Deutsche Bank shares fell more than 10% on Friday and over 30% since March 1 as investors grew anxious about the banking sector’s health. The impetus behind Friday’s decline was a surge in its credit-default swaps (CDS). Credit default swaps are derivatives allowing investors to hedge a company’s credit risk. If the associated company defaults, the insurance owner is made whole. Basically, the insurance holder receives the difference between the bond’s par value and the company’s liquidation value. Five-year credit default swaps on Deutsche Bank jumped from 80 bps to 160 bps over the last few weeks. Buyers of insurance on Deutsche Bank are willing to pay 1.60% per year to insure their Deutsche Bank bonds against default.

The table below shows the recent CDS prices for nine of the world’s largest European and U.S. banks. Chinese and Japanese banks show little financial stress at this time. None of the CDS readings are overly disturbing. However, CDS levels can rise quickly, providing little advanced warning. For instance, the five-year CDS on Credit Suisse was trading at around 400 bps throughout last year and a week before they were bought for pennies on the dollar. Its CDS surged to 1266bps in a matter of days before UBS bought them out. Insurance buyers had to pay 12.66% a year to insure their bonds. Because Credit Suisse was acquired and UBS assumed their bonds with stipulations, insurance holders may not get paid a dime.

What To Watch Today

Economy

Earnings

Market Trading Update

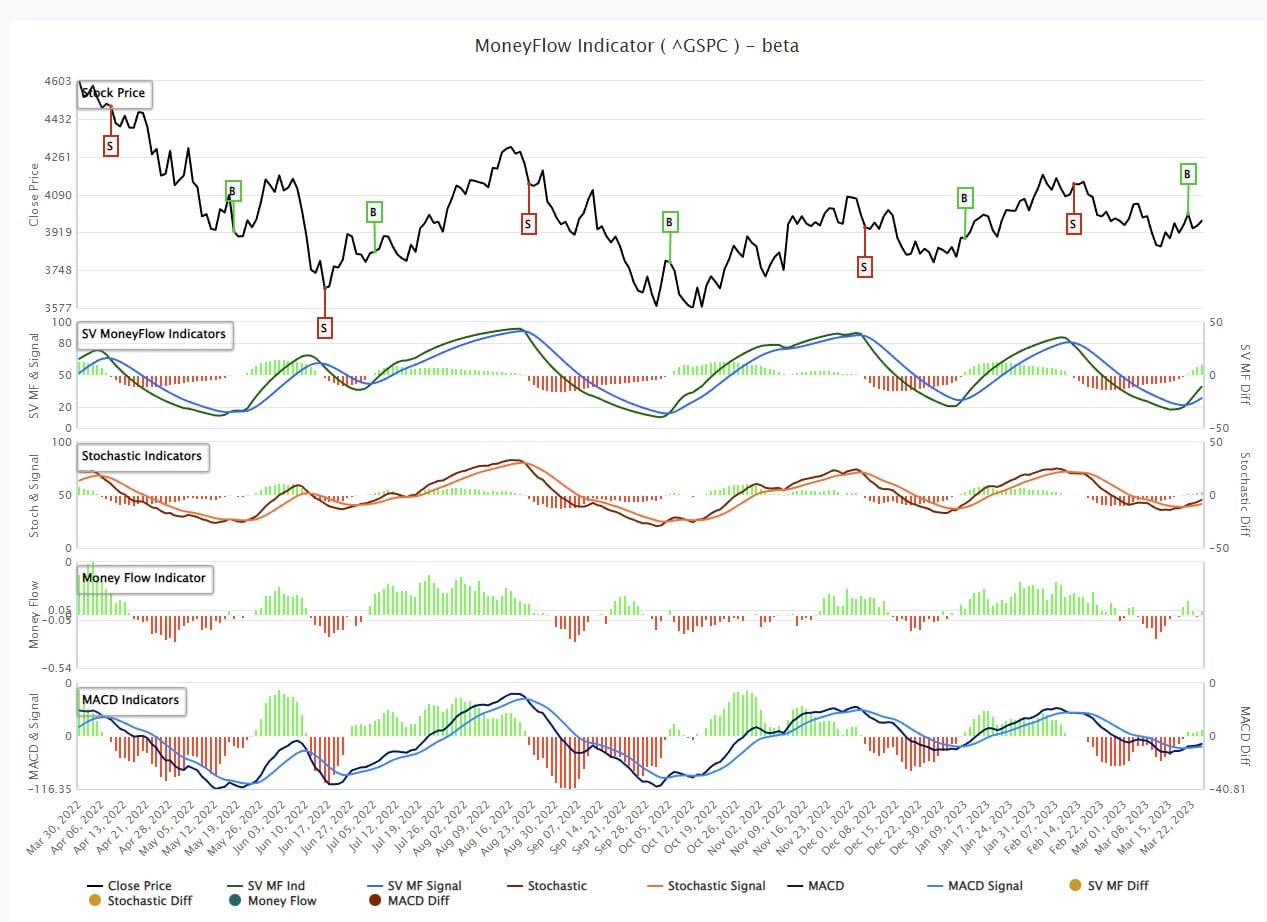

This past week, despite concerns of a banking crisis, the markets triggered multiple buy signals due to the runup before the FOMC Meeting.

These buy signals follow our early February article discussing the “sell signals” at that time.

“That commentary remains vital as our primary short-term ‘sell’ indicator has triggered for the first time since early December. Such has previously provided excellent signals of corrections and rallies. The chart below is courtesy of SimpleVisor.com and shows our proprietary money-flow indicator and the Moving Average Convergence Divergence (MACD) signal.

While that sell signal does NOT mean the market is about to crash, it does suggest that over the next couple of weeks to months, the market will likely consolidate or trade lower. Such is why we reduced our equity risk last week ahead of the Fed meeting.”

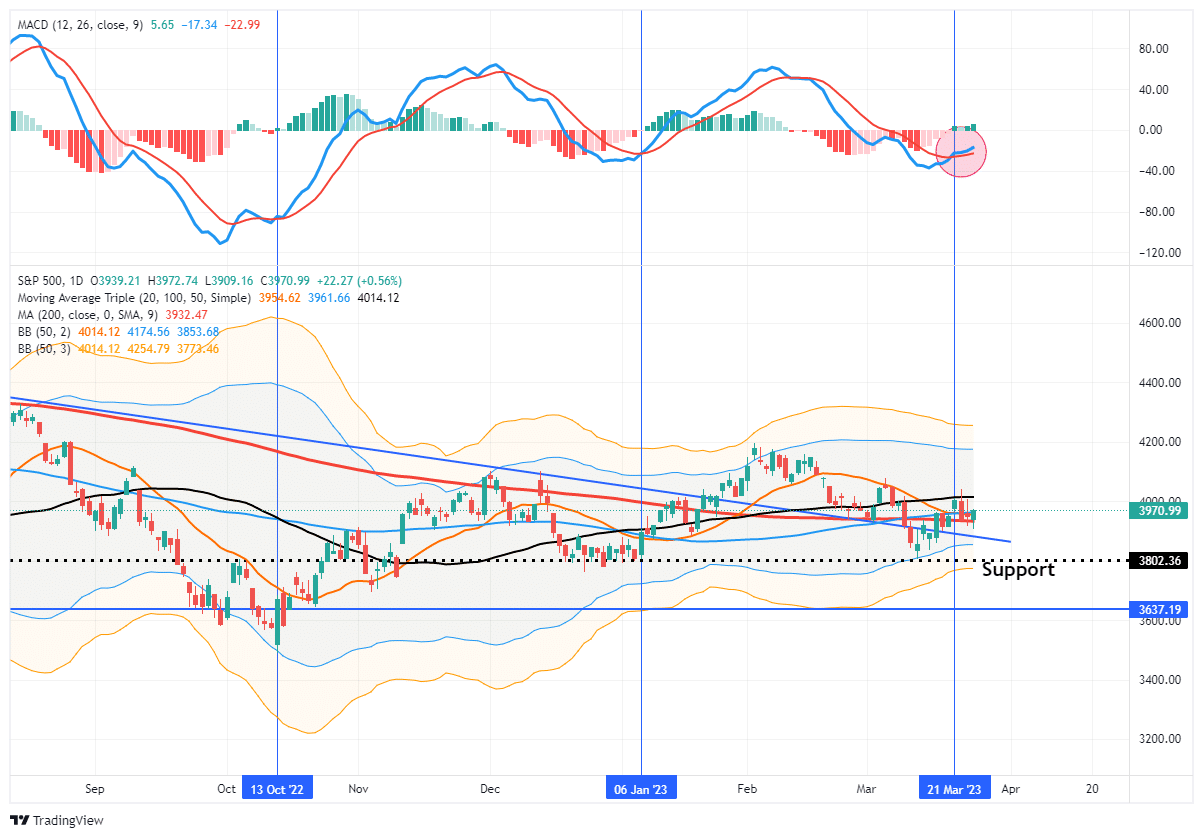

Following that article, the market declined, taking out the 200-DMA and breaking the key uptrend support from the October lows. However, the market did hold support at the December lows keeping the bullish trend intact. However, this past week, those sell signals reversed to buy signals.

The MoneyFlow chart is updated below, showing the new “buy signal” that occurred on Tuesday.

It isn’t just the MoneyFlow signal suggesting the bulls have regained control, but also the Moving Average Convergence Divergence indicator (MACD), triggering a confirming “buy signal.”

With these buy signals in place, investors should modestly increase equity exposure, as the most likely path for stock prices is higher over the next couple of weeks to months. However, with the banking crisis unfolding, such could limit any upside to equity prices near term until the crisis is “contained” or the Fed reverts to monetary accommodation.

While there is a lot of “headline noise” surrounding the recent banking troubles, the markets ultimately respond to monetary support. The recent Fed and Treasury interventions are the first steps to more accommodation. While the supports don’t liquify markets directly, the question is whether investors will step into risk on expectations of more accommodation to come.

A look back at the history of bailouts and accommodative actions by the Fed, and its shaping of investor behavior, can give us some clues as to potential market reactions.

Read the rest of the newsletter.

The Week Ahead

Many Fed speakers will opine on last week’s rate hike, their forecast for future actions, and thoughts on the banking crisis this week. Will they continue to stand united in their quest to fight inflation? Or will some members prioritize financial stability?

On the economic front, Friday will prove the most important day. PCE will provide the latest inflation update. A low reading may provide further evidence to investors the Fed may pivot soon. Also of note is the University of Michigan consumer sentiment survey. It may be early, but seeing how the recent banking issues affect consumers’ outlooks will be interesting.

Tracking the Banks

A reader emailed us, asking what we follow to track the banking crisis. In addition to watching the broader stock, bond, commodity, and foreign currency market, we also pay close attention to stock prices in the financial sector. Back in 2008, CDS and stock prices often portended trouble. For this reason, we are closely following the regional bank stocks. We use the SimpleVisor Heat Map (Dashboard > Market X-Ray) to do so. As we show below, financial stocks were relatively tame on Friday. The bigger banks were lower, while the regionals fared better.

Real Rates vs. Nominal Rates

Did the Fed raise interest rates too much, or do they have more work to do? Most people look at nominal interest rates to answer the question. Quite often, their answer is based on the deviation from recent experience. For example, the 10yr UST note yields 3.35%. Since 2010, the average yield has been 2.28%. Based solely on that analysis, the yield is over 1% too high.

Only looking at nominal rates fails to consider inflation. Inflation expectations represent the expected actual economic cost of debt. For example, a company paying 10% to issue a bond may be thrilled with such a rate if it can raise prices by 15% a year. In that case, their real rate interest rate is -5%.

The graph below plots ten-year real yields, nominal yields, and inflation expectations. The current 10-year real yield of 1.04% is higher than any level since the Financial Crisis. However, it is still well below the levels of the prior thirty years. Based on recent experience, we can claim real rates are restrictive. But on a longer-term basis, they remain very easy.

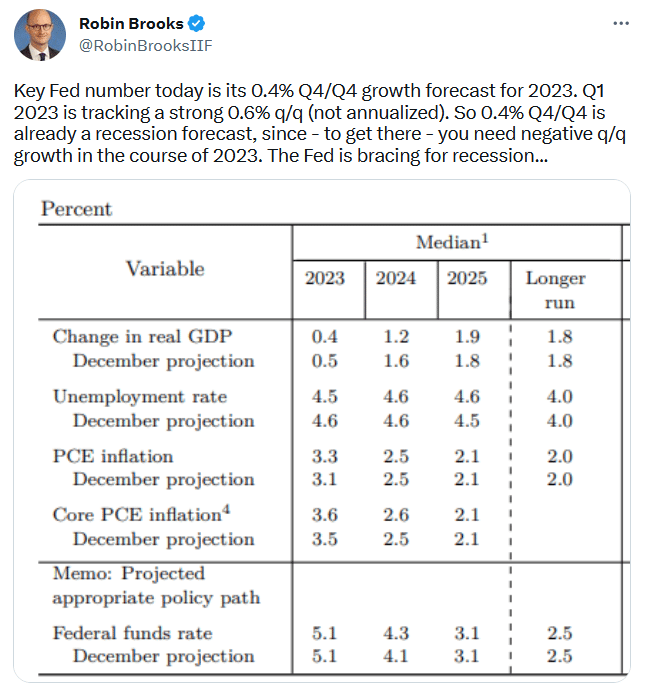

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.