Over this past week, numerous Fed members commented that the Fed may be ready to pause its series of rate hikes that started in March 2022. Specifically, Logan (Dallas President), Waller (Fed Governor), and Jefferson (Vice Fed Chair) all said they believe a pause is possible because the recent spike in long-term interest rates has sufficiently tightened financial conditions. Atlanta Fed President Bostic took it a step further and said we no longer need to increase rates.

Philadelphia Fed President Harker spoke on Friday, further stressing what we believe is the new Fed modus operandi:

Absent a stark turn in what I see in the data and hear from contacts, both in one-on-one conversations and in forums like this, I believe that we are at the point where we can hold rates where they are.

Harker goes on to say, “Disinflation is underway.” He acknowledges the lag effects of prior hikes and ongoing QT will continue to present a growing headwind to the economy. In his words, “By doing nothing (referencing a pause), we are still doing something. And, actually, we are doing quite a lot.” These series of subtle statements may help explain why stocks were seemingly unaffected by the war in the Middle East.

What To Watch Today

Economics

Earnings

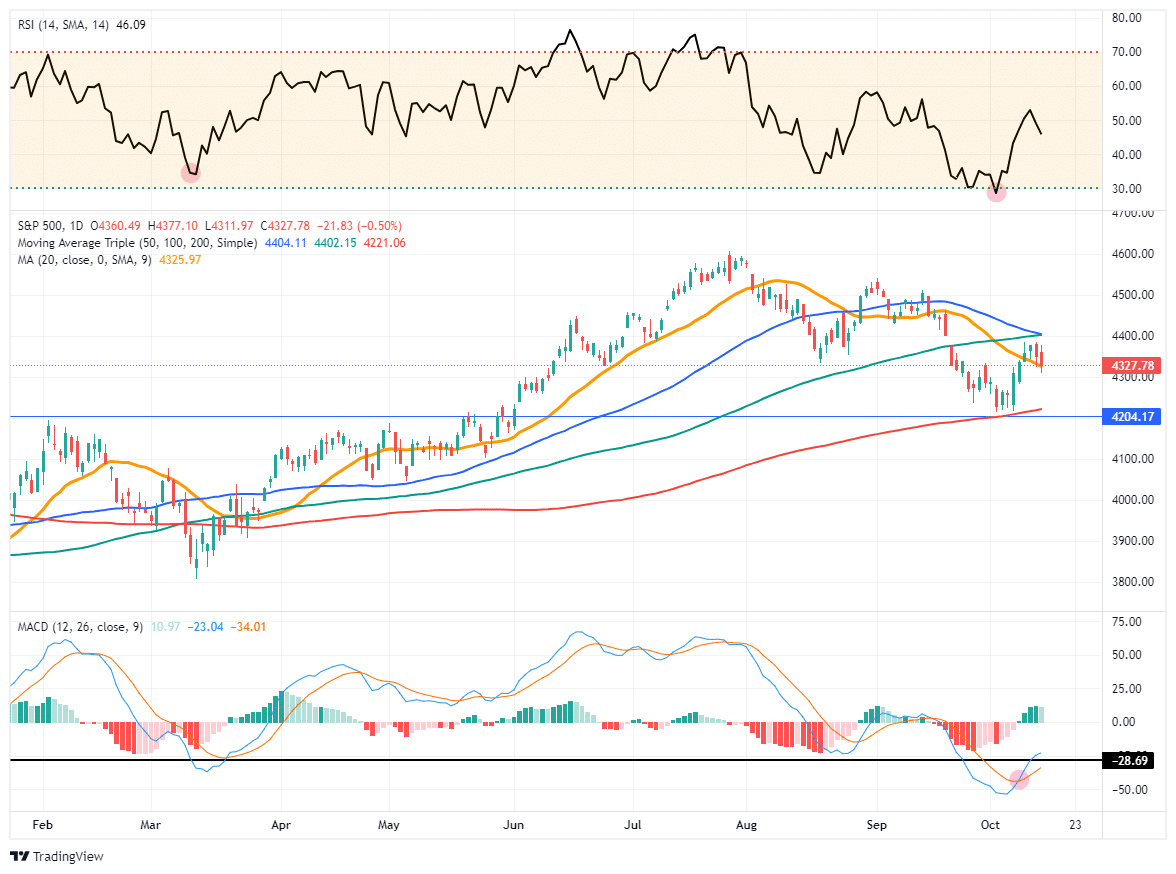

Market Trading Update

The conflict with Israel took center stage last week. However, the markets also had to deal with PPI, CPI, and the official kick-off of earnings season. From a market trading update perspective, let’s start with a review from last week. To wit:

“The market failed to hold that initial support level and quickly tested the 200-DMA as expected. The good news is the market bounced sharply off support levels on Friday, reducing the MACD ‘sell signal.’ If the market can follow through on this rally early next week, we could see a ‘buy signal’ triggered.”

As shown, that is what happened as stocks pushed higher, triggering the MACD “buy signal.” As we will discuss below, that trigger also signals the start of the “seasonally strong” period of the year. The market did run into resistance at the 50- and 100-DMA but continues to hold above short-term support at the 20-DMA. With the market not yet overbought, we could see some consolidation at these levels into next week before another attempt at resistance.

The attempt at resistance will mostly depend on earnings reports as they get underway in earnest next week. As discussed below, the bar has been lowered substantially from last year, so we should expect a high “beat rate” of earnings. The key, however, will be forward guidance that leads to concerns about a slower economy next year.

We will be watching those reports closely.

While there are certainly many concerns, particularly related to this latest conflict in the Middle East, the market continues to act bullishly for now. The summer correction remained within the confines of seasonal weakness, and the rally off of support, as noted, keeps the market’s bullish trend intact for now.

Short-term declines can be used to add to equity exposure as needed, but continue to manage risk as we head into year-end.

The Week Ahead

The number of earnings reports will increase this week. Shown below is the earnings calendar for larger companies.

On the economic front, Retail Sales on Tuesday will be the most followed data release. Expectations are for a gain of 0.3% for the month. Analysts expect the year-over-year rate to be +1.5%, or about 2% below the inflation rate.

Fed Chairman Powell will speak on Thursday. It will be interesting to see if he hints at a pause, as discussed in the opening section. There are many other Fed speakers throughout the week.

JPM Earnings And An Ominous Warning From Jamie Dimon

The big banks announced Q3 earnings on Friday, which were generally better than expected. The nation’s largest bank, JPM, beat expectations on both revenue and earnings. Revenues were almost $1 billion above estimates at $40.69 billion. Earnings beat by 0.41 cents per share. They did mention the large banks are in a sweet spot of sorts. Interest income is rising, yet credit loss expenses are below normal. They do acknowledge the differential will normalize. JPM’s deposits rose slightly, likely garnering deposits from smaller banks. JPM’s earnings were also boosted by their purchase of First Republic, one of the banks that failed earlier this year.

Despite mentioning economic deterioration and the likelihood of rising credit losses, its provision for credit losses was $1.1 billion less than analysts expected. Either JPM is not overly worried about potential loan losses, believes they overallocated in prior quarters, or they are juicing its EPS by not withholding enough reserves. Based on the following quote from RBC bank analyst Gerard Cassidy, it appears the latter- “We expect loan loss provisions to increase materially compared to the third quarter of 2022 as we expect banks to build up loan loss reserves.”

On a separate note, JPM’s CEO, Jamie Dimon, shared some ominous words about the economy and geopolitical events.

…the war in Ukraine compounded by last week’s attacks on Israel, may have far-reaching impacts on energy and food markets, global trade, and geopolitical relationships. This may be the most dangerous time the world has seen in decades.

Citi and Wells Fargo

Wells Fargo (WFC) also reported better-than-expected numbers and, like JPM, withheld less for future credit losses than was expected. The size of their loan and deposit books both fell slightly. Such attests to the broad tightening of financial conditions and disincentives to make loans due to the inverted yield curve.

Citigroup (C) followed in JPM’s and WFC’s footsteps and beat on revenue and earnings. C, unlike JPM and WFC, actually released net loss reserves.

The bottom line from the three largest banks is that earnings are being boosted by higher interest income and lower credit losses than would typically be expected. Further, they all contributed less than expected to loan loss reserves, which help earnings today. However, the odds of credit losses increase proportionally with interest rates and economic weakness. The banks may stay in the sweet spot until the economy weakens due to higher interest rates. Such is the lag effect.

The graph below shows that JPM stock has easily outperformed the other largest American banks. Also note that Citi, U.S. Bankcorp, and Wells Fargo are near their 2020 pandemic lows.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 3

2023/10/16