shows that core services (purple and yellow) are increasingly taking a more significant share of inflation. At the same time, energy, food, and core goods contribute less. The tug-of-war between goods and services may likely determine monetary policy over the coming year.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Feb. 10 (7.4% prior)

- 8:30 a.m. ET: Empire Manufacturing, February (-18.0 expected, -32.9 prior)

- 8:30 a.m. ET: Retail Sales Advance, month-over-month, January (2.0% expected,-1.1% prior)

- 8:30 a.m. ET: Retail Sales Excluding Autos, month-over-month, January (0.9% expected, -1.1% prior)

- 9:15 a.m. ET: Industrial Production, month-over-month, January (0.5% expected, -0.7% prior)

- 9:15 a.m. ET: Capacity Utilization, January (79.1% expected, 78.8% prior)

- 9:15 a.m. ET: Manufacturing (SIC) Production, January (0.8% expected, -1.3% prior)

- 10:00 a.m. ET: Business Inventories; December (0.3% expected, 0.4% prior)

- 10:00 a.m. ET: NAHB Housing Market Index, February (37 expected, 35 prior)

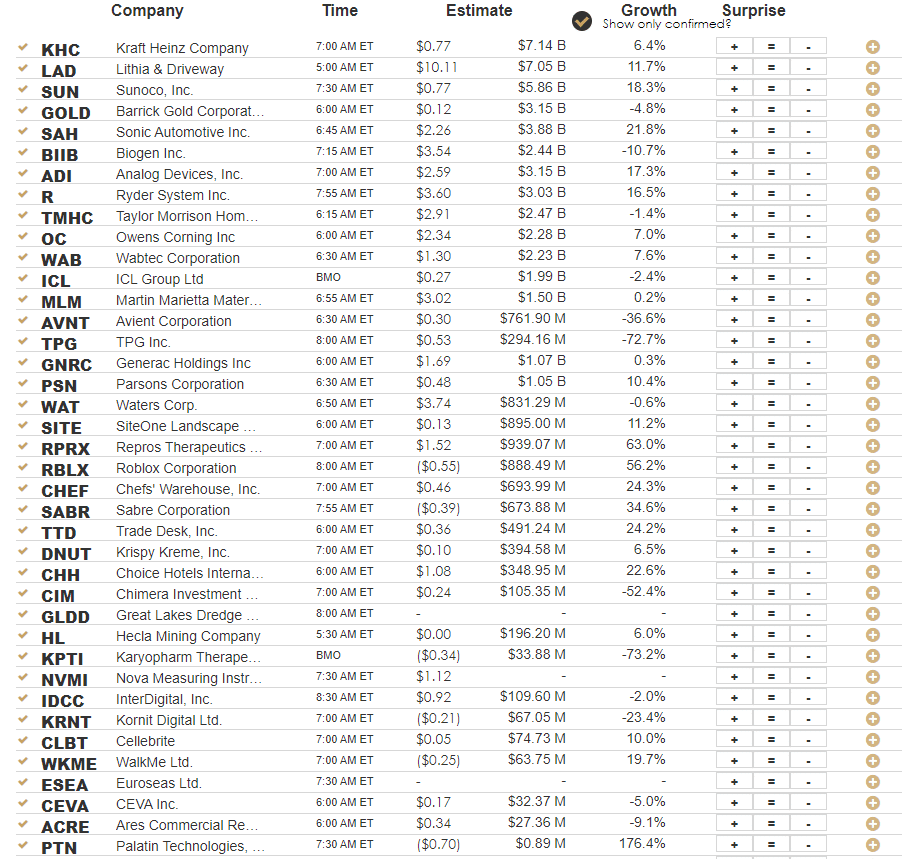

Earnings

Market Trading Update

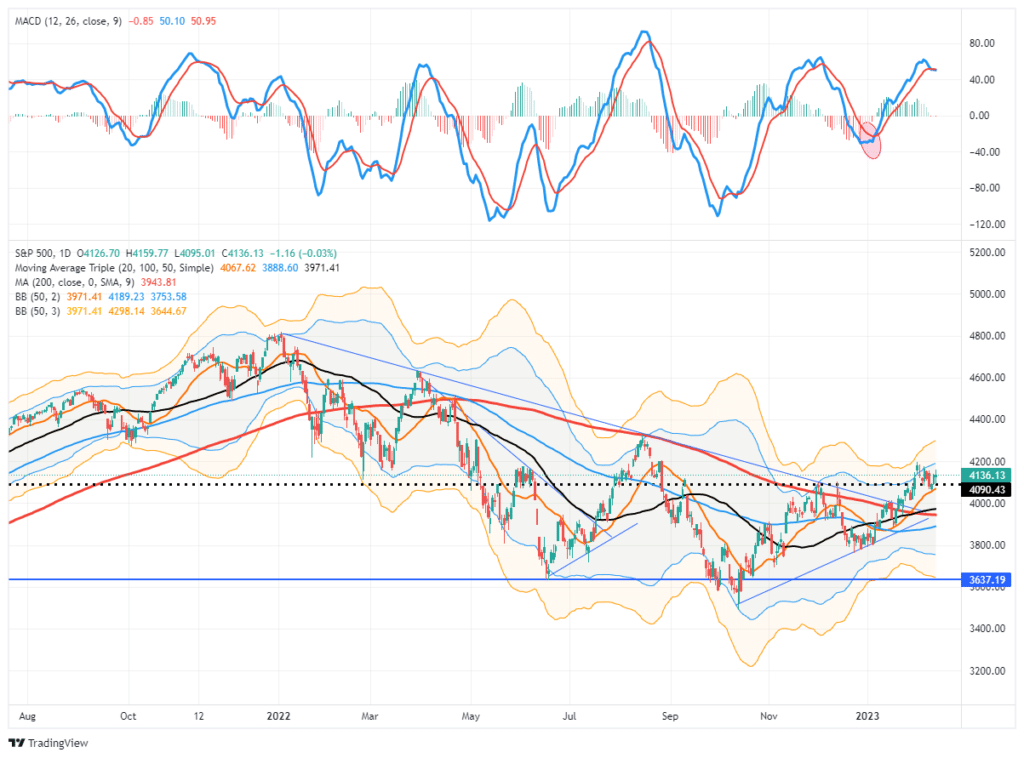

The market sold off on the hot inflation print yesterday but recovered during the day as bullish buyers continue to chase asset prices. Despite the fact this number continues to give the Fed a reason to tighten monetary policy further, the hope remains that rate cuts are coming as soon as this summer.

Regardless, the market has triggered a short-term sell signal, and, as stated yesterday, the upside to the market near term is likely limited. We suggest being patient here as the market consolidates and reduces some excesses. There is a lot of support at the 20-DMA, with a significant cluster of support at the 50- and 200-DMAs just below.

The rising trend line from the October lows remains the key alert point. If that is broken, the bears will have regained control of the market, and lower prices will result. For now, however, the bulls remain in charge, and the bullish trend remains “our friend”. Take some profits and reduce risk until we get the next buy signal.

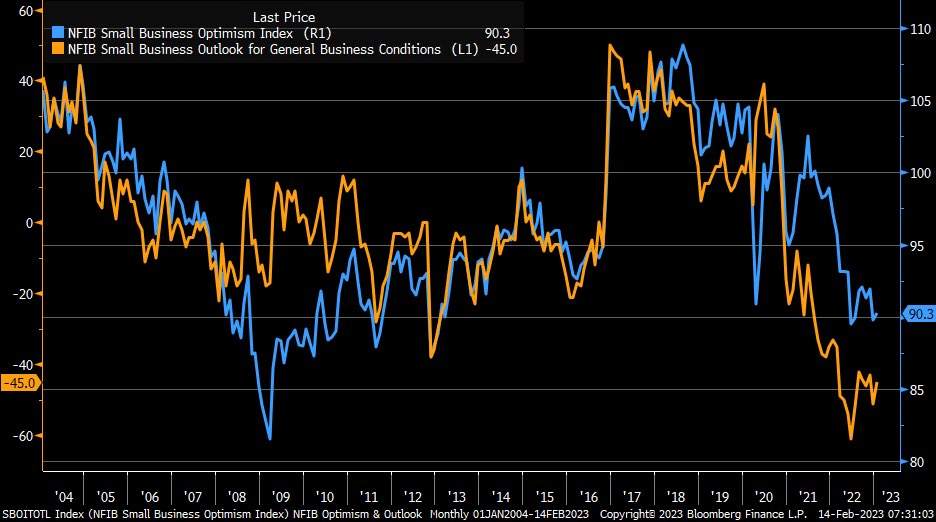

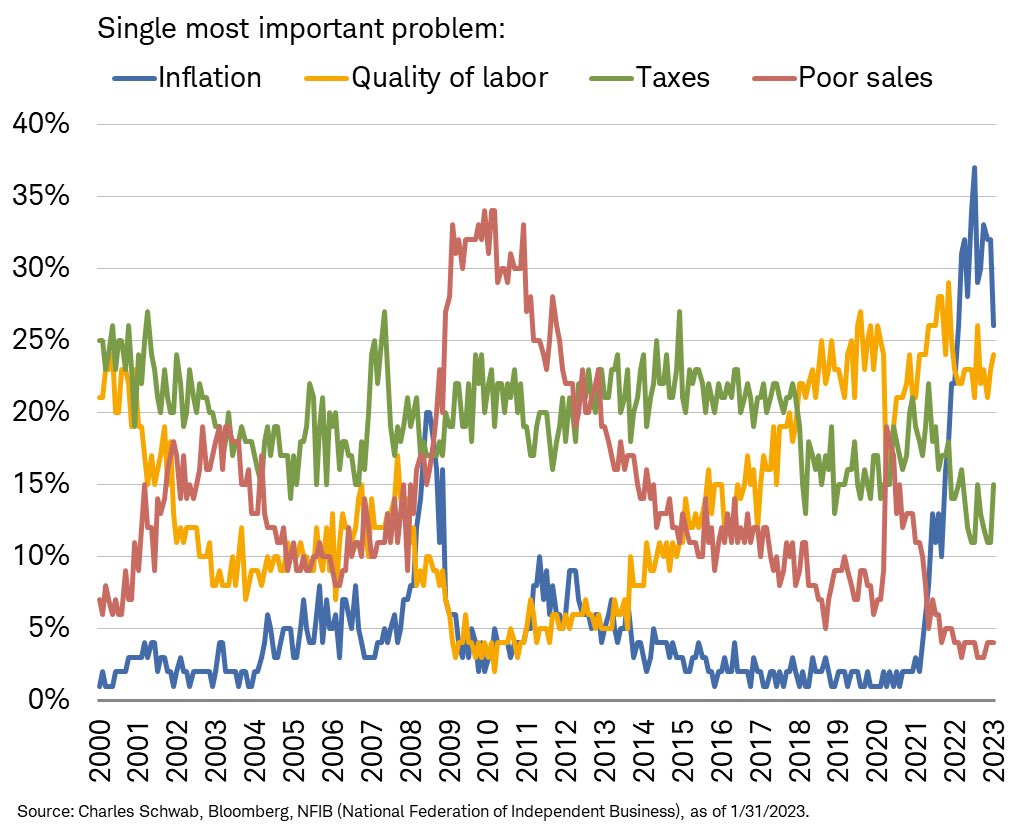

Small Businesses Are Still Pessimistic

The NFIB small business survey continues to paint a grim picture of the economy, as seen by small business owners. Per NFIB Chief Economist Bill Dunkelberg:

“Overall, small business owners are not optimistic about 2023 as sales and business conditions are expected to deteriorate”

“Owners are managing several economic uncertainties and persistent inflation and they continue to make business and operational changes to compensate.”

The first graph shows that the current conditions index (Optimism Index) remains slightly below the pandemic lows but above levels in late 2008 and early 2009. More concerning, the outlook, while off the lows, is still below levels in 2008/2009. Filling job openings and inflation are the two biggest problems facing small businesses. About 45% of those surveyed find job openings are still hard to fill. That is below the peak of 51% last year but above any level seen before the pandemic. The good news is that the number of firms raising prices fell to 42%. While still high, it is the lowest since May 2021.

Inflation- Another Risk Undermining the Fed Pause

January’s hot inflation data and stubbornness of service prices to decline affirms the Fed’s hawkish stance. As they consistently remind us, they will get Fed Funds to at least 5% and keep them there for the year. A week ago, Powell stated the following:

“Our message was this process is likely to take quite a bit of time. It’s not going to be smooth,” he said. “It’s probably going to be bumpy, and we think that we’re going to need to do further rate increases, as we said, and we think that we will need to hold policy at a restrictive level for a period of time.”

While the bond markets are starting to price in such a scenario, the stock market seems intent on a pivot. In The Correction May Have Started, Lance Roberts provides a few other risks for investors.

Over the next several months, some risks could undermine the bullish support of a “Fed Pause” and a “soft-landing.”

- If the market advance continues and the economy avoids recession, there is no need for the Fed to reduce rates.

- More importantly, there is also no reason for the Fed to stop reducing liquidity via its balance sheet.

- Also, a soft-landing scenario gives Congress no reason to provide fiscal support providing no boost to the money supply.

While the bulls remain in control of the market, we must trade it accordingly. However, the risk to the bullish view remains a challenge for the rest of this year.

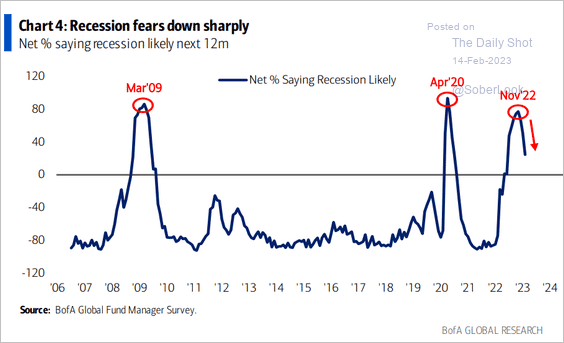

Recession Fears Abating

The no recession – soft landing outlook is growing in popularity. As shown in the Daily Shot/ BofA graph below, the percentage of institutional investors thinking that a recession is coming this year is falling. Not surprisingly, the stock market has been rallying since recession fears peaked. Many gauges of sentiment, both economic and markets, tend to rise and fall with markets.

Looking back at the recession of 2008/09, we find that recession fears abated in the same month the market bottomed. However, look back at 2007 and early 2008. The writing was on the wall that a recession was almost inevitable, yet no one saw a recession coming.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.