🔎 At a Glance

- J-Pow Sends Markets Back To Highs

- Market Valuations Don’t Matter…Until They Do.

- Portfolio Tactics For Next Week

- From Lance’s Desk: US Economy: Recent Data Suggests Risk To Earnings

- Portfolio updates & sector strategy shifts

- Market stats, screens, and risk indicators

💬 Ask a Question

Have a question about the markets, your portfolio, or a topic you’d like us to cover in a future newsletter?

📩 Email: lance@riaadvisors.com

🐦 Follow & DM on X: @LanceRoberts

📰 Subscribe on Substack: @LanceRoberts

We read every message and may feature your question in next week’s issue!

🏛️ Market Brief – J-Pow Sends Market Back To Highs

After the market slid lower all week, testing the 20-DMA on Thursday, Jerome Powell’s speech at Jackson Hole turned sentiment on a dime. The S&P 500 returned to record highs, and the Dow surged 900 points. Investors took his tone as confirmation that a September rate cut is in play. Specifically, Powell noted the slowdown in employment as a key reason for the shift in stance, as noted in the key paragraph from his speech.

“In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate.

Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance.

Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.“

Wall Street also noticed the shift in tone. Krishna Guha of Evercore ISI called it a “clear pivot to risk management.” He added the speech “gave markets permission to rally.” Bank of America’s Michael Gapen noted Powell’s comments were “dovish without overcommitting,” keeping pressure off the Fed to act immediately while softening market fears.

While stocks had been under pressure earlier this week, specifically in the overbought Technology sector, Powell opened the door for the bulls. The rally lifted risk-based sectors. Small caps led. Bitcoin and bonds bid, and homebuilders, airlines, and regional banks surged. The dollar fell as yields dropped sharply.

However, risks remain. Inflation is not yet anchored. Powell downplayed tariff impacts, but new trade policies could stoke price pressures. If data surprises to the upside, markets could whiplash. BlackRock’s Rick Rieder warned the Fed “must still see inflation trending toward target,” and cautioned that easing too fast “could reignite instability.” Don Carter at Fort Washington Investors also remained concerned, stating, “Even with Powell’s more dovish tone, the data in the coming weeks still pose some risks. The market will like this change in tone. But I think we must be careful not to get too far ahead. There is still a lot of data between now and the next FOMC meeting.”

As we will discuss in today’s newsletter, while earnings season was solid, valuations are clearly stretched. The risk to investors is that with the Fed’s next move priced in, any hesitation could lead to stocks giving back recent gains.

📈Technical Backdrop

Price remains in a primary uptrend as the S&P 500 held its initial test of the 20-DMA on Thursday. On a daily basis, the market remains well above the 20, 50, and 200 DMAs, with the top of the current trend channel rising toward 6600. Such keeps the trend constructive as long as pullbacks hold support. Short‑term pivots for the next session cluster around 6,470, with resistance being the recent all-time highs from two weeks ago.

Furthermore, daily momentum is positive but edging hot. RSI(14) sits in the low‑60s, MACD, however, remains on a “sell,” and several faster oscillators (Stoch/RSI variants) registered overbought readings into Friday’s rebound. One note is that relative strength, momentum, and money flows remain in a “negative divergence” to the market, increasing near-term investor risk. However, the “buy‑the‑dip” strategy continues to perform well for now.

Participation improved, but it’s not euphoric. Roughly 61% of S&P constituents are above their 50‑DMA and about 63% above their 200‑DMA, which is healthy, but not yet stretched. For now, breadth is supportive, but still something to monitor for confirmation via higher highs in the A/D lines.

Despite the sell-off this past week, volatility remained subdued and closed near 14 into the close, consistent with a risk‑on term structure. Options appetite is still very bullish: the 10‑day average Cboe total put/call sits near 0.84. Positioning is mixed across cohorts: NAAIM equity exposure remains high while AAII shows a cautious retail stance. After this week’s close, we will see if retail begins to chase more aggressively.

Under the surface, the week’s rebound broadened: small caps and cyclical pockets outperformed on Friday, with the Russell 2000 ripping ~4% as yields fell. Equal‑weight (RSP) has begun to show short‑term relative improvement versus cap‑weight (SPY). Even though RSP still trails YTD, it is an encouraging sign of incremental broadening. Sector‑wise, weekly performance tilted toward cyclicals (energy/materials/industrials) with defensives mixed, while megacap tech cooled earlier in the week and rejoined late.

Key Levels & Risk Markers (near‑term)

- Support: 6,385 (20‑DMA), 6,269 (50‑DMA), 6,269 (200‑DMA). A close below the 50‑DMA would signal loss of short‑term trend grip.

- Momentum guardrails: Daily RSI mid‑60s; a rollover with negative divergence would raise pullback odds.

- Internals to confirm: S&P %>50‑DMA pushing sustainably >65–70%.

- Sentiment: Watch if VIX ≤13 and put/call MA pushes lower, would increase risk of a shakeout.

Outlook for Next Week: Neutral

The primary trend is up (price above rising key MAs; breadth decent), and Friday’s broad snap‑back helps. But short‑term momentum is warm, volatility is compressed, and pro exposure is already high while seasonality turns less friendly. Netting those, the risk/reward into next week looks Neutral: tactically favor pullback buys above the 20‑DMA and fade crowded breakouts if internals (breadth/AD lines) fail to confirm. Keep an eye on small‑cap follow‑through and whether equal‑weight leadership persists; both would upgrade the signal; a quick VIX spike and breadth roll‑over would downgrade it.

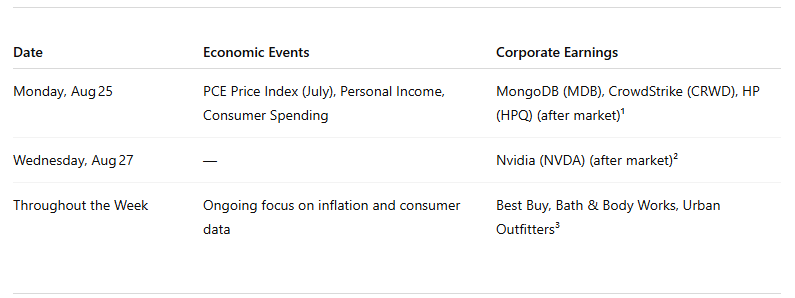

🔑 Key Catalysts Next Week

Next week’s calendar could test the durability of the post-Jackson Hole market rally. The Fed’s preferred inflation gauge, the July PCE price index, is set for release alongside data on personal income and consumer spending. These figures will help shape expectations for the September FOMC meeting. On the earnings side, Nvidia reports midweek, with investors looking for signs of continued AI-driven growth. Reports from MongoDB, CrowdStrike, and HP will also offer insight into tech sector momentum. Retail names like Best Buy, Bath & Body Works, and Urban Outfitters will give a read on discretionary spending trends.

Overall Risk Outlook: Neutral

The short-term outlook leans neutral, but with a bullish bias if key data confirms a soft-landing narrative. Markets are coming off a strong rebound driven by Powell’s dovish tone at Jackson Hole. His signal that the Fed may ease if labor market risks rise gave investors a reason to buy back into risk assets. That optimism now hinges on incoming data. Investors should stay alert. The bias is bullish, but a neutral posture is warranted unless data aligns with dovish policy expectations.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

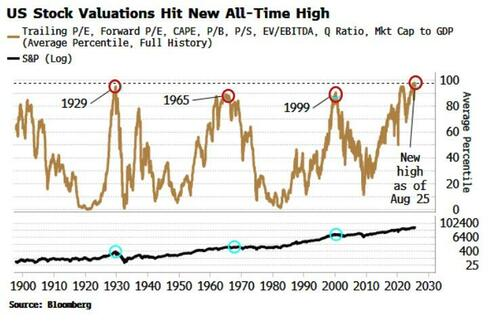

💰 Market Valuations Don’t Matter, Until They Do

One of the hallmarks of very late-stage bull market cycles is the inevitable bashing of long-term market valuation metrics. In the late 90s, if you were buying shares of Berkshire Hathaway, it was mocked as “driving Dad’s old Pontiac.” In 2007, valuation metrics were dismissed because the markets were flush with liquidity, low interest rates, and “Subprime was contained.”

“Valuation is the capstone of proximate causes for a market top, and the one most indicative of the potential magnitude of any subsequent selloff. It’s well known that valuations are high for the US market, but I thought I’d update my aggregate indicator, which combines the main measures of long-term stock-market worth. It previously peaked in April, but has just made a new all-time high this month. Not a welcome sign if you’re a long-term bull.” – Simon White, Bloomberg

Of course, just as we have seen so many times, we again see repeated arguments about why “this time is different.” For some, it is the belief that the Fed will bail out markets if something goes wrong. For others, “Artificial Intelligence” and “Cryptocurrencies” are a new paradigm of investment returns. Of course, it is hard to blame investors for feeling this way, given the market’s outsized gains over the last 15 years.

Regardless of the reasoning, there is little argument that current trailing market valuations are elevated.

However, we need to understand two crucial points about valuations.

- Market valuations are not a catalyst for mean reversions, and;

- They are a terrible market timing tool.

Furthermore, investors often overlook the most essential aspects of valuations.

- Valuations are excellent predictors of return on 10 and 20-year periods, and;

- They are the fuel for mean-reverting events.

Critics argue that valuations have been high for quite some time, and a market reversion hasn’t occurred. However, to our point above, valuation models are not “market timing indicators.” The vast majority of analysts assume that if a measure of valuation (P/E, P/S, P/B, etc.) reaches some specific level, it means that:

- The market is about to crash, and;

- Investors should be in 100% cash.

This is incorrect.

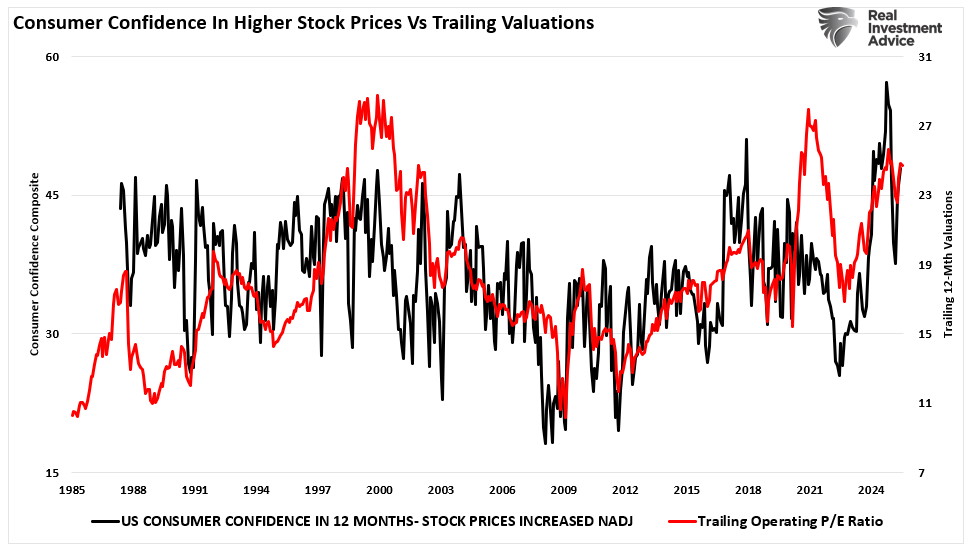

Market valuation measures are just that—a measure of current valuation. Moreover, market valuations are a much better measure of “investor psychology” and a manifestation of the “greater fool theory.” This is why a high correlation exists between one-year trailing valuations and consumer confidence in higher stock prices.

What market valuations express should be obvious. If you “overpay” for something today, the future net return will be lower than if you had paid a discount for it.

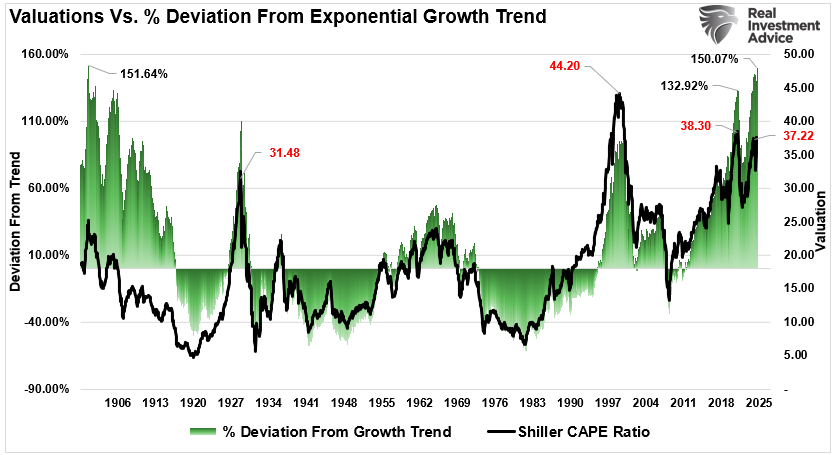

Current market valuations are not sustainable. Fundamentals, revenue growth, earnings power, free cash flow, margins, and debt govern valuation over time. This is particularly true when the vast majority of the market generates little to no earnings growth, but growth is only a function of a handful of companies.

Markets eventually will revert toward fundamentals. That process takes time, but it is both inevitable and relentless

Price‑to‑Sales and Market‑Cap‑to‑GDP Send a Warning

The Price‑to‑Sales (P/S) ratio measures how much investors pay for each dollar of a company’s sales. The S&P 500 currently trades around 3.2 times trailing sales. The long‑term average is closer to 1.6 times. For perspective, a P/S ratio above “2″ signals elevated valuations. The market P/S ratio is currently more than 2-standard deviation above its historic average.

The elevated P/S reflects bullish expectations that when you pay over $3 per $1 of sales, you expect future growth to justify it. That means investors expect strong revenue gains ahead. But if growth slows, valuations must adjust downward. In other words, the market is currently “priced for perfection,“ which leaves a lot of room for disappointment.

Another measure is Market‑Cap‑to‑GDP, known as the Buffett indicator. This measure compares total stock market value to national output. Given that earnings and revenue growth come from economic activity, the market valuation should represent the strength of the overall economy. Currently, that measure of market valuation resides at 217%. Notably, the long‑term average is around 155%. At current levels, valuations are well above what the economy can generate, and two standard deviations above the long-term trend.

That signals broad market overvaluation versus economic size. It suggests prices may be disconnected from the real economy that generates earnings.

Both metrics send a clear message: valuations exceed long‑term norms. That means excess return potential is limited. Downside risk rises if sentiment shifts or fundamentals falter.

These high valuations can be sustained longer than expected if sentiment remains jubilant. But you cannot ignore the math. Expectations already baked into the price are high. Therefore, you must realize that you tolerate a limited margin of safety unless fundamentals outperform.

Valuation Exuberance Increases The Overall Risk Profile

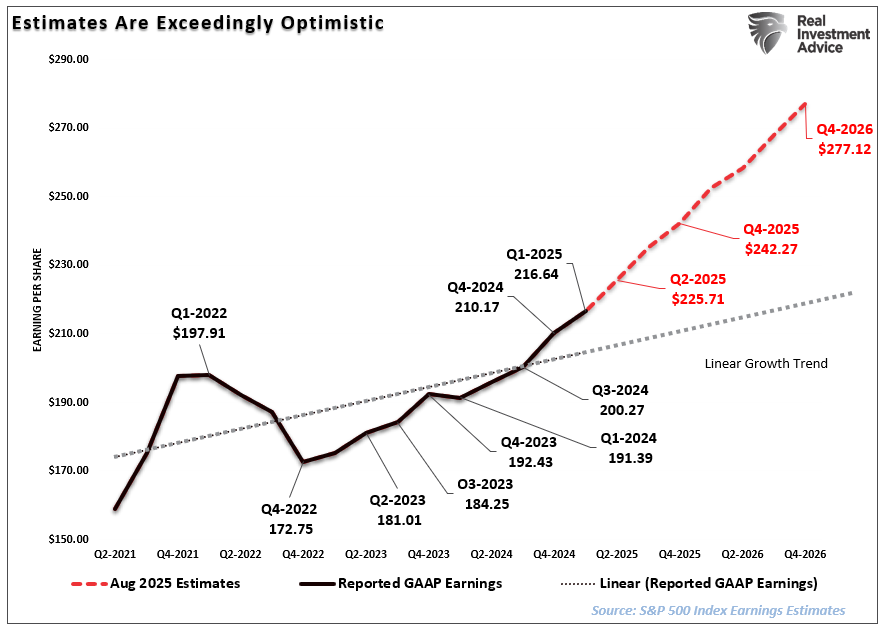

Still, the current level of exuberance is unsurprising given the strongly trending bull market, particularly when Wall Street needs to justify higher valuations. The problem is that such exuberant forecasts rarely come to fruition. For example, in March 2023, S&P Global predicted that 2024 earnings would grow by 13% for the year. In reality, earnings grew by just 9% despite the market rising nearly 28%. In other words, given that actual earnings fell well short of previous estimates, the 2024 market was primarily driven by valuation expansion.

Current earnings projections for 2025 suggest a nearly 20% increase, well above historical growth trends. While such detachments of the market from earnings are not uncommon, they tend not to be sustainable over more extended periods. We suspect that the risk to stocks in 2025 will be a failure of earnings to meet optimistic expectations.

When sentiment and expectations exceed economic realities, there is the potential for stock repricing. As noted, “stocks are priced for perfection,” which means any shortfall could lead to a more substantial decline in price. For instance, the S&P 500’s P/E ratio has reached levels that some analysts consider concerning, reflecting investor optimism that may not align with underlying economic fundamentals.

Given the interdependence between earnings and economic growth, valuations present a more serious challenge. A better way to visualize this data is to look at the correlation between the annual change in earnings growth and inflation-adjusted GDP. There are periods when earnings deviate from underlying economic activity. However, those periods are due to pre- or post-recession earnings fluctuations. Currently, economic and earnings growth are very close to the long-term correlation.

It is worth repeating that valuations are unreliable market-timing tools. Elevated valuations reflect heightened investor optimism and expectations of robust earnings growth in bull markets and can remain that way for extended periods.

However, excess market valuations leave investors vulnerable to unexpected, exogenous events. Those “events,” when they occur, lead to sharp sentiment reversals. What would cause such a sentiment reversal? No one knows. This is why when the “unexpected” happens, Wall Street’s immediate response is to suggest that “no one could have seen that coming.”

As such, investors must continue managing risk into 2025 and navigate the markets accordingly.

📒 Portfolio Tactics – Investing During High Valuation Periods

High valuations hurt long‑term returns. Elevated P/S and market‑cap‑to‑GDP ratios reduce future upside. They increase downside risk if sentiment reverses. You still can participate. You still can protect.

Consider these tactics as you consider your current exposure.

- Trim exposure at stretched multiples: When forward P/E tops 22 or P/S surpasses 3.2×, scale back positions. Take profit. Lock gains while fundamentals remain intact.

- Add value sectors: Move into energy and healthcare. These sectors often trade at lower multiples and typically offer more substantial dividends. They may provide defensive ballast.

- Hold cash or short‑duration bonds: Preserve optionality. Limit risk from pullbacks. You stay in the game without full exposure.

- Rotate to international and small‑cap value: U.S. valuations are richly priced. Value opportunities may exist overseas or in small companies. That offers diversification and lower price risk.

- Employ hedges or protective strategies: Covered calls, tail hedges, and partial inverse ETFs can provide downside support when sentiment peaks.

- Rebalance using valuation-based rules: Set thresholds for P/S and market-cap‑to‑GDP. When these thresholds are breached, allocate to defensive assets. This maintains discipline.

- Watch fundamentals closely: Track earnings yield versus bond yield, free cash flow margins, and interest coverage. If fundamental health deteriorates, reduce exposure further. Let data guide your moves.

These tactics let you ride the rally. They also protect when sentiment fades. They give you balance while participating with caution.

Trade accordingly.

🖊️ From Lance’s Desk

This week’s #MacroView blog delves into the recent slate of weakening economic data and why it suggests there is risk to the more optimistic outlook for earnings by investors.

Also Posted This Week:

📹 Watch & Listen

Bitcoin has a very high correlation to the Nasdaq and the S&P 500. What can we learn about navigating market risk from cryptocurrencies?

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

📊 Market Statistics & Analysis

Weekly technical overview across key sectors, risk indicators, and market internals

💸 Market & Sector X-Ray: Overbought

Last week, we warned investors to be mindful of the technical deterioration, which led to a sell-off early in the week. However, Friday’s surge toward all-time highs sent most markets and sectors back to extreme overbought conditions. While exuberance may feed over into next week, we recommend using any further gains to reduce overbought positions, trim out weak positions, and rebalance overall risk.

📐 Technical Composite: 86.64 – Very Overbought

Despite the market weakness early in the week, the sharp rally on Friday pushed the majority of technical indicators back to weekly overbought conditions. While the correction to the 20-DMA was healthy, it failed to reverse conditions for a more sustainable rally.

🤑 Fear/Greed Index: 74.79 – Greed Increases With Rally

Despite the early week correction, the market rally on Friday kept the fear/greed gauge near extreme greed levels, rising from 71.22 to 74.79. While the increase was mild, it continues to suggest a more aggressive posture by investors in the markets, which keeps a larger corrective process from occurring. In other words, investors continue to aggressively “buy dips.”

🔁 Relative Sector Performance

Last week, we noted:

“That rotation began this past week, with Healthcare performing well, along with Financials and Discretionary. Technology showed some signs of weakness as money rotated to more fundamentally based sectors. Keep a watch on Real Estate and Energy, which are very oversold and out of favor. The next chart shows some energy names to watch.”

The weakness continued early this week, with healthcare moving sharply higher. Real estate also performed well, and money sought more defensive positioning amid the technology sector slide. The good news is that technology is now oversold, which caught a decent rotation trade back into those key names, as shown in the next chart, on Friday.

📊 Most Oversold Sectors

As noted above, Technology is now the most oversold sector, and on Friday, money returned to names like AVGO, PLTR, and NVDA.

📊 Sector Model & Risk Ranges

The early-week correction failed to reverse the market’s more overbought conditions. Notably, the Friday rally pushed numerous sectors and markets well above the monthly risk ranges, suggesting that further upside is likely limited until there is a bit of a reset. The sectors with double-digit deviations from their long-term means are at the most significant risk of corrective action. Take profits in those sectors and look to rotate to more oversold areas of the market.

Have a great week.

Lance Roberts, CIO, RIA Advisors

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)