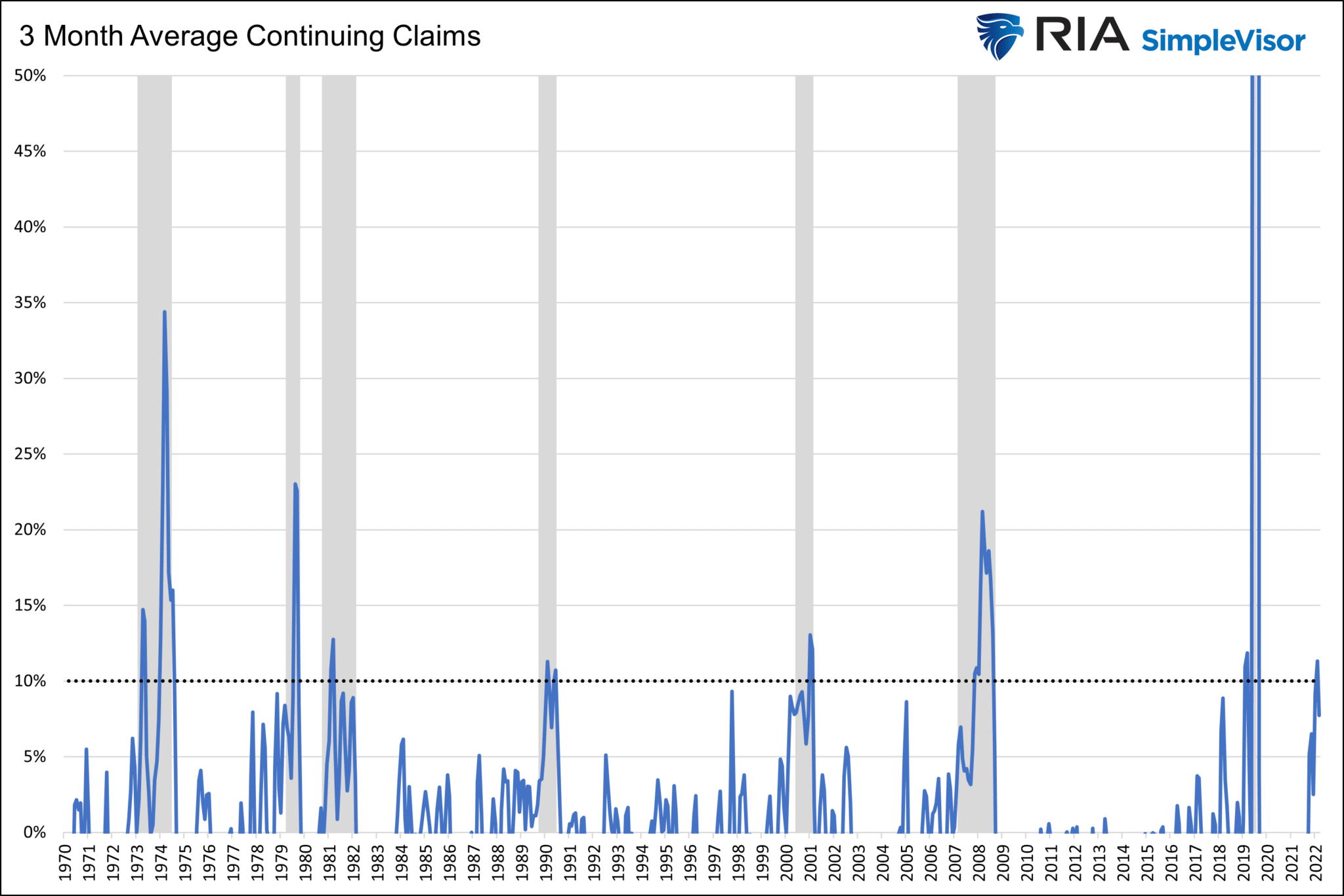

The key takeaway from Wednesday’s FOMC meeting: despite encouraging inflation news, the Fed believes they have a long inflation fight ahead. Central to the Fed’s outlook is the extremely tight labor market. The best source of real-time employment data, initial jobless claims, fell this past week and resides at very low levels. As we share below, continuing jobless claims are rising, but they are only half the average rate of the last ten years. The New York Empire State Manufacturing Index affirms the Fed’s concerns. While the broad index fell in December, the components used to gauge future inflation rose. For example, prices paid were flat versus last month, but the percentage of those surveyed reporting lower prices fell to 0%. Regarding labor, the number of employees index rose.

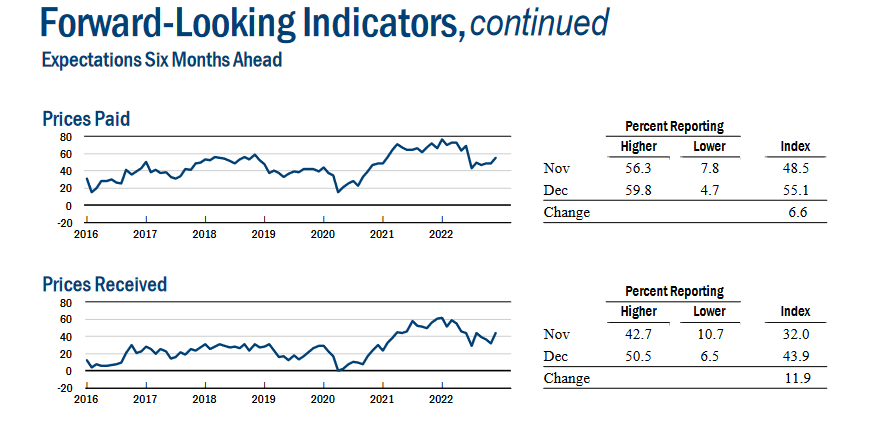

Within the New York survey are forward-looking indicators. An increasing number of manufacturers in the New York region think prices will be higher in six months. Further, a decreasing number of respondents believe they will be lower. The Fed deeply values inflation expectations. The New York survey and relatively solid labor markets affirm the inflation fight is far from over.

What To Watch Today

Economy

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, December Preliminary (46.9 expected, 46.4 prior)

- 9:45 a.m. ET: S&P Global U.S. Services PMI, December Preliminary (47.8 expected, 47.7 prior)

- 9:45 a.m. ET: S&P Global U.S. Composite PMI, December Preliminary (46.5 expected, 46.2 prior)

Earnings

Market Trading Update

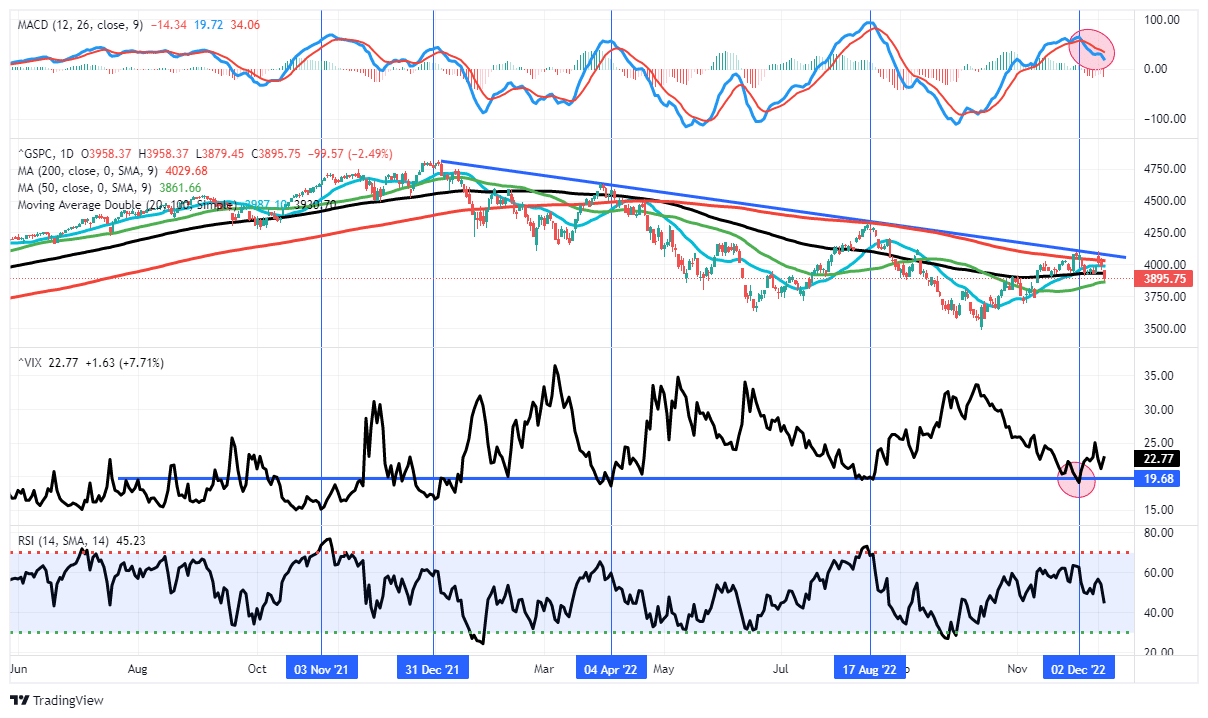

A more hawkish than expected Fed led to a sharp selloff on Thursday. Such was not unexpected, as noted in yesterday’s commentary. However, the market broke the recent month-long trading range to the downside and took out the critical support at the 100-DMA. A test of the 50-DMA is next, with little support below that until a retest of previous lows.

While the best two weeks of the year kick off on Monday, there is no guarantee that “Santa Will Visit Broad & Wall.” We suggest remaining cautious for now until the market finds some level of support to hold. The good news is that the market is oversold on a very short-term basis. However, the MACD sell signal remains intact, suggesting that any upward moves will likely be met with sellers.

Caution remains advised.

Retail Sales Point to Weak Holiday Sales

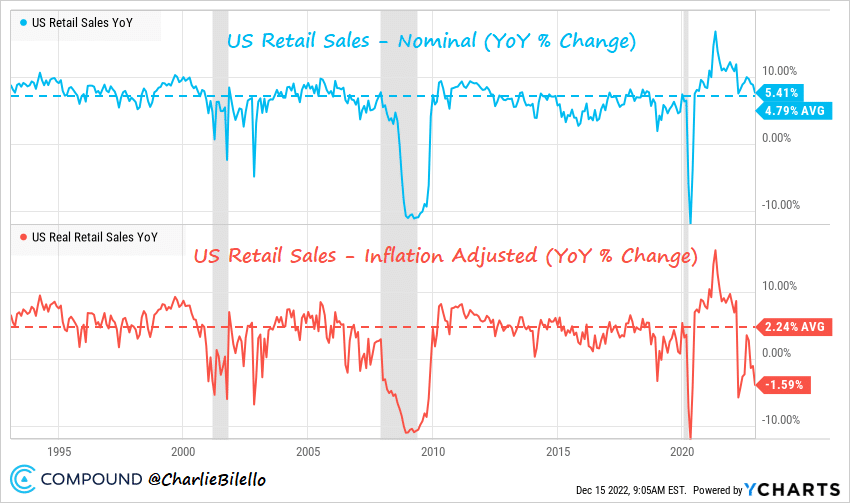

November retail sales were weaker than expected at -.6% and well below October’s +1.3%. We remind you this data is not adjusted for inflation. Therefore, consumers in November spent less and are getting even less for their money. Thursday’s print is the lowest negative reading since mid-summer. Leading the decline were furniture, building materials, and autos. The data affirm credit card data from Black Friday and Cyber Monday. Retail data is seasonally adjusted. Given the many factors that affect holiday shopping and deviations from year to year, we must take the weakness with a grain of salt. However, a recession becomes more likely if the trend continues in December and January. Consumers account for two-thirds of the GDP.

Labor Markets Matter Most to Powell

Rereading the transcript from Wednesday’s FOMC press conference, it becomes even clearer Jerome Powell thinks he must weaken the labor markets to get inflation to 2%. Bob Elliot shares some advice in this regard. To wit:

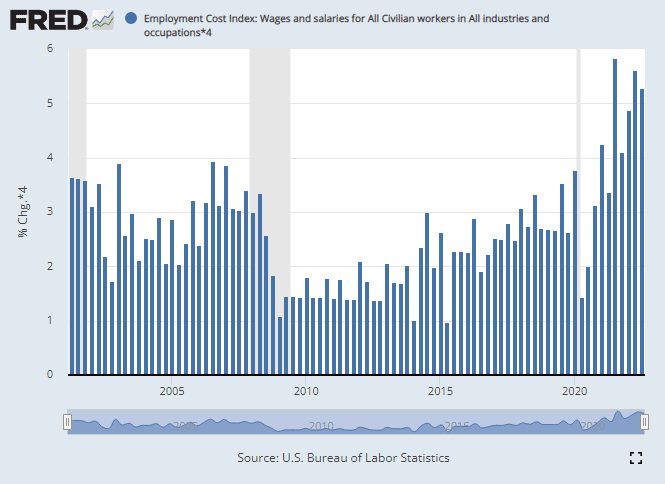

Don’t focus on the nuances of the CPI report. Its much more valuable / less noisy to focus on incomes. That’s because in any economy nominal income vs. output determines the structural inflation rate. Most stats show US incomes are growing pretty consistently at 5-6%.

To summarize, as goes wages goes inflation. Wage growth is still climbing.

Continuing Jobless Claims, one of the few near real-time official labor reports, tends to be early to show labor weakness. Per the second graph, it is increasing at a 7% quarterly rate. While the rate of change is picking up decently, the total number of continuing claims is only half the average since 2000.

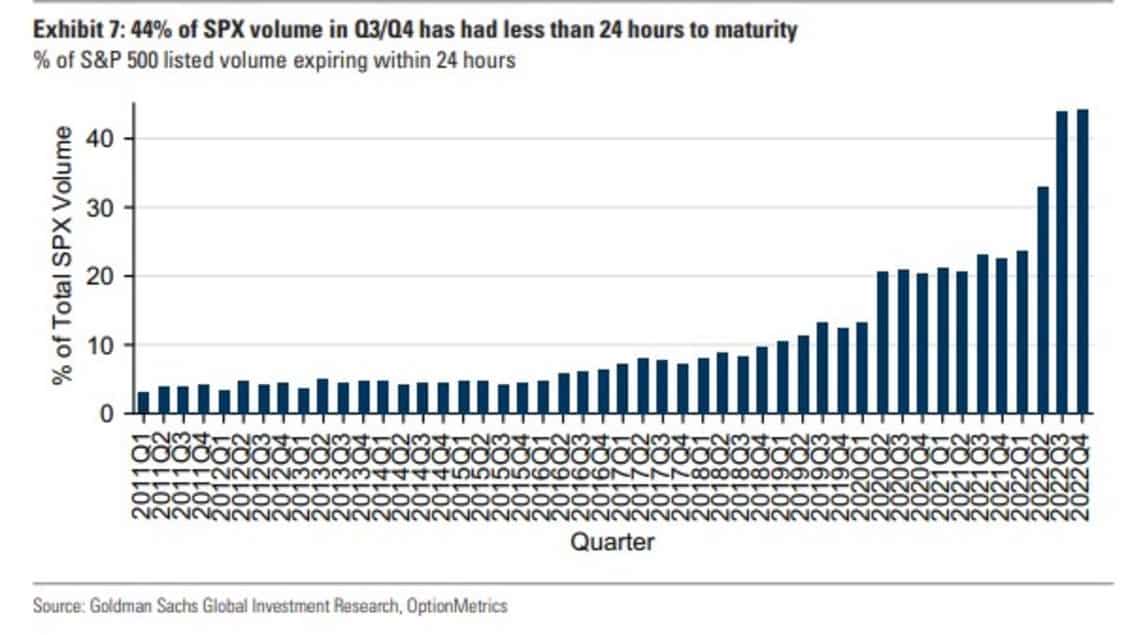

S&P Casino

The following graph helps explain why stocks were up over 3% on the CPI report yet erased most of the gain by the close. Almost half of the volume on S&P 500 options is occurring in options that expire in less than a day. Given the extremely short time frame of said option trades, these are binary, roulette-like bets on the markets. Importantly they are bets on how the market immediately reacts to an important piece of economic data, a Fed speech, or another known market-moving event.

Wall Street dealers often take the other side of options trades. Unlike most investors, dealers aggressively hedge their options book. Therefore, dealers execute trades that can accentuate short-term trends when a market moves powerfully in one direction. The takeaway, don’t to get hoodwinked by large market moves. Focus on longer-term technicals and fundamentals dictating the broader market trends.

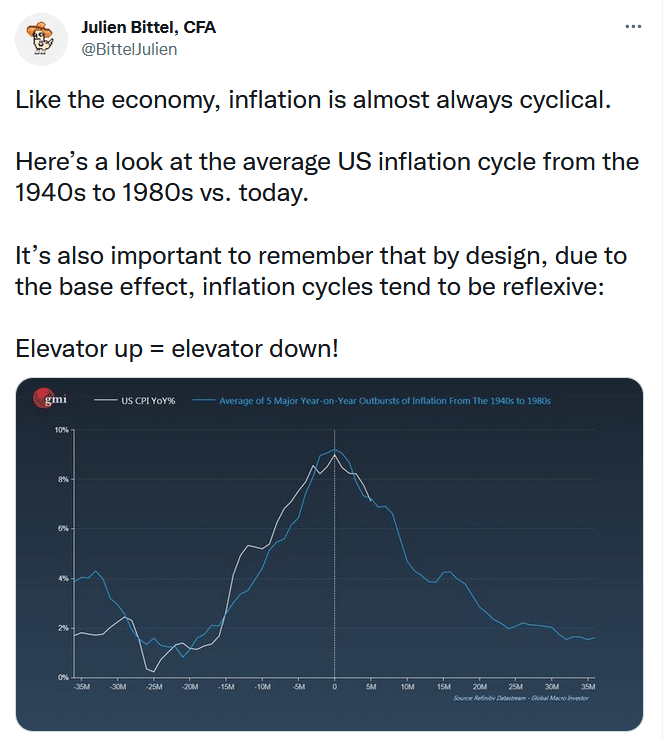

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.