A recession is very unlikely if the only recession gauge one was following is the spread of junk bond yields to U.S. Treasuries. Typically, leading up to a recession, junk bond spreads versus Treasuries increase as earnings waver and the risk of default increases. Despite a very aggressive Fed, higher borrowing costs, and weakness in equities, junk bond spreads are hovering near their pre-pandemic averages. The graph below shows the yield spread of BB-rated junk bonds to U.S. Treasuries is nearly 1% above its 2021 lows but slightly below its pre-pandemic average. Further, as shown in blue, the average spread between junk and investment-grade (BB and BBB) bonds is also near historical averages.

There is no stress in the corporate bond markets. As we saw in 2020 and 2015, financial stress and instability can happen quickly, and junk bond yield spreads can rise rapidly. Investment grade and junk bond spreads to Treasuries are an important gauge the Fed closely follows. Seeing that spreads are normal likely gives the Fed confidence that they can continue to raise rates.

What To Watch Today

Economics

- Dallas Fed Manufacturing Activity, November (-23.0 expected, -19.4 prior)

Earnings

- No notable earnings reports

Market Trading Update

This past week, the market jumped to the top of its recent trading range and continues to work in a consolidative manner. While the MACD “buy signal” is overbought, the market’s momentum is still bullish. The 200-dma will provide the next level of serious resistance.

Most notably, the number of stocks trading above their respective averages continues improving. While this is bullish, it is also typical, at these levels, to align with short-term market peaks.

One issue challenging this rally remains the drop in the volatility index. As noted last week, net bullishness rose to the highest level since the July rally. That bullish increase coincides with a sharp decline in the volatility index as investors think the “bottom is in.“ So far this year, a reading of 20 or below has provided a good signal to take profits and reduce risk.

As noted, the Wednesday rally followed the release of the FOMC minutes, which read more “dovish.” While there was no mention of a “pivot” or a “stall,” investors seem to like the idea of a slower pace of rate hikes. However, traders overlooked the Fed’s statement they will increase rate hikes in 2023.

The rally reversed a majority of the previous oversold conditions and net bearishness. Therefore, some profit-taking and risk reduction in portfolios remain prudent. While the expectation for a rally into year-end remains, we could see some selling in the first half of December from tax loss harvesting and portfolio rebalancing. Such will likely provide a tradeable opportunity into year-end and the beginning of 2023.

The Week Ahead

The next two weeks will be important as the Fed and investors will see the latest inflation and employment data. ADP on Wednesday and the BLS Jobs Report on Friday are expected to show the labor force grew by about 200k jobs in November. Besides the recent uptick in jobless claims, nothing leads us to believe labor data will be disappointing. However, there are an increasing number of corporate layoff actions. Therefore a lower-than-expected number and increase in the unemployment rate should not come as a total surprise.

The Fed’s preferred inflation gauge, PCE, will be released on Thursday. Expectations are for the monthly core PCE to remain the same as last month at 0.5%. The year-over-year rate is expected to decline to 4.9% from 5.1%. Investors hope PCE comes in below expectations, as CPI did a few weeks ago.

Chairman Powell will speak at 1:30 PM ET on Wednesday. He has been quiet since the last Fed meeting, so this engagement allows him to update investors on the Fed’s path ahead.

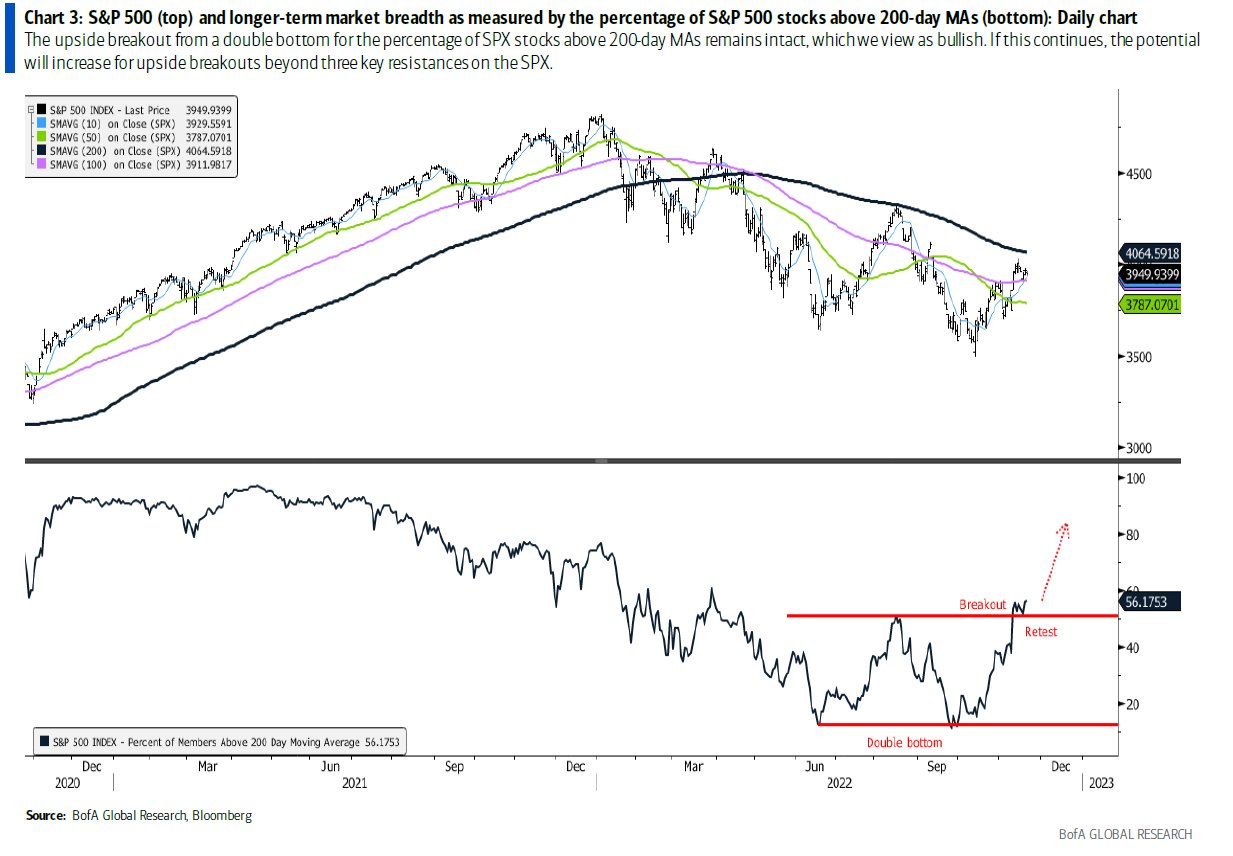

Improving Market Breadth

The graph below from Bank of America provides a little optimism. Breadth is improving, and a bottom might be forming in the S&P 500. Throughout the decline in 2022, the percentage of S&P 500 stocks trading above their 200dma was trending lower, similar to the index. With the recent rally, the percentage of stocks trading above their 200dma is now above the prior peak. The higher high in the breadth indicator introduces a positive divergence. Ideally, we want to see the S&P 500 trade above the 200dma to confirm this signal. The 200dma capped the prior rally. Caution is warranted as the S&P 500 rose above it for a short period during the April rally, but it turned out to be a trap for bulls.

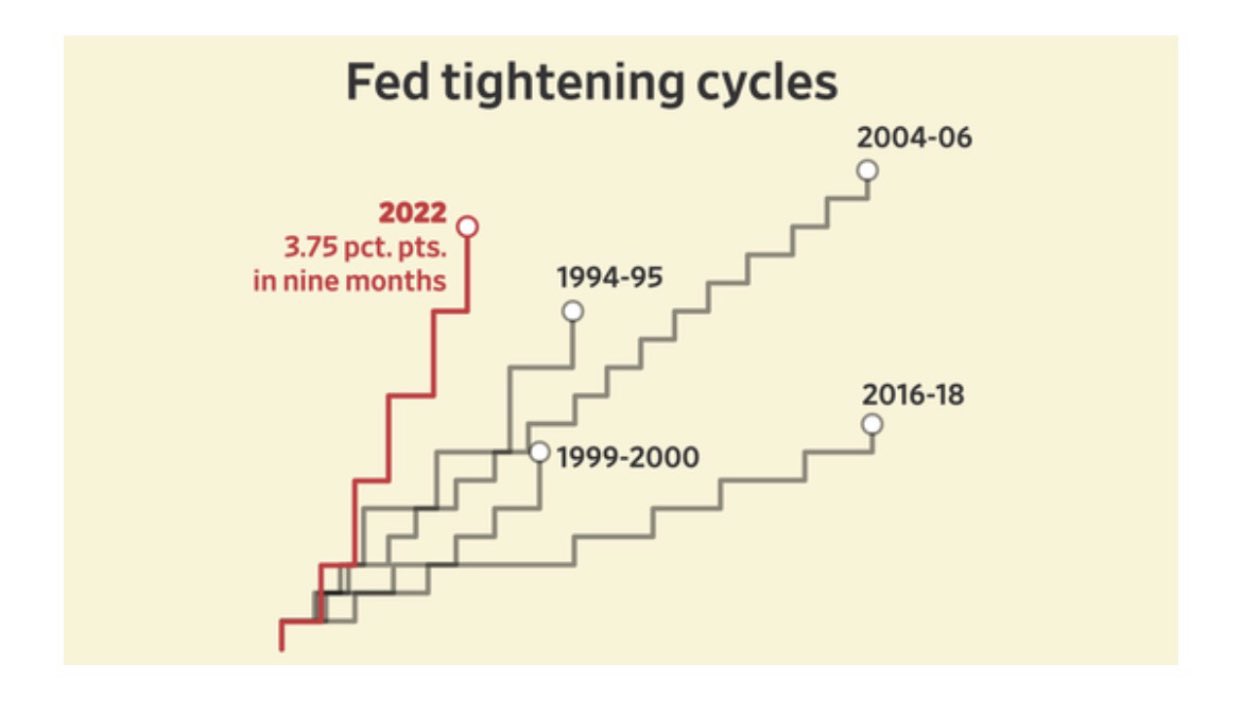

Fed Tightening Cycles

The graph below compares the current Fed tightening cycle to the previous four. The recent 3.75% increase in nine months is more aggressive than the previous four. However, when assessing the amount of tightening, we must also consider the rate itself. Even with the sharp increase in Fed Funds, Fed Funds only stands at 3.75%. That is decently higher than the prior hiking cycle ending in 2018, when the terminal rate hit 2.5%. But it remains well below the prior three. Fed Funds topped at 6.0%, 7.0%, and 5.5% in chronological order from 1994 to 2006.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.