Sarah Friar, OpenAI’s CFO, spoke at a Wall Street Journal technology conference to update the audience on the potential of AI. While her comments were very optimistic, she noted that OpenAI seeks continued capital inflows, highlighting the lynchpin for AI development. Her quote below, courtesy of Bloomberg, takes traditional bank and industry financing a step further. Notably, she mentions a role for the US government in backing or guaranteeing loans to OpenAI. Moreover, OpenAI’s need for such support underscores its burgeoning capital requirements.

In addition to OpenAI’s deals with chipmakers, the ChatGPT maker is also eying a broad mix of financing vehicles to fund its infrastructure efforts. Friar said OpenAI is “looking for an ecosystem of banks [and] private equity” to support its ambitious plans. She also hinted at a role for the US government to “backstop the guarantee that allows the financing to happen,” but did not elaborate on how this would work. – Bloomberg (LINK)

After a backlash from her remarks, she clarified her statement on LinkedIn as follows:

I want to clarify my comments earlier today. OpenAI is not seeking a government backstop for our infrastructure commitments. I used the word ‘backstop’ and it muddied the point. My point was that American strength in technology will come from both the private sector and government playing their part.

Both the original statement and her clarification make it clear that OpenAI, despite the massive fundraising effort they have already accomplished, still needs a lot more capital. OpenAI seeks additional resources to maintain its leadership role in AI. The graph below shows how OpenAI and the rest of the industry have been self-funding to meet their needs. More recently, and detailed further in this Commentary, a $30 billion bond offering by Meta and $25 billion deal by Google point to the possibility that earnings and cash flows from industry players are no longer sufficient to cover AI development costs.

What To Watch Today

Earnings

Economy

Market Trading Update

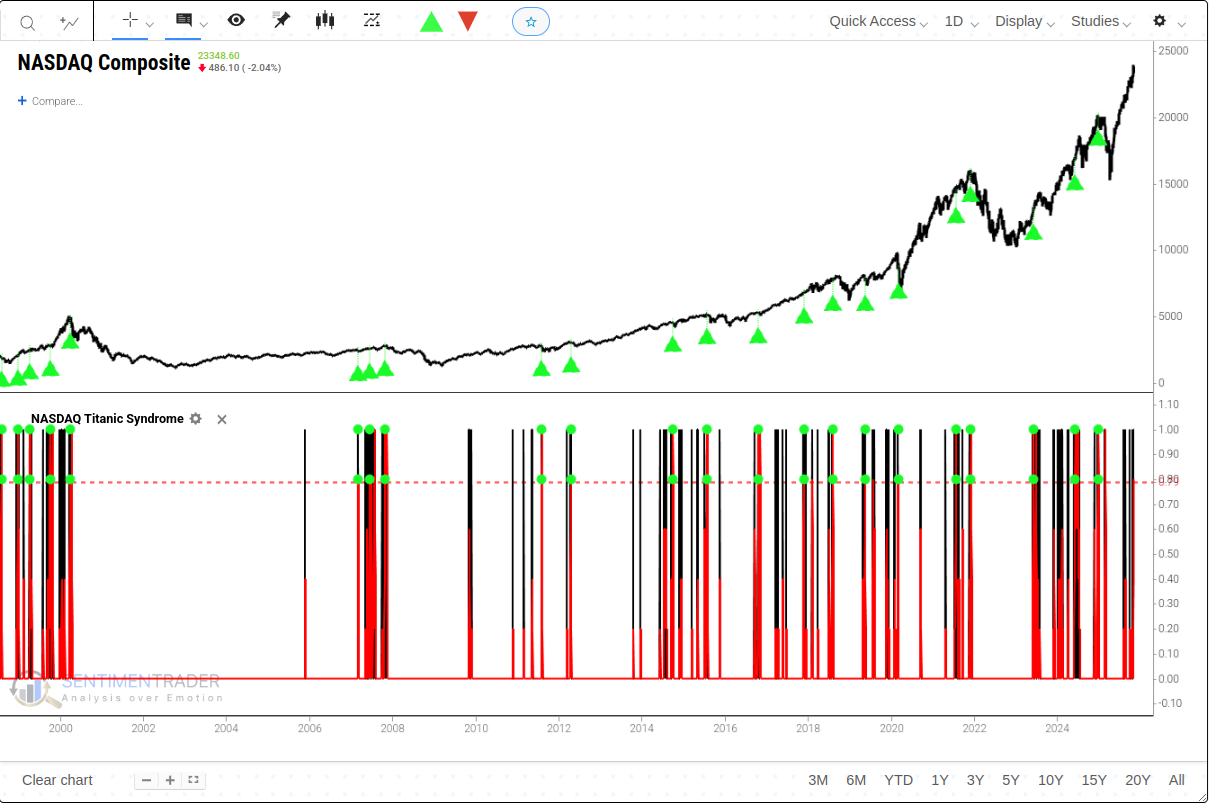

Yesterday, we discussed the bifurcation in the market between the mega-cap weighted index and the rest of the market. The “breadth” problem has been a frequent topic of discussion here lately, as the market continues to hold near highs while its internals deteriorate. Sentiment Trader had an excellent note out yesterday on the cluster of both Titanic and Hindenburg signals. (Yes, they are named after historic tragedies.)

“While the Nasdaq Composite remains near its all-time highs, the market’s internal health has shown signs of significant deterioration. This creates a potentially dangerous divergence, where the headline index is held up by a few names while broad participation crumbles.

One of the classic indicators for identifying this type of “top-heavy” market is the Nasdaq Titanic Syndrome. This signal is designed to spot a lack of confirmation for new highs, triggering when new 52-week lows are greater than new 52-week highs while the index itself is near a peak. This is an alarming scenario, as it shows more stocks are breaking down than breaking out, even as the index appears strong. This warning sign flashed four times in five days.

Historically, when the Nasdaq Titanic Syndrome signal has triggered, the forward returns for the Nasdaq Composite have been challenging, particularly over the short-to-medium term.

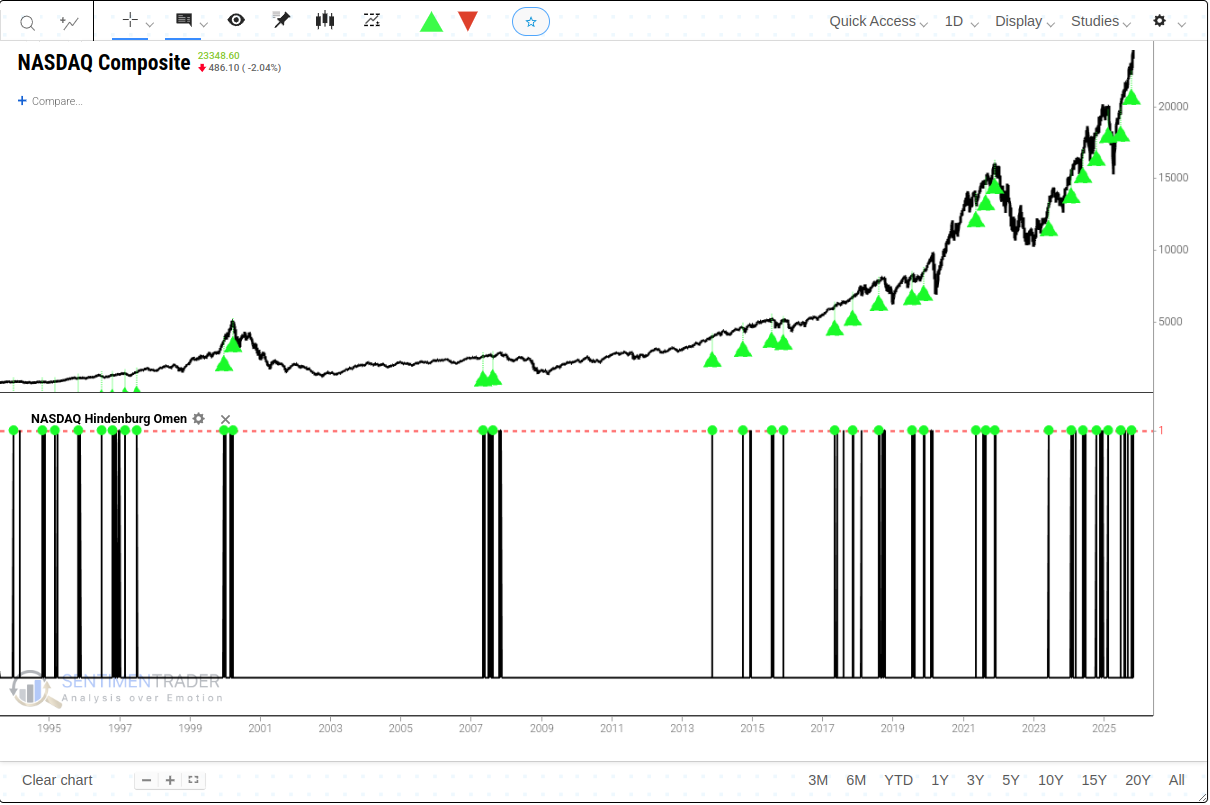

Another classic breadth warning signal, the Hindenburg Omen, has also been active. This indicator identifies periods of extreme internal divergence and market fractionation. A new signal triggered just two trading days ago, adding to the recent cluster. The historical precedent for the Hindenburg Omen is similarly noteworthy. Following the signal, the Nasdaq’s forward performance has been inconsistent.

Here is the crucial part of their note:

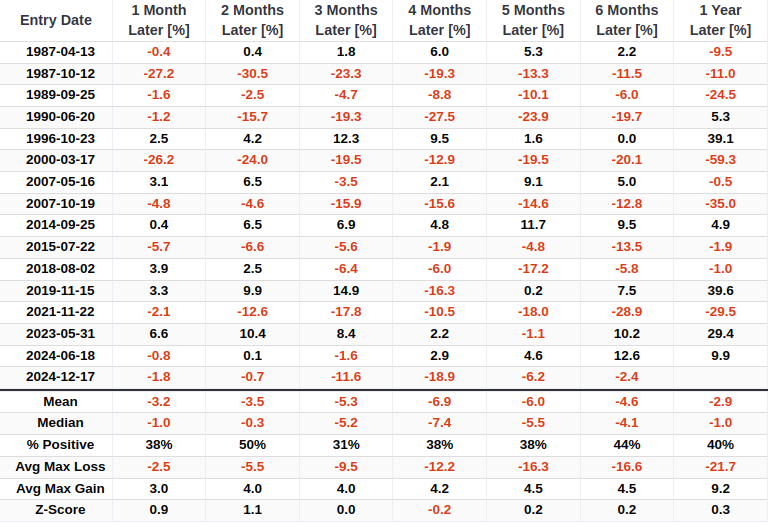

“Individually, these signals are not particularly noticeable. However, when they trigger together in a tight cluster, the warning becomes far more potent. To quantify this, we can create a combined signal that counts the total number of Hindenburg Omen and Titanic Syndrome signals over the past five days. With four Titanic signals and two Hindenburg signals recently, this count has now exceeded 5, triggering our cluster model.

When this rare cluster of signals has occurred, the forward returns for the Nasdaq Composite have been decidedly poor. The median return has been negative across all time frames from one month to one year. “

As they conclude:

“Despite the Nasdaq Composite Index hovering near historic highs, a series of potent internal warning signals-the Titanic Syndrome and the Hindenburg Omen-have simultaneously triggered. Individually, these signals merely point to market volatility. However, when they appear together in such a rare, concentrated pattern, historical precedents reveal a distinctly unfavorable outlook: the median returns for the Nasdaq Composite, Nasdaq 100, and even the S&P 500 have turned negative in most time periods.

In this environment, further gains may prove unsustainable. Such signal clusters often prove more reliable than individual trading days, but close monitoring remains essential in the coming weeks. The more trading days that trigger this omen, the greater the likelihood of a reversal in the uptrend.”

With that in mind, trade accordingly.

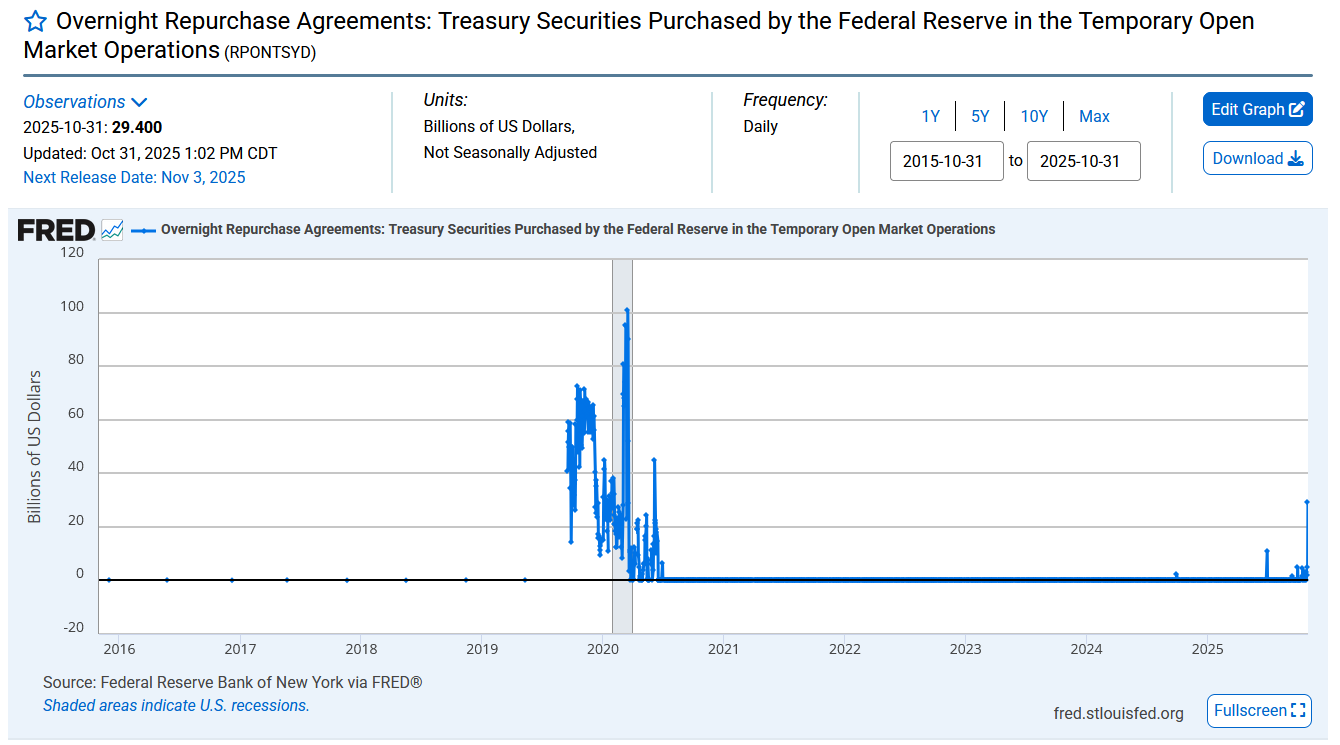

The Standing Repo Facility Points To Stress

In September of 2019, the liquidity markets froze as the largest banks would not lend money overnight to other financial institutions on a collateralized basis, despite the near-zero risk of default. The result was a spike in very short-term yields and the Fed taking emergency measures, including three rate cuts and QE, to improve liquidity conditions. One of these remedies was the Standing Repo Facility (SRF). The SRF allows eligible financial institutions to borrow cash overnight from the Fed by pledging Treasury securities as collateral at a fixed rate. This backstop is priced at a higher interest rate than the repo markets, effectively creating a ceiling on overnight borrowing costs.

Recently, banks have been tapping the SRF, indicating they were unable to obtain overnight funding from traditional sources. This is likely due to the strained liquidity conditions we have been mentioning for the last few weeks. As we share below, the program was used extensively during the 2019 liquidity freeze and during the beginning of COVID-related liquidity stress. As we see, the recent usage is relatively small compared to those periods, but it is increasing. The standing repo facility should help avoid a liquidity problem like the one in 2019. However, with everyone watching, it may also raise concerns among liquidity providers, further exacerbating liquidity issues.

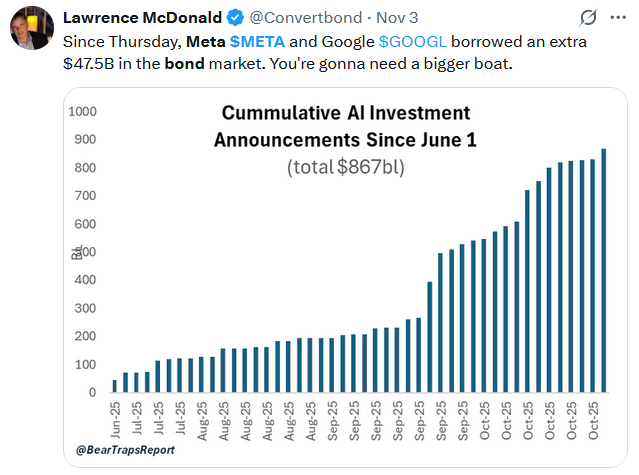

Funding AI

As we led, OpenAI seeks significant financing. It’s not just them. Consider the following bond deals priced over the last week:

Meta priced a $30 billion bond deal on October 30, 2025. The deal offered investors six maturities, ranging from 5 to 40 years. Investors clamored for the bonds, as evidenced by $125 billion in orders, which is over 4x the number of bonds for sale. This capital is for funding AI and data center expansion.

Alphabet’s (Google) $25 billion bond deal ($17.5 billion USD and €6.5 billion EUR) was priced on November 3, 2025. The USD portion comprised eight tranches ranging from 3 to 50 years. Like Meta’s offering, Google’s also attracted significant interest. They reported $90 billion in orders. The proceeds are to be used to fund Google’s AI infrastructure spending.

As we share below in the Tweet of the Day, the cumulative US dollar investments into AI in just the last five months are nearing $1 trillion.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.