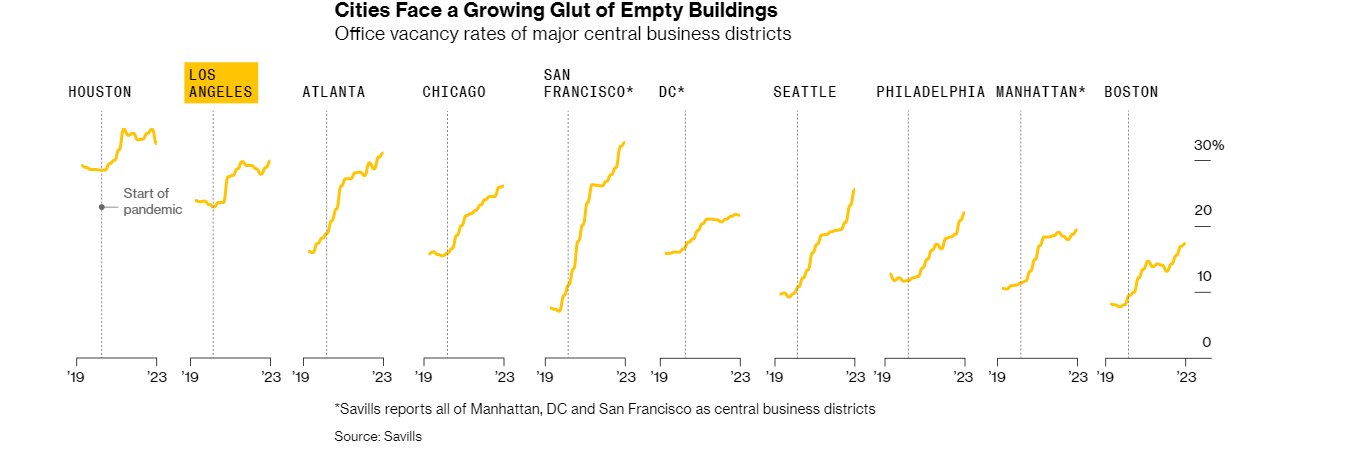

Exceedingly low-interest rates spurred a boom in office construction in the decade following the financial crisis. From 2014 through 2019, construction spending for office space grew on average by 15.6% annually, per the St. Louis Fed. That rate is about five times the rate of economic growth. Before the pandemic, the growing amount of office space was largely absorbed. However, the work-from-home revolution fueled by the pandemic results in growing office vacancy rates nationwide. The graph below, courtesy of Savills, shows that office vacancy rates in the nation’s central business districts are rising. In some cities, almost a third of office space is vacant. The national average for all office space is nearly 16.7%.

The upward trend in office vacancy rates and consequent problems for holders of commercial office properties are likely to persist. For starters, the occupancy rate is purportedly much higher than vacancy rates. As a result, companies with leases coming up for renewal may opt for less space. Second, most office space debt has floating rate terms, often three to seven years. As those rates reset, the owner must refinance at higher interest rates. Raising rents to offset the higher interest rates will prove challenging in many instances due to the glut of space available. As such, profit margins will likely decline for many property holders. Consequently, we will continue to see rising defaults. It is estimated about $400 billion of said debt will mature through 2025.

So who is on the hook if vacancy continues to rise office property owners default? Banks hold the mortgages on about 55% of the debt. Insurance companies have another 15%, and about 10% is in the hands of investors via securitization. REITs, Pension Funds, and many others own the remainder of the debt.

What To Watch Today

Earnings

- No notable releases today

Economy

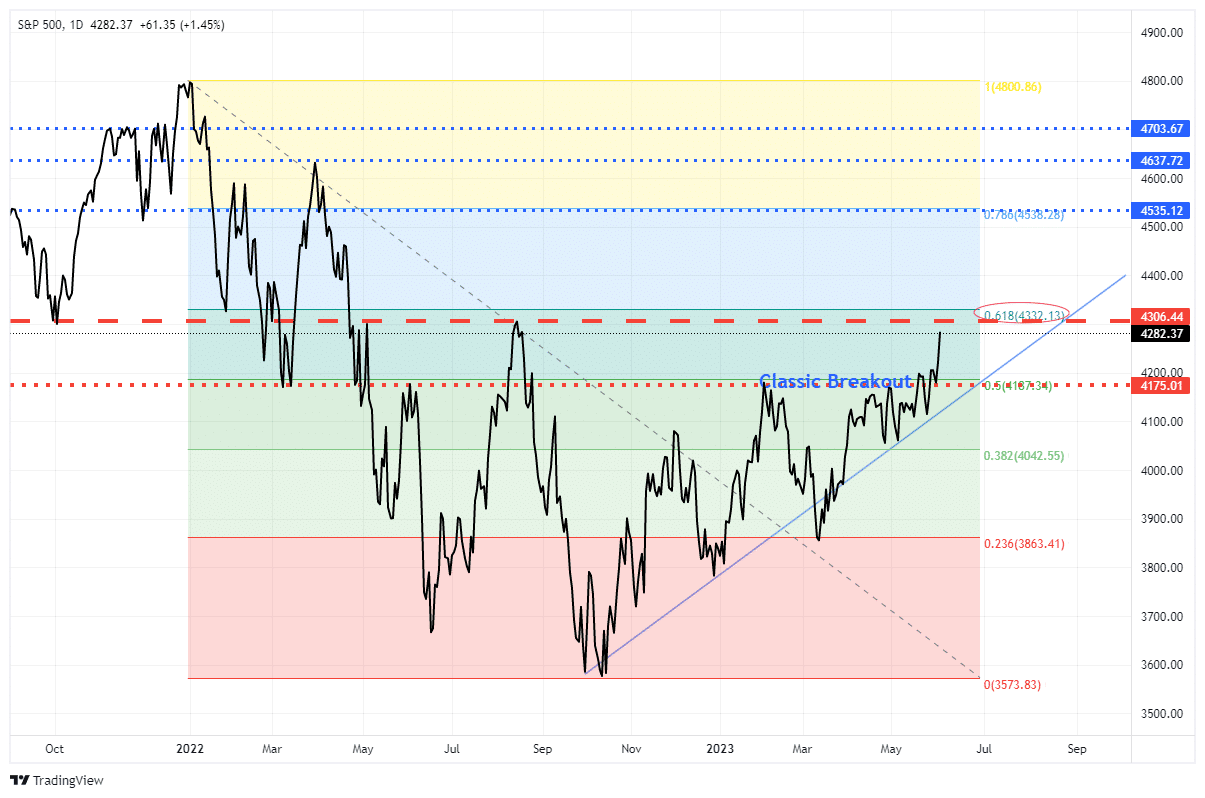

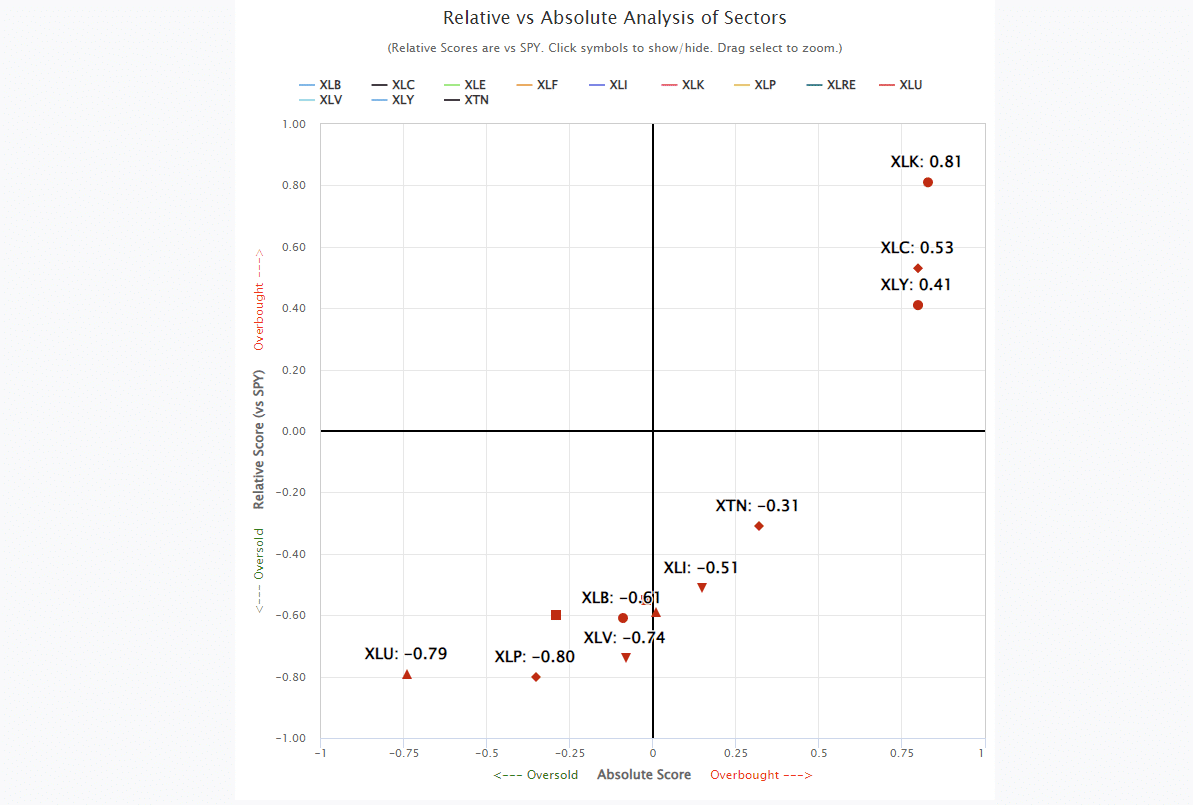

Market Trading Update

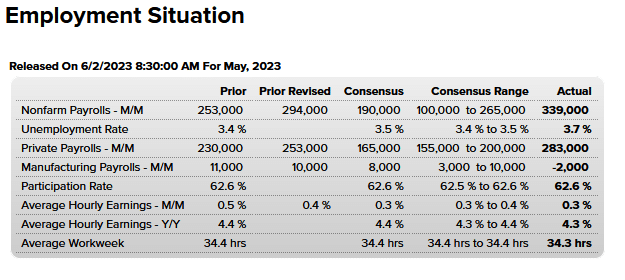

Friday’s employment report was another upside shocker, with 339,000 jobs created. There is no evidence of a near-term recession, but the robust employment number also pushes out any potential for a Fed rate cut. While such should have been read as a bearish note, stocks rallied sharply out of the gate on Friday, pushing the S&P 500 above its previous resistance level and setting a new high in this rally from the October lows. As noted last week:

“This breakout is very bullish for two reasons. First, the market has completed a 50% retracement of the 2022 decline, which sets the stage for a further advance. Secondly, the breakout confirms the bullish trend that started from the October lows. While many reasons exist to bearish, the market suggests those concerns are misplaced for now.

The next resistance level for the market is the 61.8% Fibonacci retracement level at 4332 which is slightly above the July 2022 high of 4306. A break above those levels, and there is only some minor resistance to fully recovering from the 2022 decline.

The market surge on Friday pushed the market toward that initial target.

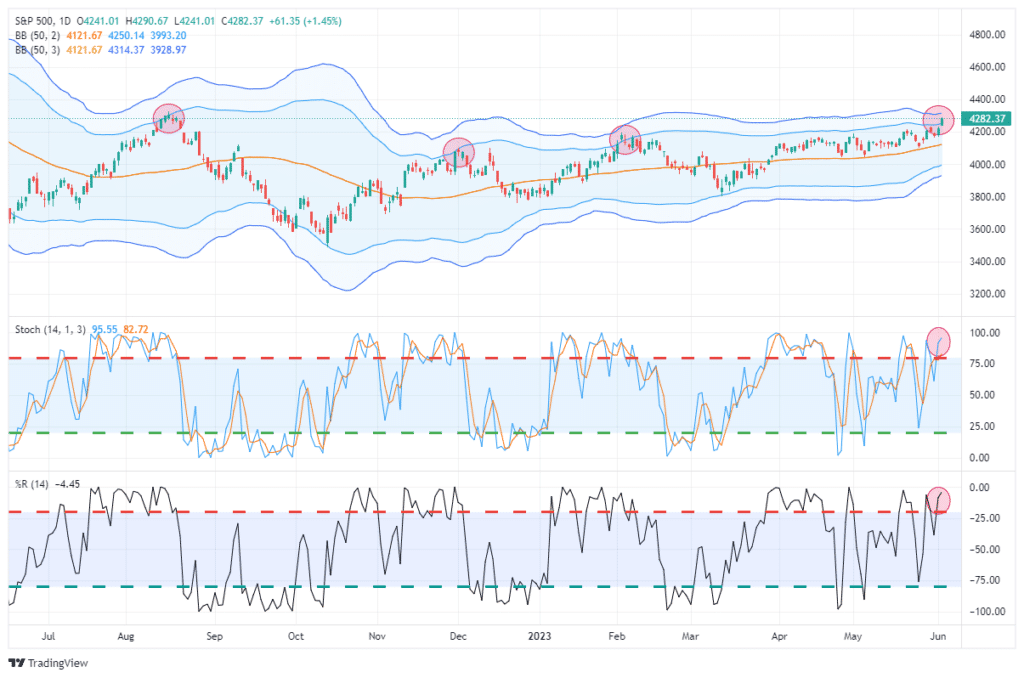

While the market advance is getting technically overbought short-term, as shown below, pullbacks to support should be used to increase exposure accordingly.

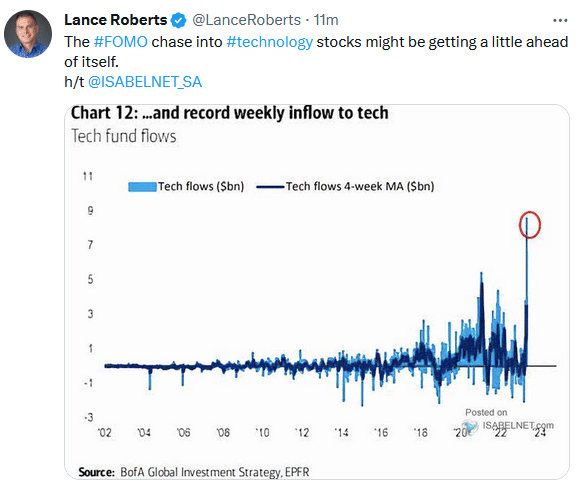

Furthermore, while the market has been chasing technology stocks lately, the market remains bifurcated between the cyclical and defensive sectors. As such, the rotation to Energy, Financials, Materials, and Staples on Friday was not surprising. The question is whether more of that rotation will come near term. Such extreme deviations in performance from the overall index tend not to last indefinitely.

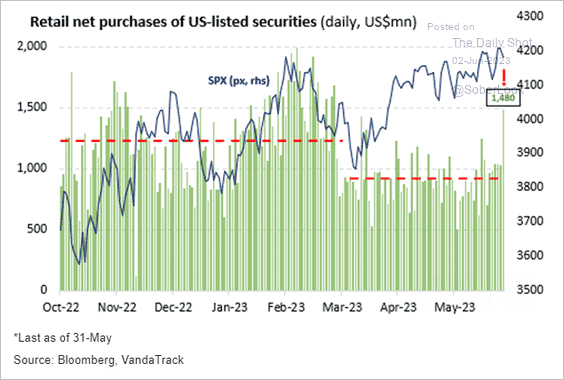

However, the current chase for stocks related to “artificial intelligence” has undoubtedly grabbed everyone’s attention. Retail investors are jumping back into the markets with both feet for the first time since last year.

The Week Ahead

There is little economic data this week, but a lot on the horizon as traders set up for CPI and the Fed meeting next week. With the debt cap extended, the Treasury will start issuing large amounts of debt. The well-followed ten and thirty-year auctions will not occur until next week. However, this morning’s three and six-month bill auctions will kick off a total of $313 billion of short-term bill issuance. Yields around 5.50% are likely to generate significant interest as the demand for short-term high-yielding assets remains robust.

Employment Remains Red Hot

The BLS reported that the economy added 339k jobs last month, well above the 190k expected. However, the unemployment rate rose by 0.3% to 3.7%. Manufacturing payrolls shrunk slightly. Such is not unexpected, given the weak sentiment readings from the manufacturing surveys. Despite the labor market strength, average hourly earnings and the average workweek were slightly less than last month.

The report’s conundrum is why the unemployment rate rose so much, given that so many new jobs were added, and considering the labor participation rate was unchanged. The 339k job growth is from the establishment survey in which they poll companies. The unemployment rate is based on the household survey in which they survey individuals. The second table below from the BLS shows that 310k jobs were lost per the household survey, and the number of unemployed rose by 440k.

So which is correct? Likely the truth lies somewhere in the middle. The surveys often differ over the short run but track each other well over extended periods. Over the last two months, the establishment survey added 804k more jobs than the household data. But, since the start of the year, the difference has been less than 100k.

With last week’s employment data in the books, the odds of a rate hike at the mid-June FOMC meeting are decent. At least one hike between the coming and July meetings looks certain. Of course, the Fed constantly reminds us they are very data-dependent. Ergo, those odds may change based on economic activity and inflation data. The Fed Funds futures market assigns a 50/50 chance of hike at either meeting and a 15% chance of two rate hikes by late July.

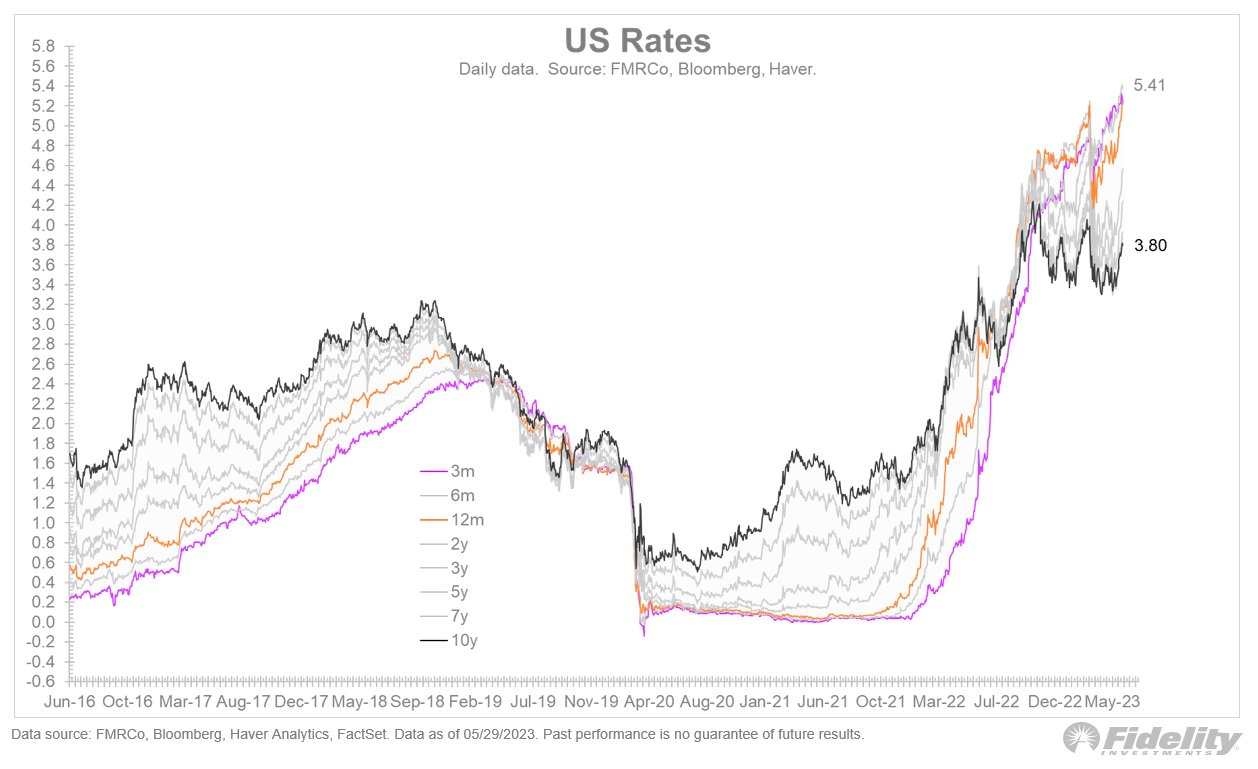

Another Look at Bond Yields

The graph below, courtesy of Fidelity, uniquely compares how the yield curve has shifted over the last year. Throughout most of 2022, long and short-term bond yields rose commensurate with inflation and the Fed’s aggressive monetary policy. However, toward the end of 2022, longer-term yields stabilized while short-term yields continued to rise, reflecting expectations that the Fed will keep hiking rates. In early November 2022, the 10-year note and 3-month bill had the same yield.

Since then, longer-term yields have declined slightly while short-term rates have continued upward. The current difference is nearly 2%. The gap represents a very restrictive policy designed to make shrink bank profit margins making it difficult for them to lend money. We suspect the gap will stay at current levels or even widen until the Fed appears close to lowering rates. That may be quite a ways off if unemployment stays low and inflation remains sticky.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 4

2023/06/05