As sentiment shifts from a Fed rate-cutting forecast to one that now sees a chance of a rate increase, a potentially powerful short squeeze setup might be emerging in the Treasury market. Heading into the Iran conflict, speculative short positions in TLT and Treasury futures were near historically elevated levels, reflecting a broad consensus that yields would increase. Then the conflict broke out, and oil prices surged. Rather than following the traditional flight-to-safety script of falling yields and rising bond prices, yields increased as inflation fears took hold in the bond market.

Higher yields, including nearly 5% on 30-year bonds, could set up a bond short squeeze. When or if higher oil prices lead to economic weakness, or if the Iran conflict de-escalates faster than expected, the Fed could quickly shift back toward a dovish stance more aggressively than the market anticipates. Further, the unwinding of the oil premium, combined with weaker economic growth and buying by yield seekers, could force a rapid unwinding of elevated short positions and drive a short-squeeze rally in Treasury prices. Investors who have been shorting bonds for the past month have been rewarded, but the bigger the short base, the more likely a meaningful reversal.

As we wrote in last week’s Commentary, the Donald Kohn framework suggests that rate cuts are more appropriate than rate hikes in the context of a supply-driven oil shock. If the Fed and the market come around to that perspective, a bond market short squeeze may catch many investors by surprise.

What To Watch Today

Earnings

- No earnings releases today

Economy

Market Trading Update

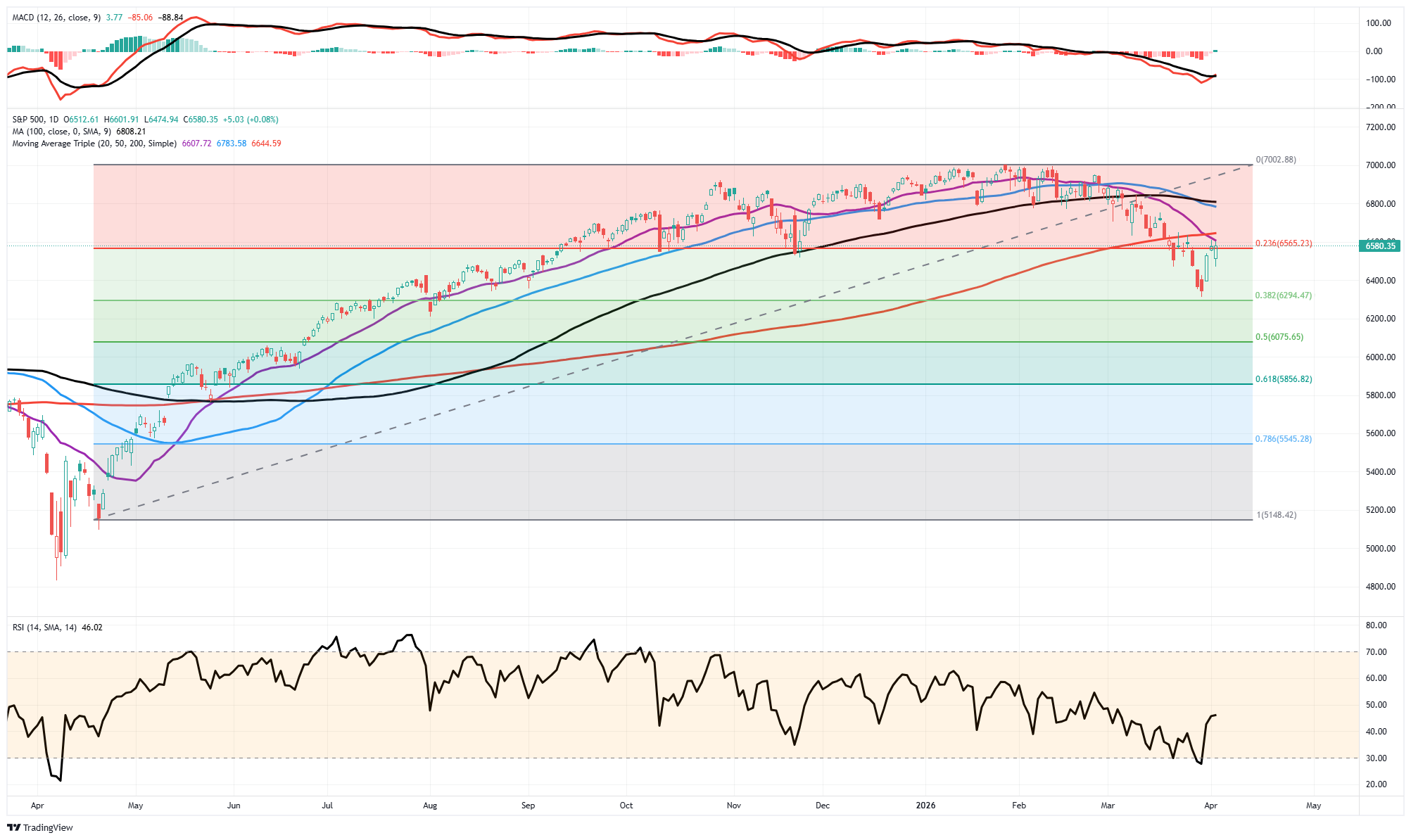

The S&P 500 closed Thursday at 6,566 ahead of the Good Friday holiday, snapping a brutal five-week losing streak with a gain of roughly 3% on the week. Tuesday’s +2.9% surge—the best session since May—was ignited by reports that Iran’s President is open to ending the war, combined with Trump’s announcement of “productive talks.” March still ended down over 5%, but the bounce off 6,300 produced a 4.2% rally from trough to Thursday’s close. The question heading into Q2 is whether this bounce has legs or is simply another dead-cat rally in a larger corrective phase.

As shown, the current rally is pushing into resistance at the 20-day moving average, which has crossed below the 200-day moving average. Notably, momentum has triggered a short-term buy signal, and relative strength is improving from very oversold levels. However, the big question is whether investors can retake the current resistance levels and push markets higher into next week, but the data suggests caution.

The internals tell us this bounce is real but fragile. As of Wednesday’s close, only 27.6% of S&P 500 constituents traded above their 50-day moving average, a percentile reading of just 12, meaning breadth has been this weak only 12% of the time. That is an extraordinarily narrow rally. Meanwhile, 49.2% remain above their 200-DMA (25th percentile), below average but notably above the sub-30% washout levels of the 2022 bear market. The RSI has recovered to 45.7 from the oversold low-30s in late March, and the McClellan Oscillator has turned positive after deeply negative readings. Both are constructive, but the percentage of stocks above the 50-DMA needs to expand well above 50% before we can call this anything more than a “reflexive bounce within a downtrend.“

So, is the market oversold enough for a sustained move higher? The short answer: the conditions are present for a tradeable rally, not a durable bottom. Seasonality helps as April is historically the second-best month for the S&P 500 (+1.4% avg per the Stock Trader’s Almanac), and earnings season kicks off with FactSet consensus at 13% YoY EPS growth. However, the macro overlay remains hostile: Brent near $117, the Fed has priced out cuts entirely (Macquarie expects a hike in 1H27, and the 10-year yield sits near 4.45%. The index closed Thursday still 1.2% below its 200-DMA (~6,642), and until price reclaims that level, the primary trend remains down. Investors who missed the bounce should not chase here.

Bottom line: If you are fully invested, this bounce is an opportunity to add hedges, not remove them. Consider put spreads on SPY or collar strategies on concentrated positions. If you’ve been building the shopping list we recommended, this isn’t the entry; that was the 6,300 level two weeks ago. The next entry comes on either a successful retest of March lows or a decisive close above the 200-DMA with breadth confirmation (50-DMA participation above 50%). Warren Buffett said it best Tuesday: he’d buy more Apple, “but not in this market.”

We agree. Defense over offense. Trade accordingly.

The Week Ahead

In the prelude week to corporate earnings, there will be a decent amount of data to digest. The likely headliners will be CPI on Friday and PCE on Thursday. Bear in mind, PCE covers the February time frame, so it will not include the impact of higher oil prices. CPI is expected to rise by 0.8% in March; however, Core CPI is expected to rise by only 0.2%. Thus, higher energy prices will exert themselves in this report. As we have discussed, the Fed primarily focuses on Core inflation; thus, the potentially high headline CPI should not be a surprise to the stock or bond markets. Further, higher yields and lower stock prices already reflect the increase in oil prices.

The FOMC minutes on Wednesday may shed some light on how the Fed balances the inflationary impact of the Iranian conflict with the negative effect on the economy. The market will focus on how they speak to both risks and the balance of those conversations. Currently, as shown below, the market is pricing in a mere 3bps of rate cuts through November.

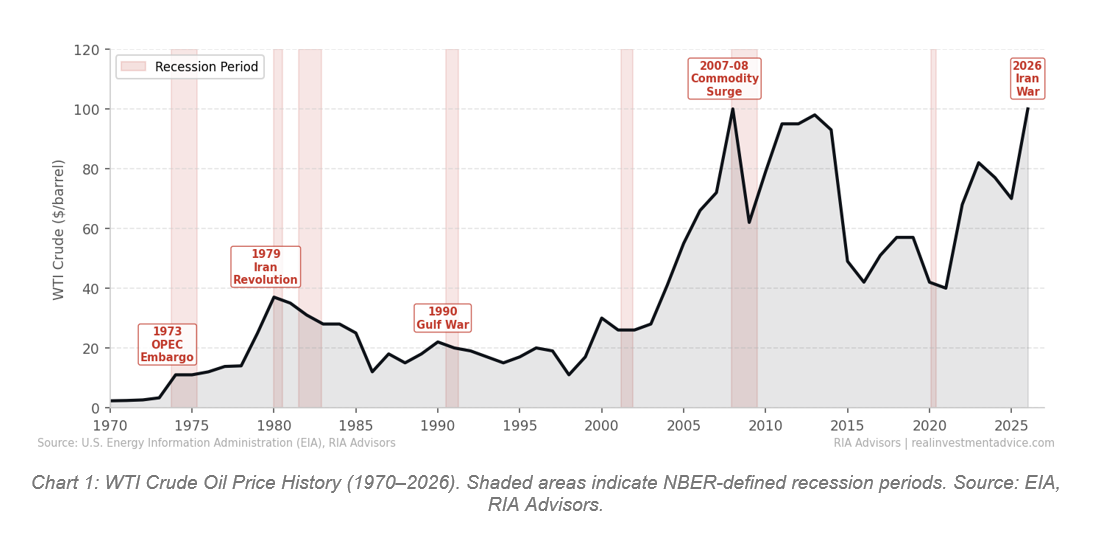

Oil Shocks & Recessionary Outcomes

After more than three decades of watching oil markets upend economies, one pattern keeps repeating: investors learn the wrong lessons from the last shock. The 1973 OPEC embargo taught us that geopolitical disruptions are temporary. That lesson then got everyone killed, financially speaking, in 1979. The 2003 Iraq War produced only a mild oil bump and no recession, so traders got comfortable. Then 2008 happened. Today, with Brent crude having spiked over 60% since U.S. and Israeli strikes on Iran began in late February, the same dangerous reasoning is circulating again. That narrative is that this “event” is manageable and will resolve quickly. If that is the case, then the economy will absorb it.

That may indeed be the case. However, the conditions that determine whether an oil shock becomes a full recession are specific, quantifiable, and worth examining with clear eyes. That is what this analysis does.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.