Some political pundits think that Iran holds important negotiating cards versus the US if it can control traffic through the Strait of Hormuz. While that may hold some truth today and for the next few months, some of the world’s largest oil producers are ensuring that the Strait of Hormuz is not the lynchpin it is today.

For starters, Saudi Arabia ramped up the usage of its pipeline that crosses through Saudi Arabia to the Red Sea, thus bypassing the Strait of Hormuz. Before the Iranian conflict started, an average of just 770,000 barrels per day (bpd) flowed through the pipeline. The pipeline was converted to full capacity of 7 million bpd in mid-March following the closure of the Strait of Hormuz. While a tenfold increase is impressive, the two end terminals can only handle about 4.5 million bpd.

The second major exporter trying to bypass the Strait is the United Arab Emirates (UAE). The UAE recently announced that it is fast-tracking construction of a second west-to-east pipeline to Fujairah, which will double its crude export capacity to 3 million bpd. Like the Saudi pipeline, the current and new UAE ones will avoid transit through the Strait of Hormuz. The pipeline isn’t expected to be operational until 2027.

While neither pipeline carries 100% of either country’s oil, these two delivery workarounds divert about 25% of the oil that the Strait of Hormuz carried before the war. We expect other countries to follow suit with pipelines and other methods when feasible.

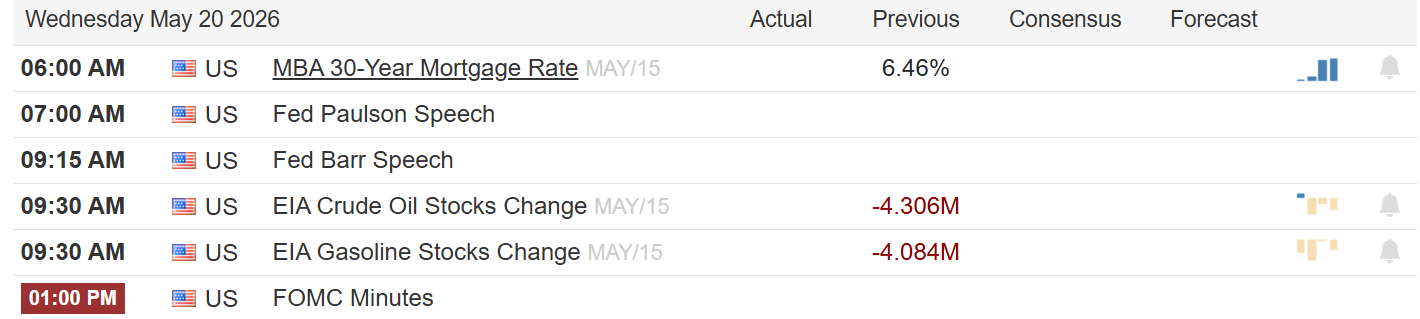

What To Watch Today

Earnings

Economy

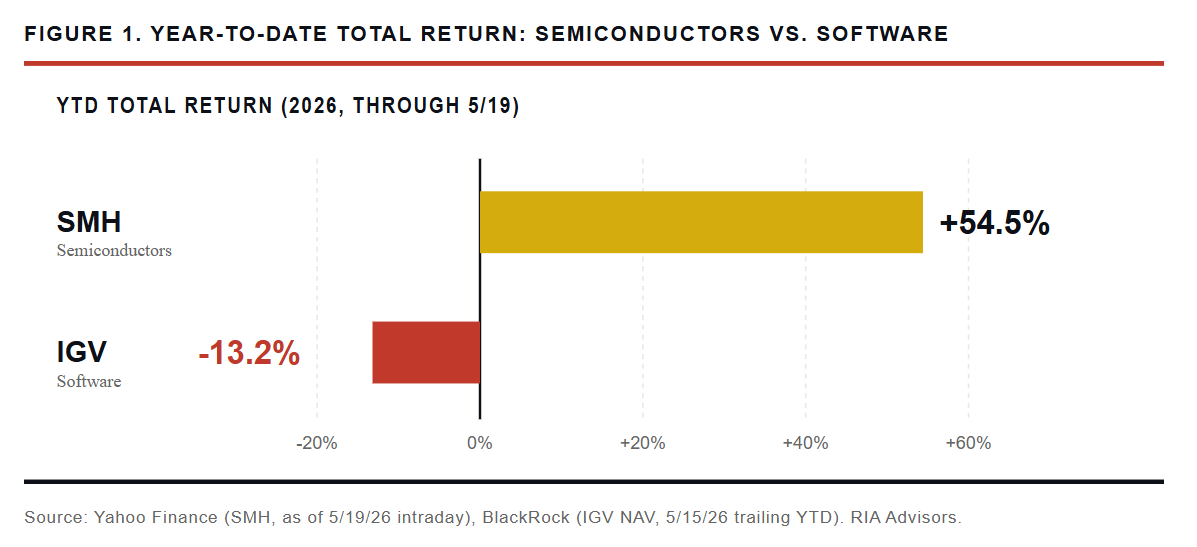

Market Trading Update

Yesterday, we discussed Nvidia’s earnings estimates, which will be reported after the bell tonight, with an expected move of 8% +/- depending on forward guidance. However, since Friday, we have seen a interesting rotation between software and semiconductors.

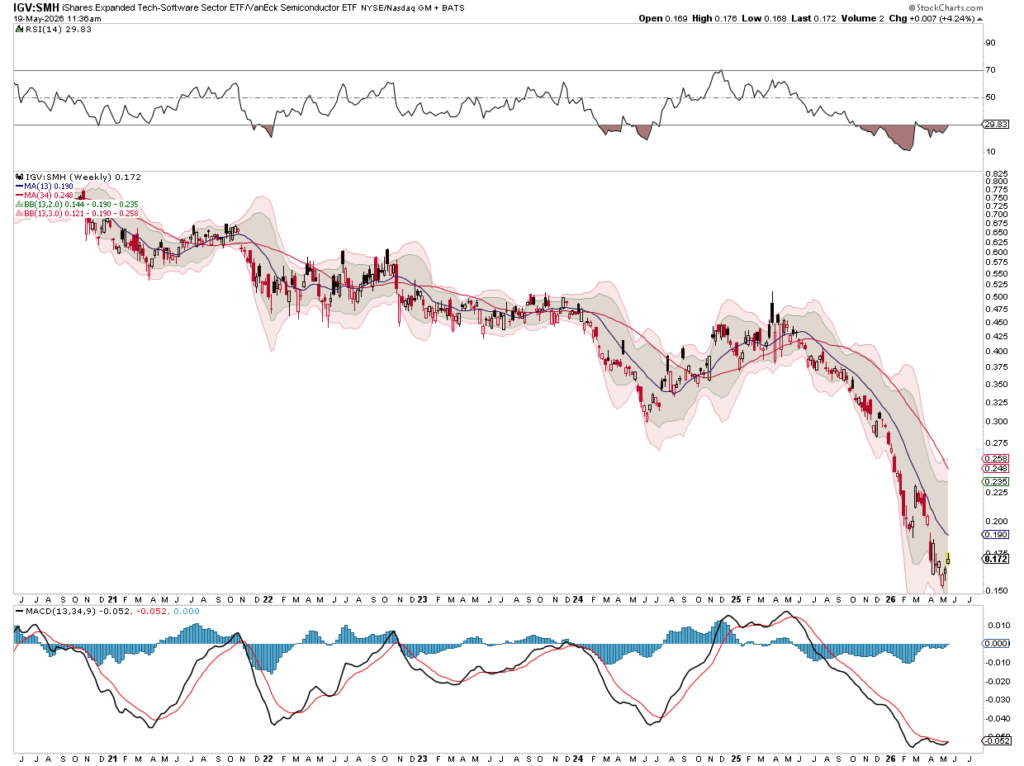

If we look at where the two largest pieces of the Technology sector have ended up, SMH sports roughly a 54% year-to-date gain, while IGV settled down about 13% on the year. That is the widest YTD spread between semiconductors and software I can pull on the screen. And the IGV-to-SMH relative-strength ratio just printed its most oversold reading in the 25 years IGV has traded.

The headline isn’t subtle. AI capex is pouring straight into chips and largely skipping the SaaS layer. Hyperscalers are guiding to roughly $700 billion of AI infrastructure spend this year. Memory pricing has gone vertical, and Gartner now sees global semi revenue topping $1.3 trillion in 2026, a 64% jump.

Importantly, however, software earnings aren’t actually broken. They’re just being graded on a curve nobody can clear. Per FactSet, Q1 2026 earnings growth came in at 52% for Semis & Semi Equipment and 19% for Software. Both are strong numbers. But in this market, only one of them gets credit.

Notice what’s happened. SMH trades north of 44 times trailing earnings. IGV sits closer to 23 times forward, which puts software at a discount to the S&P 500 forward P/E of 21.4 for the first time on record. The premium that recurring revenue earned for two decades just got priced out.

However, here is where it gets interesting. Software is the most-disowned corner of large-cap tech right now. Positioning is light, sentiment is bombed out, and dealer books are full of cheap short calls that nobody bid for in months. The setup is asymmetric. The IGV/SMH relative ratios’ 14-week RSI hit 15 earlier this year, the lowest reading on record. Mean reversion from that extreme rarely happens quietly.

The bottom line is the next squeeze in tech may not be more chip stocks ripping to new highs. It may be the long-forgotten software complex finally catching a bid as dealers and underweight institutions scramble to cover what they spent six months unwinding. IGV just reclaimed the $88 zone, broke a head and shoulders bottom, and registered its first one-month relative strength against the S&P 500 in months. Even Goldman Sachs called the Q1 selloff “overdone.” The pieces are lining up.

We’re watching the $94 to $101 zone on IGV. A clean breakout through that band, on volume, would be the tell. Conversely, a fresh leg lower in SMH on AI-capex doubts would do the same work from the other side. Either way, the trade that’s worked for nine months has the highest negative gamma if it stops working.

Are Software Stocks Ready To Take Chipmakers’ Throne?

Recently, semiconductor stocks have been the undisputed kings of the AI trade. The primary semiconductor index ETF (SOXX) is up more than 130% over the past year, easily outpacing the S&P 500’s 24% gain. Further in the dust lies the software stocks (IGV), which are down 12% over the one-year period. Micron (MU), up 600% over the past year, exemplifies the semiconductor run, riding a narrative of insatiable demand for chips to accompany the massive AI-driven data center buildout.

Software stocks, meanwhile, have not only sat out the party but also languished. ServiceNow (NOW) is a case in point, down by nearly 50% over the last year. Despite posting consistently strong revenue, earnings, guidance, and AI-driven workflow adoption. NOW and other software companies are considered relics of an outdated industry, with no moat against AI. Whether the chip or software narratives are true has yet to be seen. However, the sharp divergence in returns is worth noting.

Thus far, with AI, we are seeing infrastructure stocks, like hyperscalers and chipmakers, lead the way higher. However, AI spending and development will shift once the infrastructure is more fully developed to more agentic uses. This is when money flows from hardware to deployment and monetization of the technology. This should include some software companies.

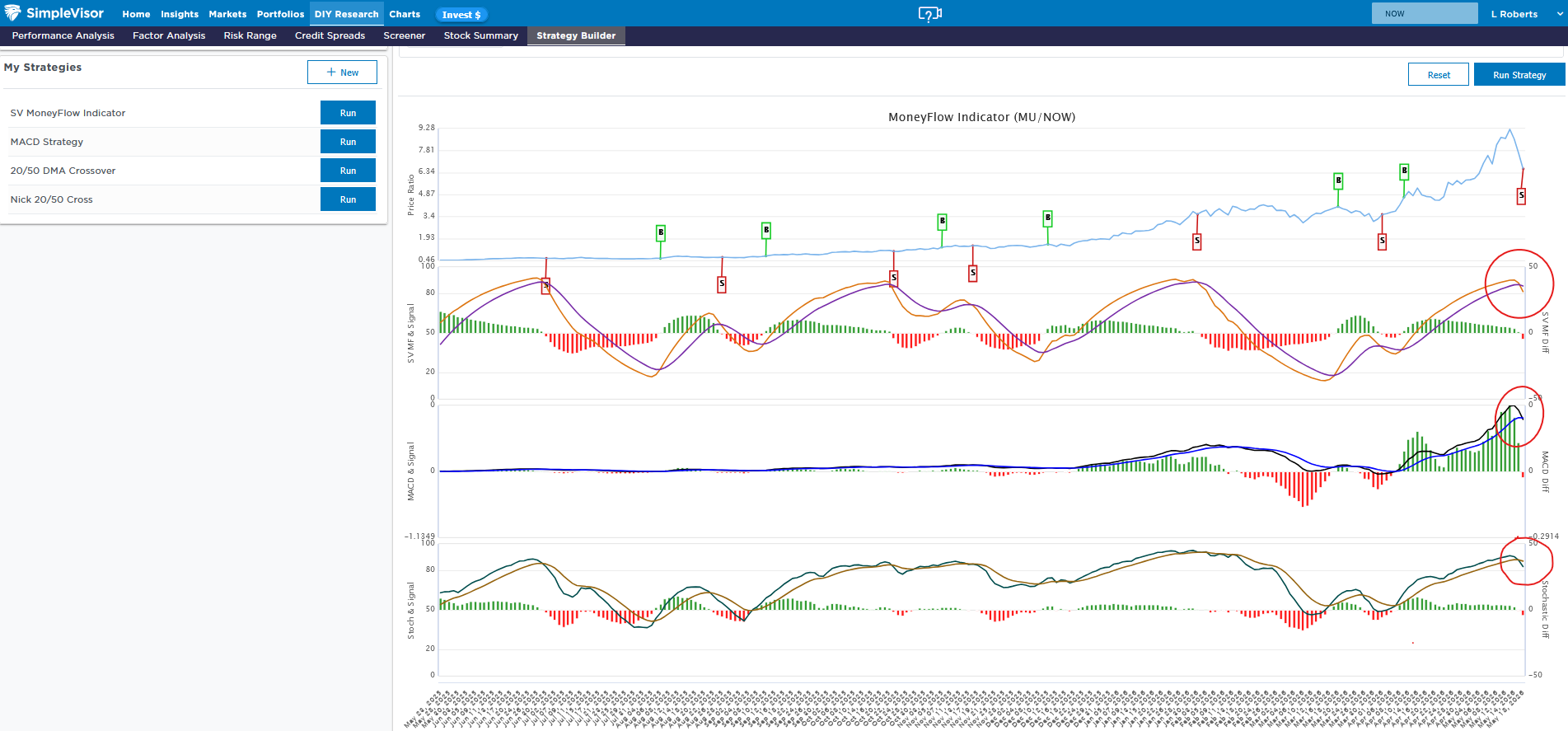

The setup for NOW is compelling. Valuations relative to growth have compressed while the fundamental story has strengthened. Its enterprise AI adoption is moving from pilot programs to generating real revenue. MU is riding the wave of sharply rising memory prices, which is great. However, chip pricing has always been volatile and tends to peak when the news is best, as it is today.

The graph below, courtesy of SimpleVisor, charts the MU-to-NOW price ratio. As shown, the ratio is up 1300% in just one year. However, the three technical indicators of the ratio are turning on sell signals, favoring NOW over MU.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.