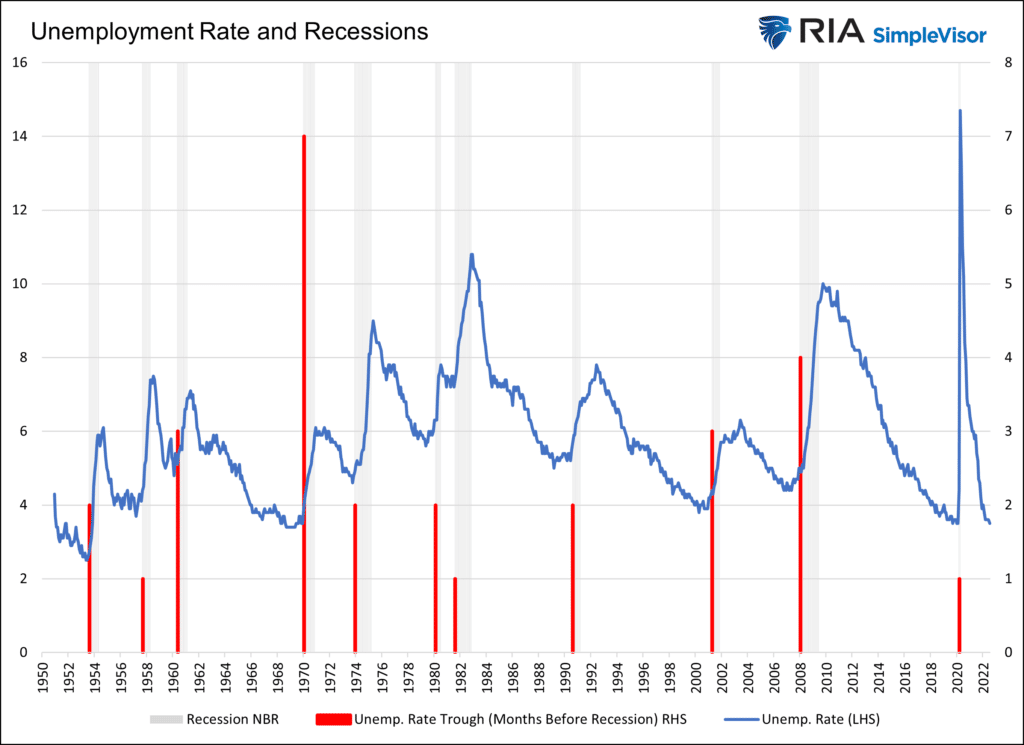

The economy added 528k jobs in July, almost 300k more than expected. With the much stronger-than-expected jobs report, the odds of an official NBER recession proclamation fade. The NBER considers both GDP and employment before deeming a period of economic weakness a recession. The graph below shows that, on average, NBER recessions start about two to three months after the unemployment rate starts ticking higher. The July 3.5% unemployment rate fell .1% from last month and is the lowest in fifty years. Arguing further that NBER recession odds are falling is labor market strength throughout the report. The prior two months were revised higher by 28k. Also encouraging, average hourly earnings rose more than expected (5.2% vs. 4.9% year over year); however, they remain well below inflation rates. The only fly in the ointment is that the participation rate continues to fall and remains about 1% below pre-pandemic levels.

What To Watch Today

Economy

- No notable reports are scheduled for release.

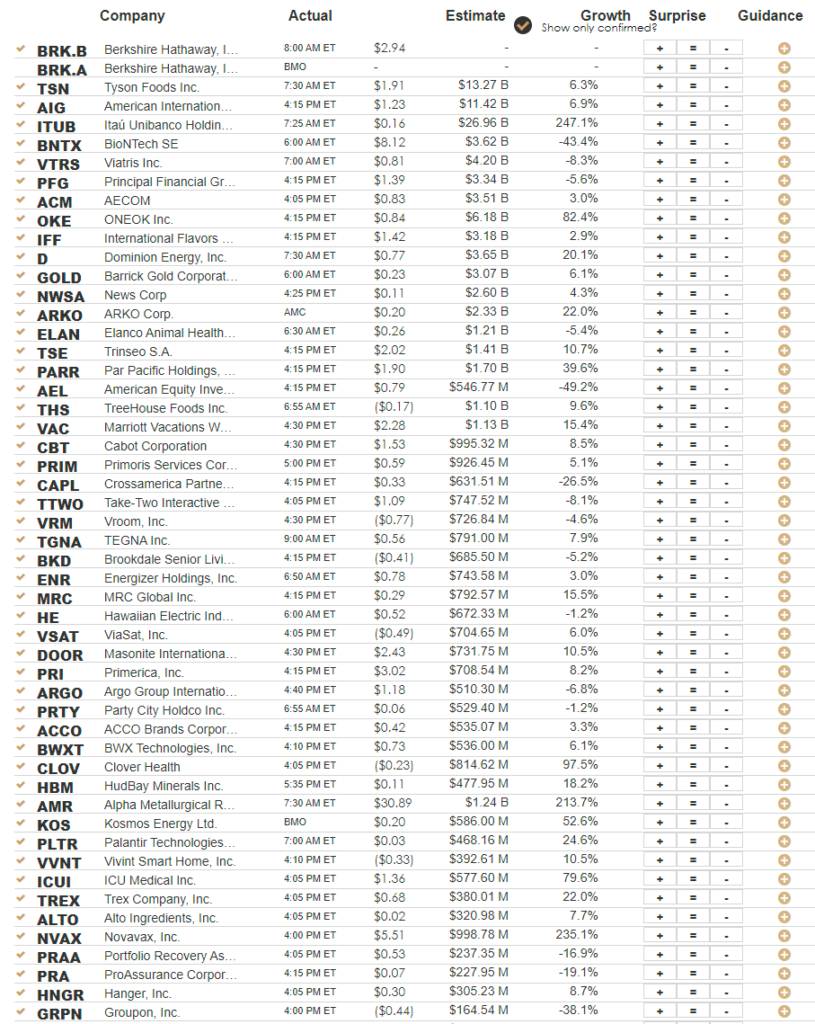

Earnings

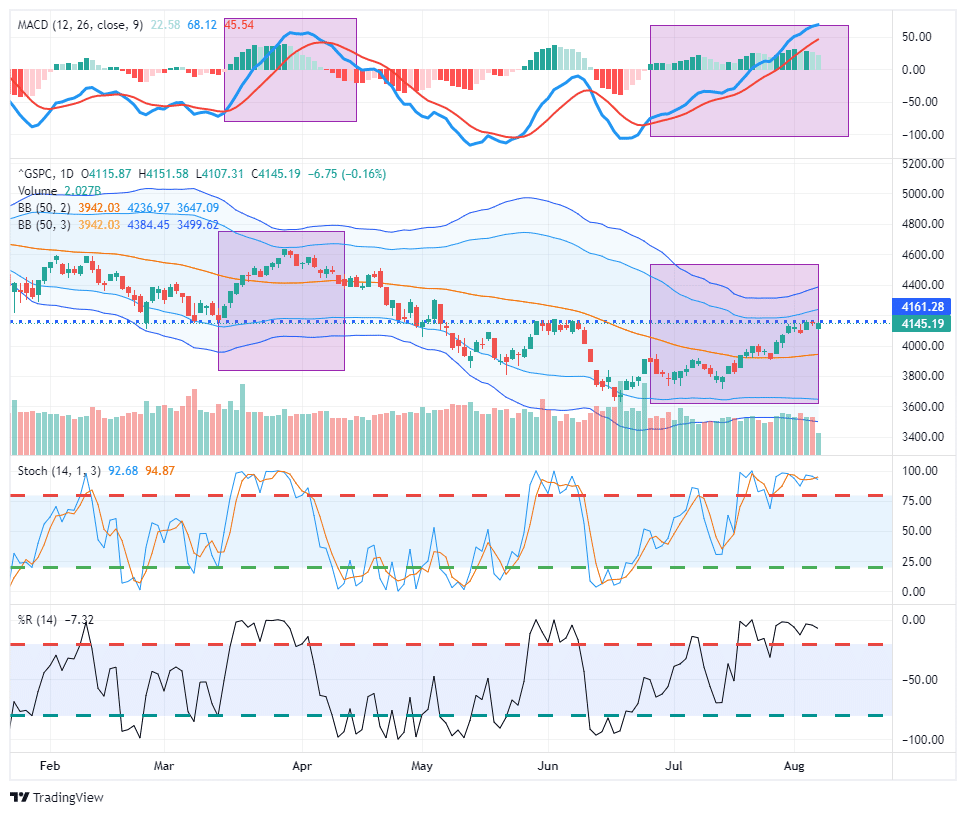

Market Trading Update

Following the recent Fed rate hikes and some “better than expected” economic data, the market surged this week. The rally is not surprising given the extremely negative sentiment and positioning in the markets in June. As we noted then, such extreme negative sentiment is a “contrarian” indicator and provides the fuel for a market rally. Such was the case, much like we saw in March this year.

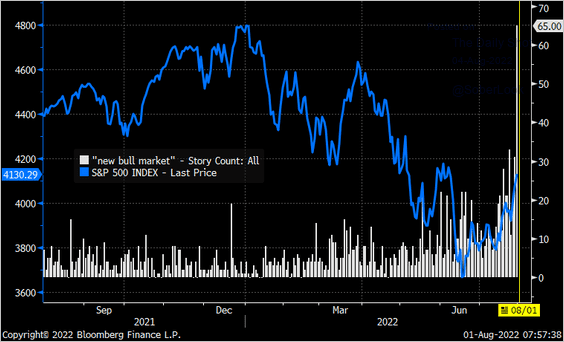

Despite the Fed hiking rates, shrinking their balance sheet, and inflation at 9%, much of the financial media and market gurus have determined that the bear market is over and a new bull market has started. As shown, as the market surged, so did the number of articles discussing a new bull market.

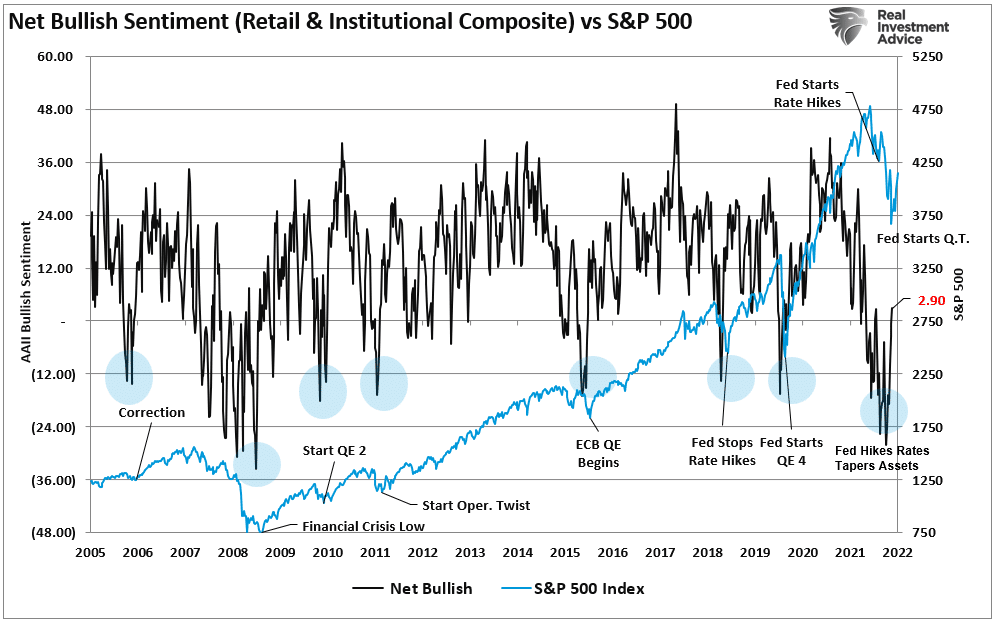

The previous extreme pessimism levels formed the perfect foundation for a strong bull market rally. Notably, those more extreme levels of bearishness are rapidly turning bullish. The chart below is a composite of both professional and retail investor sentiment.

Bull Rally Has Some Legs

The question becomes sustainability. To that end, some indicators currently support the view of a more sustainable bull market. To wit:

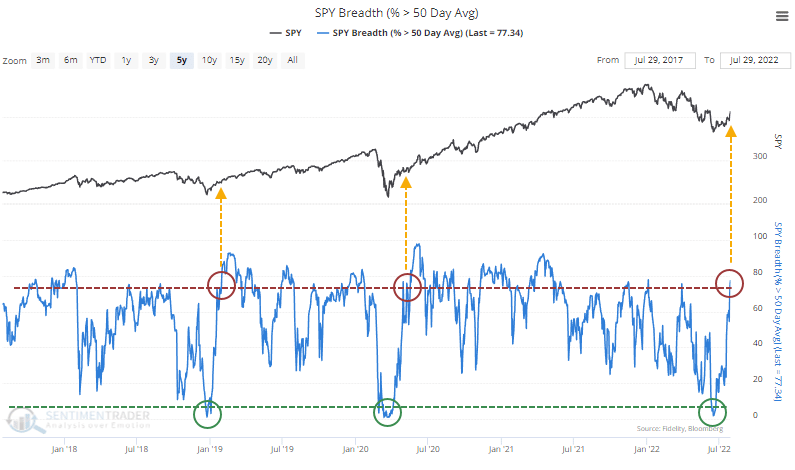

“With a continued rise last week, more than three out of every four stocks in the index recovered above their 50-day moving averages, the most since the beginning of the year. The other two times in the past five years, when this cycled from fewer than 5% of stocks to more than 75%, it coincided with the kick-off to sustained rises.” – Sentiment Trader

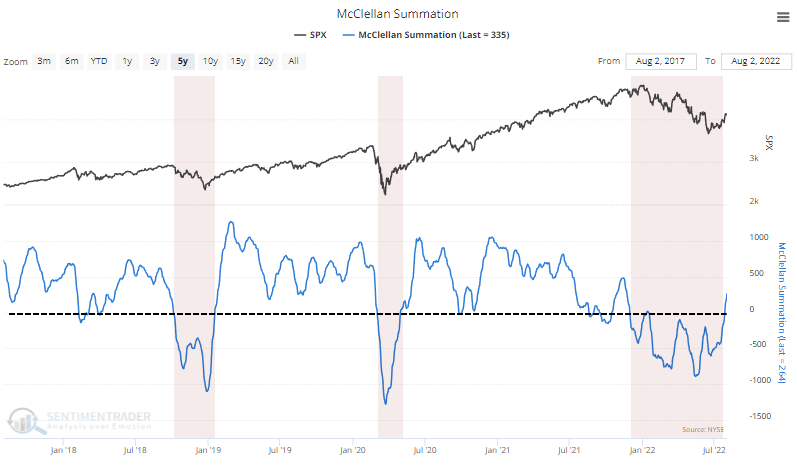

Furthermore, the McClellan Summation Index is also denoting a more healthy market which has historically led to more gains.

As Sentiment Trader concludes:

“The setup was ripe for at least a bear market rally in late June. Sentiment was about as bad as it gets, for as long as it gets before dip-buyers tend to step in. And they did, aggressively. That triggered some thrust-y signals a month ago, and unlike others over the past six months, buyers persisted and triggered even more compelling signals. It’s another sign that this recovery should have legs.”

We agree this market surge could have some legs as the short- to intermediate-term time frame is bullish and does warrant increased equity exposure. However, such does not mean there won’t be some pullbacks along the way, as the market is very overbought short-term. Such pullbacks will provide opportunities to increase exposure.

The Week Ahead

The economic fireworks start on Wednesday when the BLS releases July CPI data. Expectations are for year-over-year inflation to remain at 9.1%. To do so, the monthly rate needs to be +.45%. If it’s higher, the year-over-year rate will increase, and vice versa if it’s lower than .45%. Three of the last four months were 1% or higher. PPI follows on Thursday. Given the recent declines in many commodity prices, analysts expect a decrease from 11.3% to 10.9%, with a meager .2% monthly increase. The University of Michigan Consumer Sentiment Survey will help us gauge consumer price expectations. Last month, the five-year expected inflation rate fell from 3.1% to 2.9%.

We suspect a large number of Fed speakers will be on the speaking circuit again this week. Given the strong employment report and a slight uptick in economic data, they will likely continue to bemoan inflation and remain very hawkish. It’s hard to believe any Fed members will mention the words “stall” or “pivot.” The Fed’s annual Jackson Hole conference will occur from August 25-27. The Fed often uses this conference to announce changes to their policies or current thinking around the economy or inflation. Some Fed members may provide a preview of things to expect from the conference.

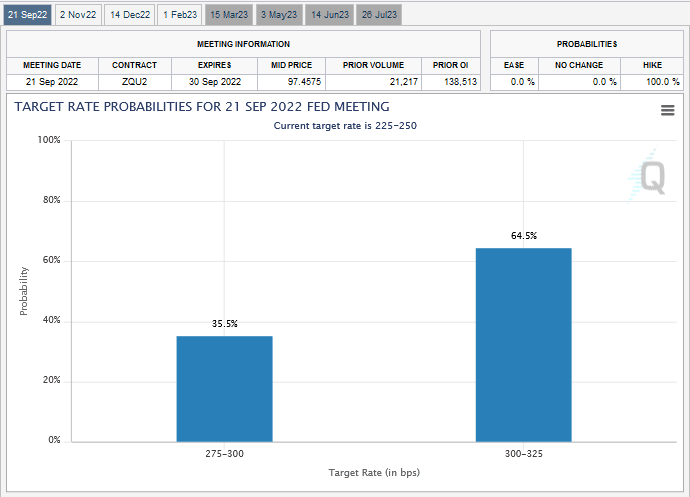

Will The Fed Hike By 75bps?

The strong jobs report and diminishing odds the NBER calls a recession soon are prompting Fed Funds traders to price back the odds of the Fed hiking by 75bps at the coming September meeting. As we show below, the Fed Funds futures markets now imply a two-thirds chance of the Fed raising rates by .75%. It was as low as .25% a few days ago.

Refinery Shut Capacity Keeps Upward Pressure on Gas Prices

The page below is from Exxon’s latest earnings release. It shows that global refining capacity increased from 2017 to the eve of the pandemic. Since then, refining capacity has been declining. Per Exxon, more than three million barrels per day (Mbd) of capacity have been shut down since 2020. The bright side is they expect about one Mbd per year to come back online over the next two years. As we have noted, crack spreads remain stubbornly high, which is one reason gasoline prices remain higher than they would have been in the past. Bringing refineries back to full capacity will help the problem in the short run. The bigger question for the next decade is will energy companies build new refineries as global warming protocols and regulations weigh on their economic viability.

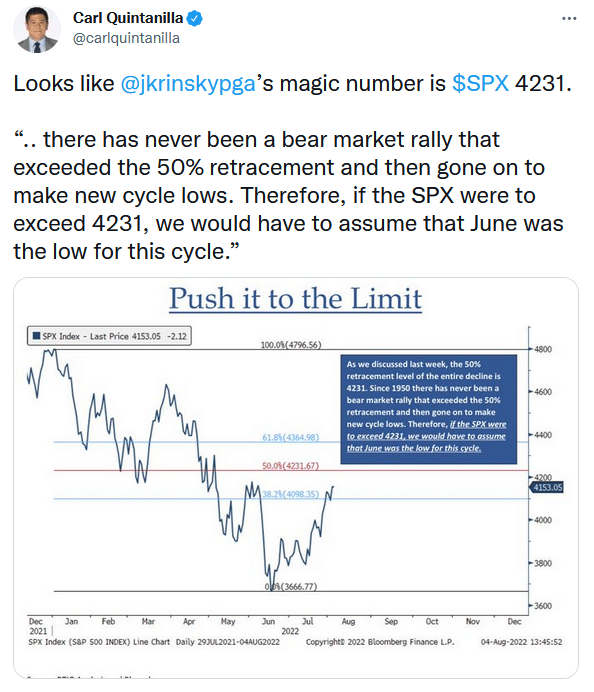

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.