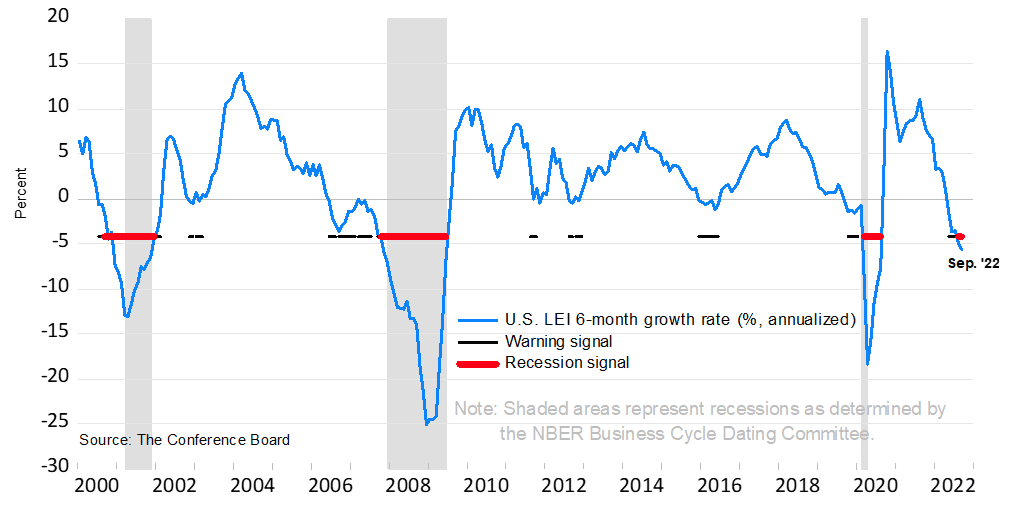

The Conference Board’s Leading Economic Indicators Index (LEI) is a robust predictor of coming recessions, as shown below. The six-month percentage change in leading economic indicators portends a recession is likely. Per the Conference Board: “US leading economic indicators fell again in September, and its persistent downward trajectory in recent months suggests a recession is increasingly likely before yearend.”

Of the ten components comprising the LEI, six are already at weak levels. Three are average, and only one, unemployment claims, remains strong. Despite weakness in leading economic indicators of the economy, the Board’s Coincident Economic Index (CEI) measuring present conditions remains strong. The divergence between CEI and leading economic indicators might explain why the Fed remains very hawkish. As we often note, monetary policy works with a lag. Therefore, we hope the Fed is considering the lag between leading and coincident economic indicators as they formulate policy.

Opening paragraph

What To Watch Today

Economy

- Chicago Fed National Activity Index, September (0.00 prior)

- S&P Global U.S. Manufacturing PMI, October Preliminary (51.0 expected, 52.0 prior)

- S&P Global U.S. Services PMI, October Preliminary (49.6 expected, 49.3 prior)

- S&P Global U.S. Composite PMI, October Preliminary (49.5 prior)

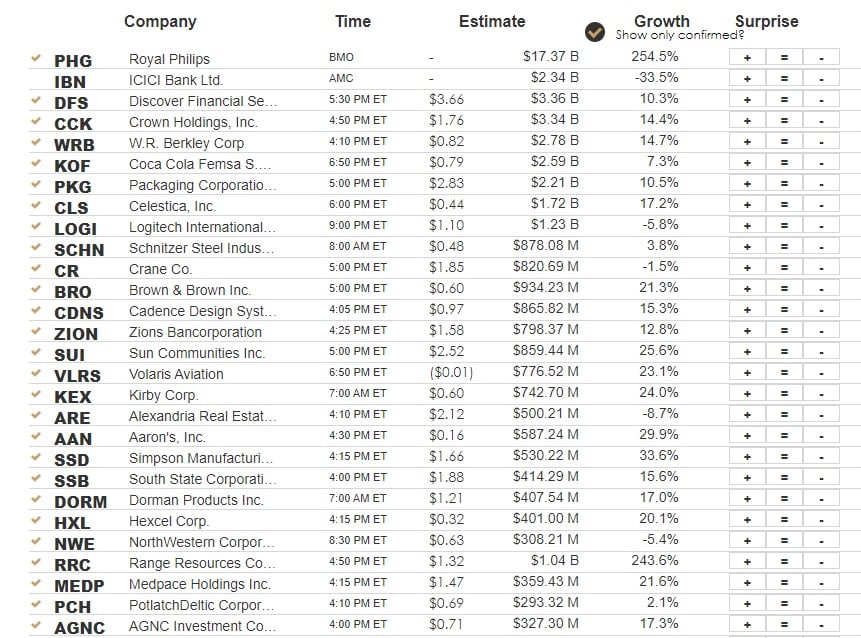

Earnings

Market Trading Update

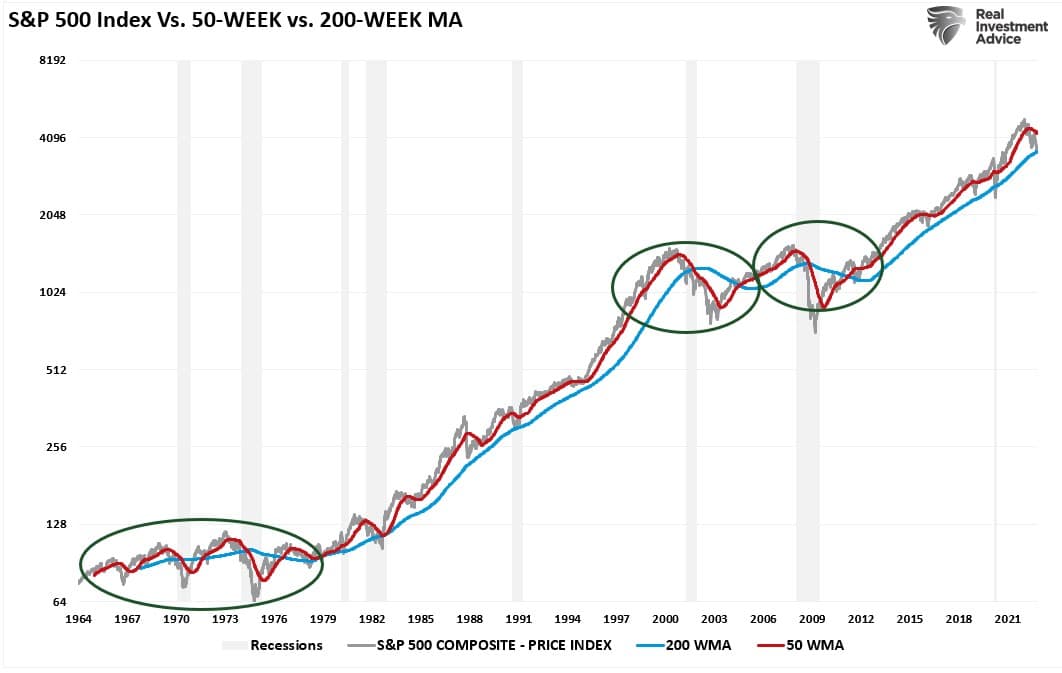

Last week, we discussed the market was testing a critical support level that separates bull markets from bear markets. To wit:

“Notably, the market continues to flirt with support at the 200-week moving average, which has defined the ‘bullish trend’ since the financial crisis lows. In other words, despite the ‘correction’ from this year’s highs, the ongoing bull market remains intact. However, a ‘confirmed break,’ which will be a close, retest, and failure of that bullish trend, will constitute a bear market.”

I updated that chart to include the 50-week moving average and recessions. The importance of these additional measures shows that in all previous bear markets and recessions, the 50-WMA crossed below the 200-WMA. That cross also coincided with a price break below the 200-WMA.

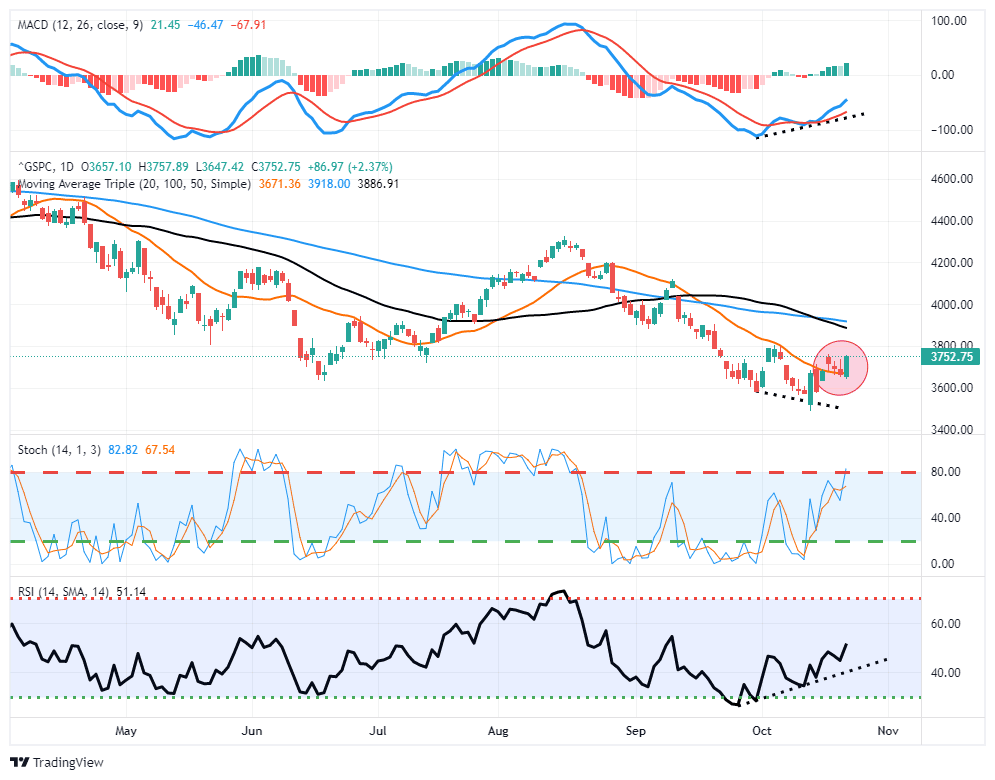

Notably, while the market held that critical support level this past week, there was also no progress on the anticipated reflexive rally. Such is because investors have now become “bear bitten” and are unwilling to “buy the dip.”

This past week was another disappointing week in terms of market action. However, there were some positive developments short-term. The market bounced off the 20-dma, turning that previous resistance level into support. That bounce came on rumors from the “Fed Whisperer,” Nick Timaros of the WSJ, the Fed may be considering slowing the pace of rate hikes in December. Such was a welcome relief for the beaten-up bulls, and stocks rallied sharply to close the week.

It will be necessary for the market to rally some more next week and ideally rises above 3800 to confirm another “bear market” rally is underway. Furthermore, the positive divergences of the MACD and RSI indicators also support the short-term bullish outlook.

With the technical action of the market supporting a rally, October tends to mark lows as the seasonally strong period gets underway. However, it is important not to mistake a rally from oversold conditions as a market bottom. There are still a tremendous number of headwinds that suggest we won’t see the final market lows until next year.

The Week Ahead

This week’s economic calendar includes new home sales and building permits. We suspect housing data will be weak as mortgage rates are north of 7% and homebuilder sentiment is poor. In last Thursday’s Commentary, we wrote the following about the latest NAHB survey results:

The NAHB survey of home builders fell to 38, approaching the low of 30 in April 2020. More importantly, the index is plummeting at an extremely sharp pace. The six-month decline in the index is a four-standard deviation event.

The third quarter GDP will be released on Thursday. Expectations are for a 2.5% increase. The Atlanta Fed estimates it comes in close to 3%. While strong economic growth should be welcome news, the Fed will likely frown as it makes their job to fight inflation harder. PCE price data for September will be released on Friday. Expect the core PCE price index to increase by .4%, .2% less than last month.

The Fed will be quiet as they enter its media blackout period ahead of the November 2nd FOMC meeting. The big tech companies, including Apple, Microsoft, Google, and Amazon, report earnings this week. Their results may help set the price trend for the week. As we share below, election polls will also be closely followed this week.

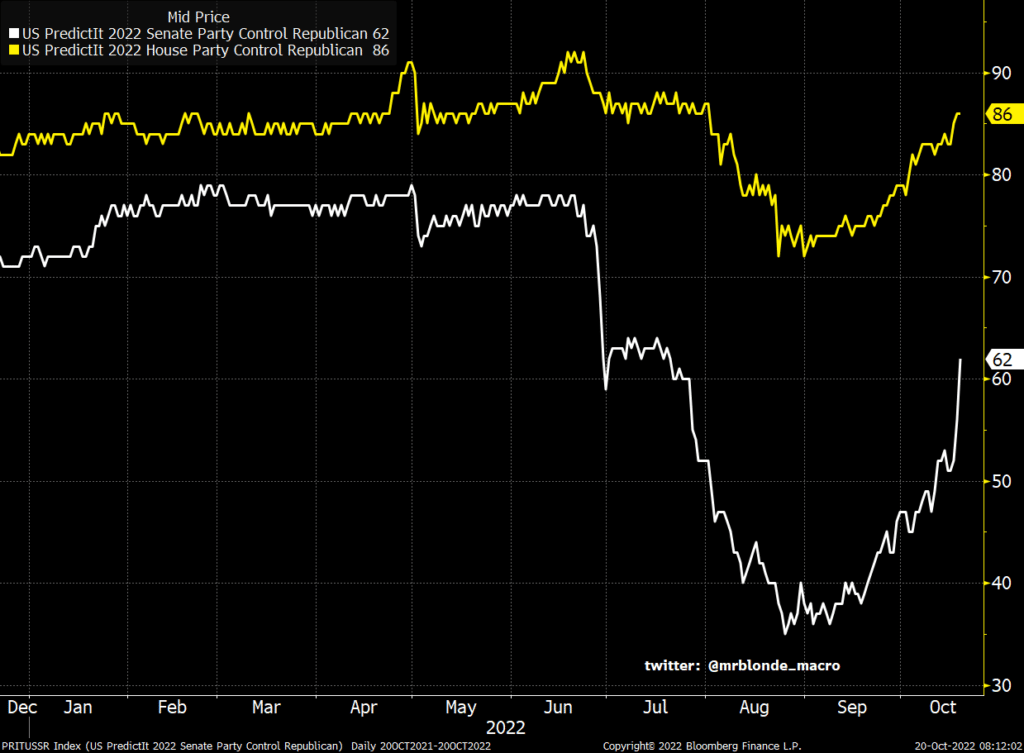

Election Odds and Fiscal Stimulus

As investors, it’s imperative we put aside our political preferences and focus on how the coming mid-term election might affect the economy and markets.

Currently, with a slim majority in the Senate and control of the House, the Democrats have struggled to pass significant bills. More fiscal spending would likely have occurred had the Democrats won a few more Senate seats in the last election. As shown below, the odds are increasing that Republicans will take control of the House and or Senate. Therefore a Republican win in either House will make it even harder for President Biden and the Democrats to pass fiscal spending bills.

Given the trouble that bond markets are experiencing, reduced spending, which limits debt issuance, should, on the margin, be good for bond prices. However, if the economy weakens, the economy may not benefit from higher fiscal spending levels that occurred in the past. Regardless of your politics, Republican control of at least one of the two houses should benefit bondholders but to the economy’s detriment.

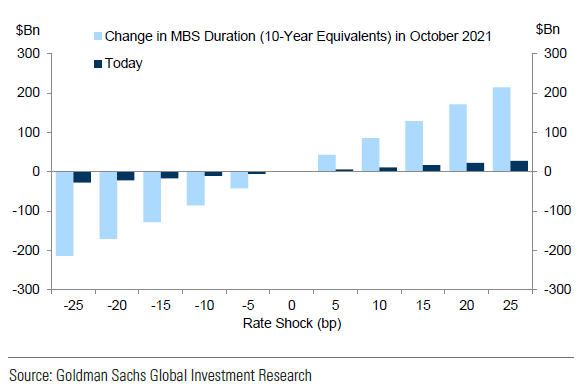

MBS Should Provide Hope for Bond Investors

The graph below is very important for bond investors, but so few will recognize its importance. In a nutshell, it shows that large institutional MBS (Mortgage-Backed Security) investors no longer have to short Treasury bonds or other instruments that have been pressuring bond yields higher. To help explain the graph’s importance, Michael Lebowitz will post an article on Wednesday explaining MBS and the role its investors have on the broader fixed-income markets.

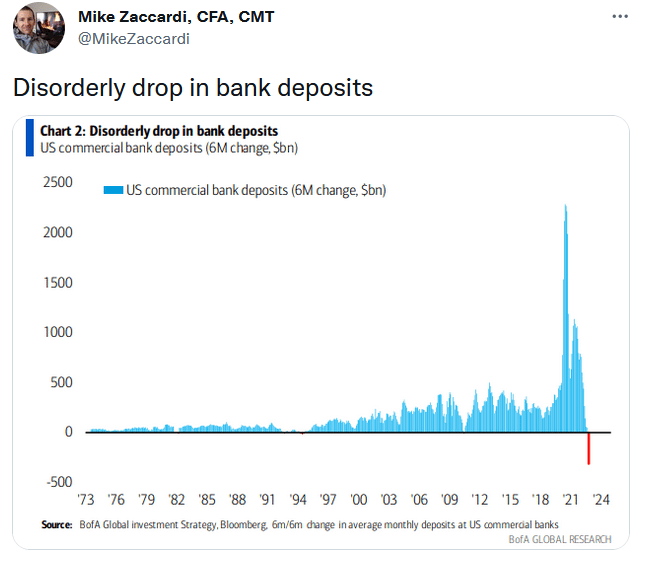

Tweet of the Day

For more on the importance of this tweet, read our Commentary from October 19th.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.