We have read commentary equating the sharp increase in money market assets with cash on the sidelines waiting to be redeployed into the stock market. Therefore, the analysts imply the extra cash sitting in money market funds is fodder for a stock rally. During the 2008/2009 market swoon, money market assets rose sharply and peaked as stocks were troughing. Similarly, cash in money markets spiked at the pandemic’s start and then eased commensurate with stocks surging in value. If the recent surge of cash into money market assets is a placeholder for investors to buy stocks, we may have a strong rally ahead.

Unfortunately, the surge in cash holdings does not appear to be investment dollars waiting to buy stocks. The graph below shows an approximate $500 billion increase in money market assets since January 2022. However, the St. Louis Federal Reserve estimates that commercial deposits have shrunk by a very similar amount. Unlike early 2009 and May 2020, the surge in cash holdings is not coming from investors parking cash. Instead, the large majority is from non-investing depositors chasing higher yields offered at money market funds and, to a lesser degree, avoiding risks associated with banking deposits.

What To Watch Today

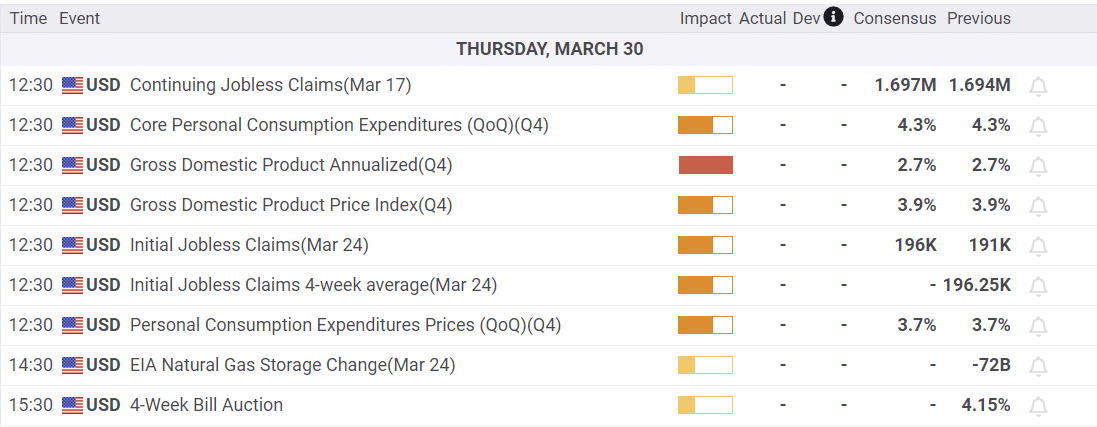

Economy

Earnings

- No notable releases today

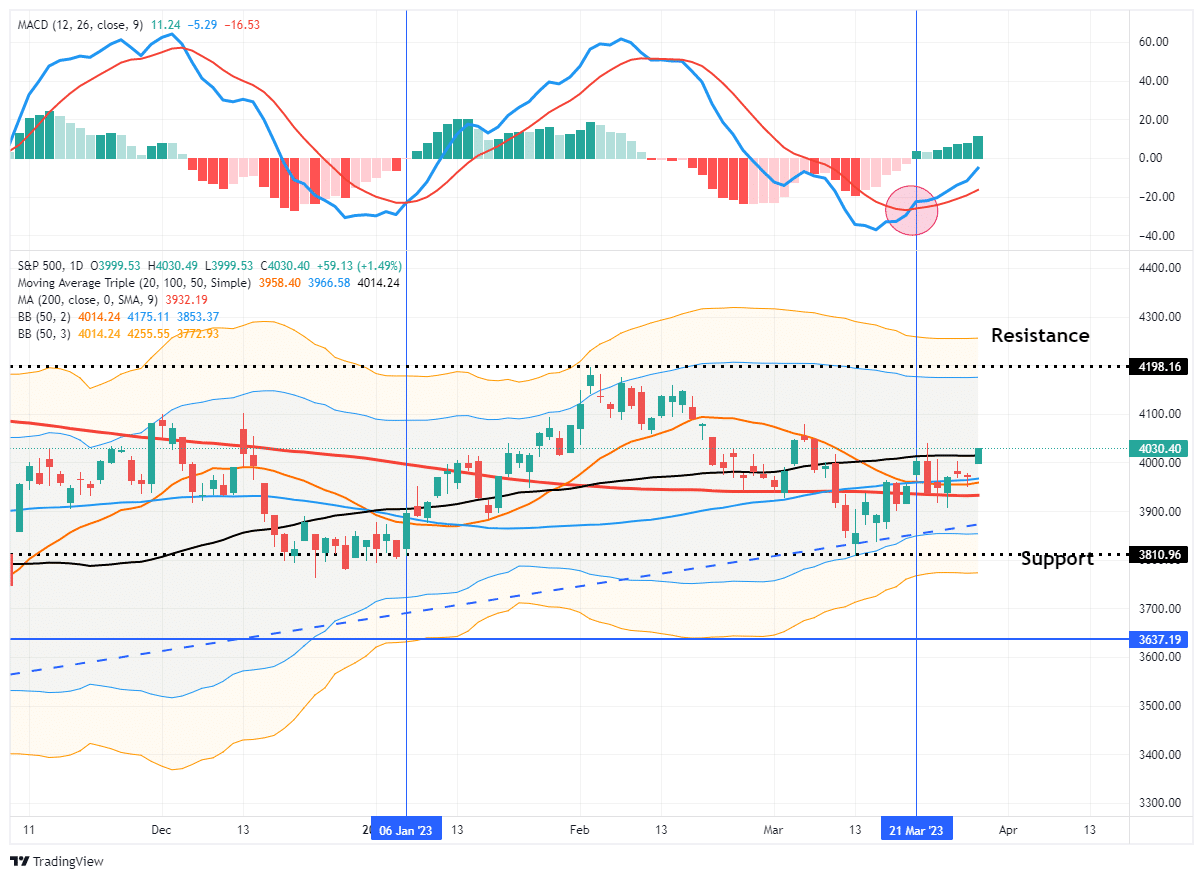

Market Trading Update

Yesterday, the market regained its bullish swagger as banking and recession fears continue to fade. The S&P 500 cleared its 50-DMA, which now clears the market to rally towards our initial target of 4100. With the buy signal firmly in place and the market not overbought, the setup for a continued bullish rally into April is positive. Hold current positions and use the rally to rebalance and reduce risk accordingly.

We aren’t out of the woods regarding a further bout of economic weakness or banking issues, but those may not arise again until this summer. The lag effect of the Fed’s previous rate hikes continues to work through the system, further extracting liquidity.

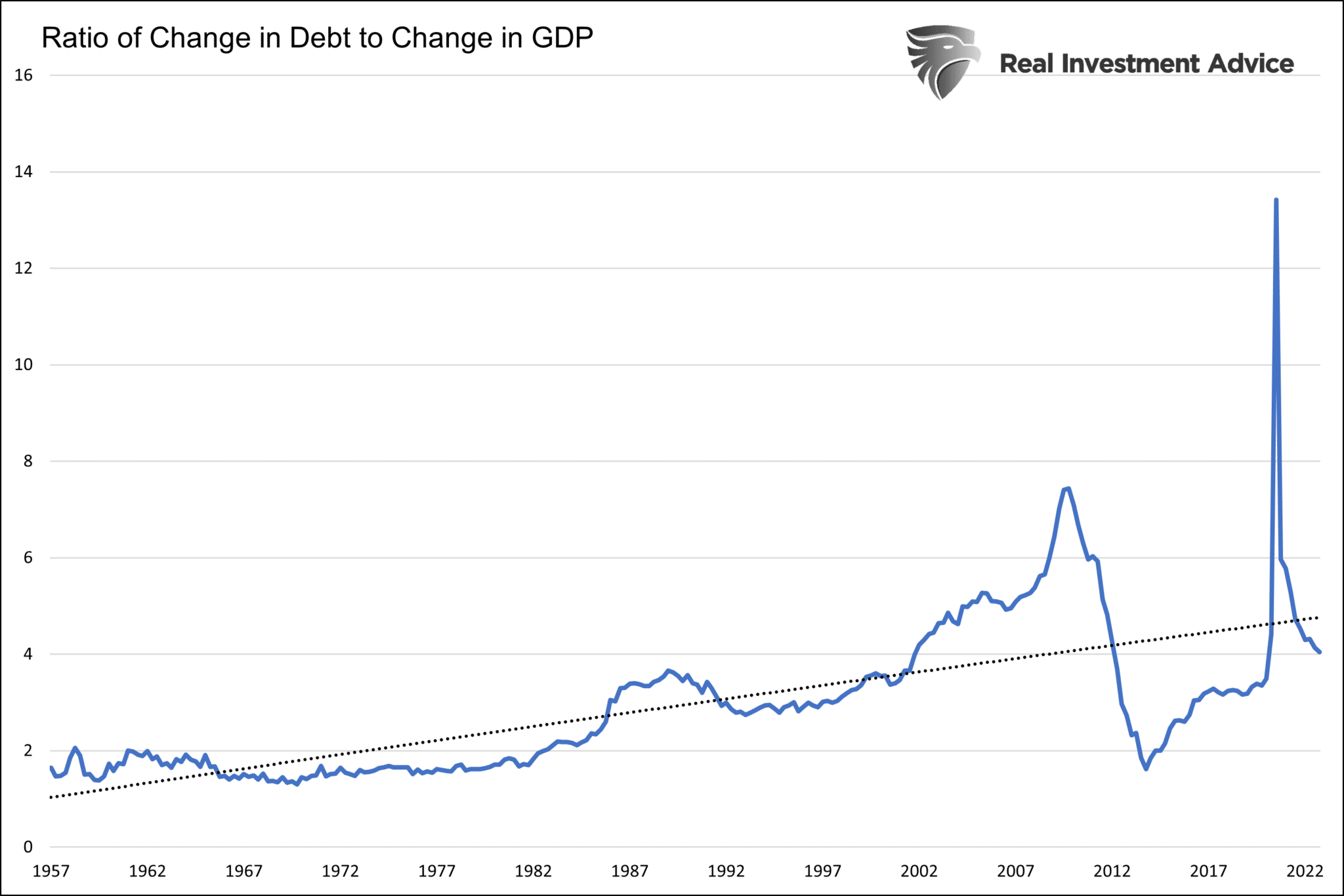

Debt = Growth

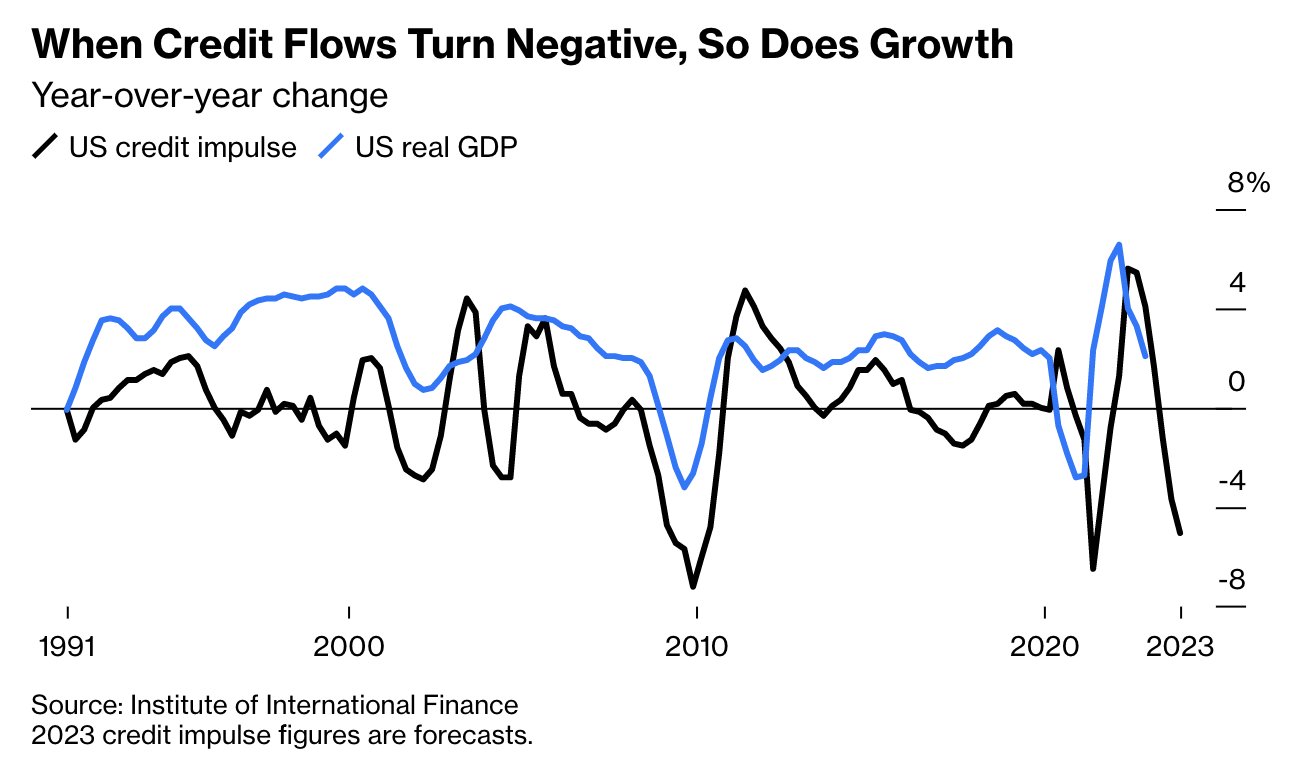

Over the last thirty-plus years, credit growth has increasingly driven the economy. As illustrated by the graph below, in 1957, debt and nominal GDP were growing at a 1:1 ratio. Based on the five-year running trend, it now takes $5 of debt to generate $1 of GDP growth. Consequently, as we are likely embarking on a period of tightening credit conditions by banks, we must ask ourselves, what happens if debt growth slows or declines?

The next graph, courtesy of Goldman Sachs and the Institute of International Finance, helps answer our question. The sharp decline in their measure of credit impulse portends that real GDP growth could decline by two to five percent. The term credit impulse was coined by a Deutsche Bank economist in 2008. He defines credit impulse as the change in new credit issued as a % of GDP.

Bond Yields Could Plunge

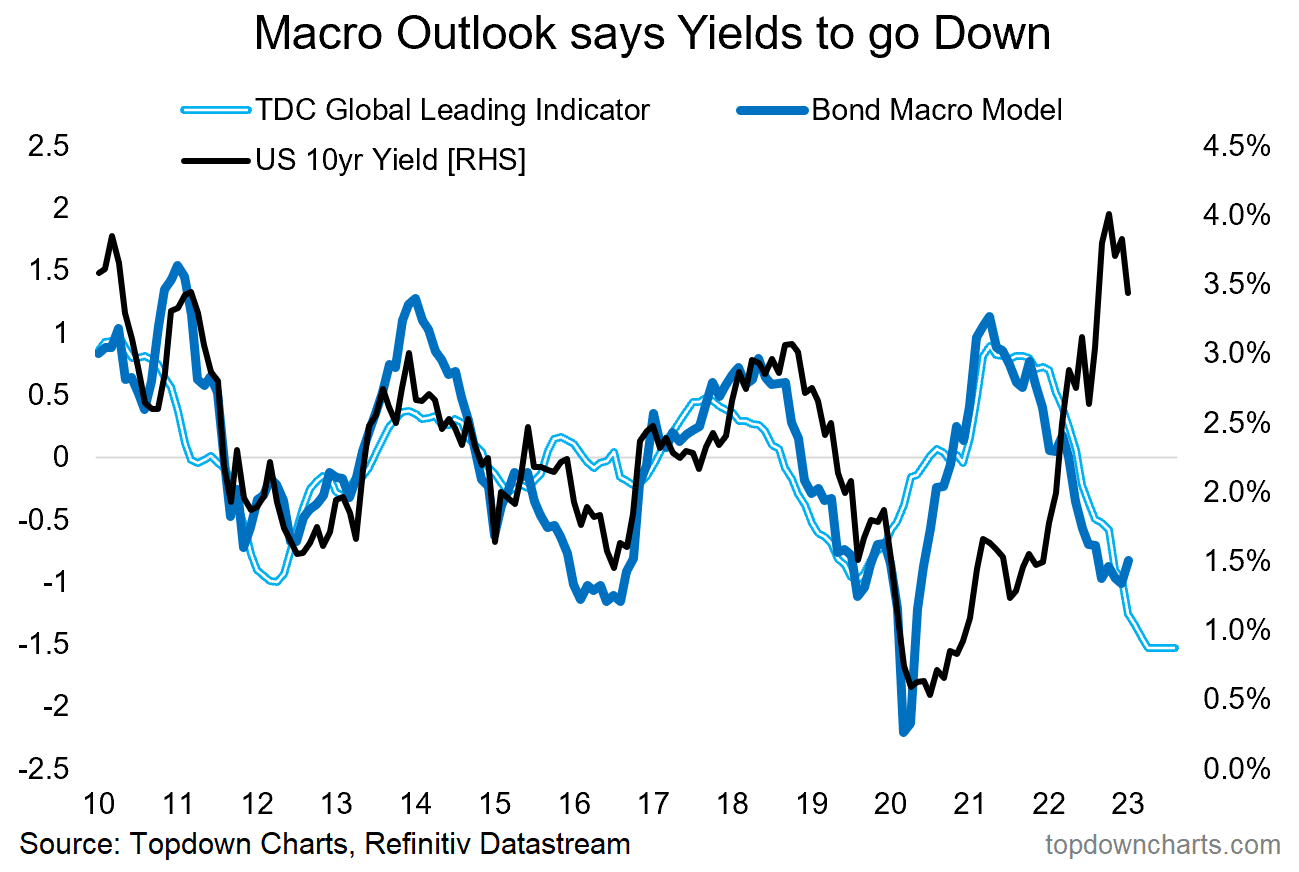

The graph below from Topdown Charts shows the strong correlation and recent divergence between leading global economic growth indicators and bond yields. The current divergence is startling but unsurprising, given that inflation remains sticky. Therefore, assuming the leading economic indicators forecast proves correct and the economy falls into a recession, inflation will fall rapidly. Consequently, ten-year UST yields could fall below 2% or lower if that occurs.

SVB’s Weakness and Fractional Reserve Banking

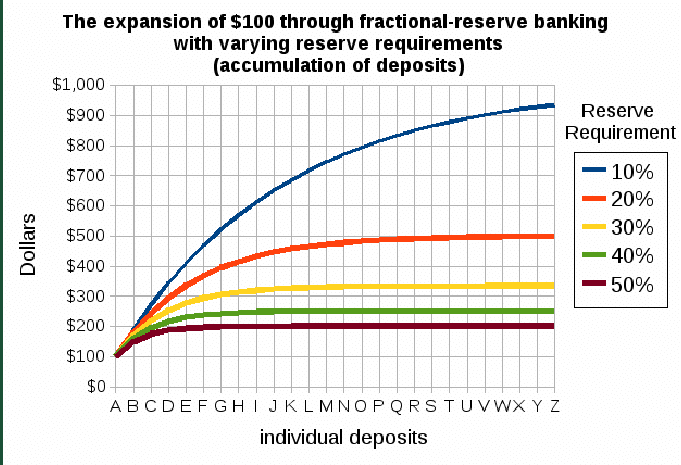

The U.S. monetary system and most others are based on fractional reserve banking. Basically, one dollar of a deposit can be turned into about nine dollars. Therefore, the financial system has ten dollars of assets but only one dollar of real money backing said assets. A dollar of assets must be sold if a dime is withdrawn from the bank.

With that, let’s dig into SVB’s Achilles heel. Per the FDIC, SVB’s ten largest deposit accounts totaling $13.3 billion, accounted for about 8% of SVB’s total deposits. As discussed in our example, banks typically hold about ten percent of deposits and lend out the rest. In the case of SVB, losing just those ten accounts left the bank having to sell about $100 billion of assets. Assuming the loans were trading at 90 cents on the dollar, the bank realized an approximate $10 billion loss. They likely lost much more than 8% of deposits, and the assets were probably sold below 90 cents on the dollar.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.